TLDR; Don’t be a dummy when you get to the finance and insurance department.

First off… thanks to everyone that posts here for your knowledge. I was a first-time leaser and even though I read many posts here, I still got run over when I got to the F&I guy. I am putting this here as a cautionary tale, but also would like some advice on the best way to proceed.

I had read many things here on LeaseHackr about how to evaluate deals, but unfortunately, not enough on what to do once I got in the F&I room - previously I’ve always paid cash for used or CPO cars.

Let the story begin.

I had spotted what looked like a good deal on a loaner BMW. It had less than 5000 miles, the title had been taken by dealer after a few months of trying to sell - and then been used as a loaner for about 4 months. It was about 17% off MSRP, and I confirmed with the Internet Sales rep that it was eligible for the new BMW lease rebates ($3250 + $2000 loyalty on this model).

I then asked for a $0 cash down except for drive-off costs quote.

Here’s what I got.

OK, so I couldn’t make the numbers quite match the LeaseHackr calculator I’d created - mainly because it was unclear what the drive-off fees/costs actually were - e.g. the MSD were $3150, leaving $2366 for first month + other costs. I knew this dealer was renowned for marking up the MF, but the tax was definitely going to be more, and I assumed it had to include the $925 acquisition fees - was that the $955 listed as DMV/State fees on the quote? Well, I thought, I’m going to be a hardass when I get there and go over the full worksheet.

Lesson 1: Ask for a detailed breakdown of drive-off costs in your quote before going to the dealer

I get to the dealer - the Internet Sales rep was perfectly fine - but then I get to F&I.

- He hands me initial papers to sign off regarding this being a “used car” and therefore provided with “No Warranty”. Well, I knew BMWs always had 4 years warranty from date of in-service and it was on the car, not the owner - so I assumed it was just referring to no explicit warranty from the dealer.

Lesson 2: Ask about the manufacturer’s included warranty

- He pulls out a single sheet of paper with various “protection packages” in three different columns. First column included things like Lease Wear and Tear, Tire Protection, “Maintenance package” etc, second column had fewer, and third column had just “Maintenance Package - $1450”. The BMW logo and name were absent from the sheet of paper.

I pointedly said “No, I don’t want anything” (echos of many posts stating “reject every package offered by F&I” in my head). He continued to press, saying “well, you know you’re going to need brakes and rotors done before you hand this in - are you sure you don’t want the maintenance package”? Again, I said “No”.

He rattles away for about 20 seconds on his keyboard, then asks “What if I could cut the price to about $800”? Still “No”, I said.

He types on for about another 30 seconds - looks up at me and asks “Are you a member of Costco?” “Yes” I state truthfully. “Well, what if I reduce the money factor so you can add the maintenance package for only $15 extra per month?”

Danger! Danger! Will Robinson!

This is where, somehow, I lost my brain and succumbed. Don’t be a dummy like me.

Lesson 3: Just keep saying No

Instead, I said, “OK, if it’s only $15 per month, then I’ll do it”.

With a gleam in his eye, he finally turned around the computer screen so I could see the lease worksheet with a monthly of $461.

At no point did he volunteer that BMW’s Ultimate Care 3 year/36 months program from in-service date is supposed to carry over to the first lessee on loaner cars. If only I’d read more about the Ultimate Care programs in other forums, I’d have been aware of this. Instead, I didn’t have that information to counter him.

Lesson 4: Educate yourself on all of your manufacturer’s warranty/maintenance and conditions before getting to F&I

- At first, I decided to go through all the numbers and compare them to my LeaseHackr calculations.

I asked him to reproduce what my original quote had been - without the maintenance. I asked “Can you show me how that gets to $5,516.46 upfront?”

He entered the 7 MSD at $3150 and an initial MF of 0.00180 (compared to the base 0.00128). What I did not know then is that BMWFS supposedly allows only a 0.0004 dealer markup - so the max he should have been showing me was 0.00168.

I knew total up-front costs should have been just the 7 MSD + the first month payment + taxes + fees. I started doing the calculation on my own piece of paper with the numbers he was showing on the screen for acquisition cost/fees etc. I pointedly asked him “so this upfront includes the $925 acquisition fee, right?”. Based on the presented numbers on his worksheet, the total came out to around $5180, not $5516.46 as on the quote.

“Where does that missing $336 come from?” I asked. He paused for a second, and started playing around with the worksheet. He couldn’t get it to match on his screen no matter what he tried to do - he played with the MF bumping it up to 0.002, he tried changing the cash down - he couldn’t find the $336. He tried to get me to double-check my figures - and again I included the $925 acquisition cost in the upfront costs, showed him all the numbers and it still came up $336 short.

Eventually he laid the blame on the Internet Sales person. “Well, I guess she wanted to get you under $450 so she must have added that $336 as a cash down payment”.

I was indignant. “Well that’s an invalid quote. It says $0 down, but you’ve admitted it includes $336 cash down. I want that $336 backed out of the deal”. I was ready (and should have) walked out at that point. Don’t be a dummy like me.

Lesson 5: When your quote-sheet can’t be reproduced, walk away.

He played around with his worksheet some more - and at some point reintroduced the “maintenance package”. But on his worksheet, he still had the $3150 in MSD from the quote worksheet effort (it was hand-entered, not auto-calculated).

“Well, here’s what I can do for you. What if I just change the MSD so that you get $3500 back although you’ve only put $3150 down? That’s an extra $350 back compared to the $336”.

“Can you do that?” I asked.

“Sure, I can just enter $3500 for the MSD to be returned to you at the end of the leaser even though your upfront only includes $3150 of MSD. Will that work for you?”

Fatefully I replied “Yes”. Don’t be a dummy like me.

Lesson 6: Don’t be distracted by the F&I’s sleight of hand in moving numbers around.

What in fact had happened was that he had never actually shown me the breakdown of the drive-off costs. Instead he was just manipulating the rebates/MSD and “invisible” cash-down and making me think I was still paying only $335 in cash down + the drive-offs.

In fact, once I got home that night and rechecked everything in the real lease document line-by-line as used by BMWFS, I realized that the acquisition fee was not included in the upfront costs - it was being capitalized… in spite of my pointing it out when we were trying to reproduce the original quote. Moreover, the fees, registration, taxes and first month’s payment were around $1200 all together. So in fact, that quote sheet I received was based on something more like $1200 cash down! Not the $0 down I had originally requested.

He quickly reverted the MF on his worksheet to 0.00168 - to which I said “hey, I know the base MF is 0.00128, so you’re getting a big markup on this”. And he had the gall to say “Well, that’s the only way we can sell these loaners so cheaply”. What I realized later is that he would not have been able to submit the original worksheet as is because likely BMWFS wouldn’t have allowed any of those quotes which had a MF of > 0.00168 to go through.

- You may think that should be the end of the story - I ended up giving the dealer about $1200 cash down and he sold me a $1450 maintenance package at a maximum MF markup of 0.00168. Don’t be a dummy like me.

But here’s where things became even weirder, and where I think the sloppiness of the F&I guy will actually work in my favor.

So he starts getting me to sign on everything – using the little electronic signature pad - and although the signatures were indeed for what he claimed, he was just flipping through pages on his computer screen until he got to the signature line - there was no time for me to read it off his screen.

Lesson 7: Ask for a full printout of the lease pages and conditions along with any add-on packages and read through them all before starting to sign.

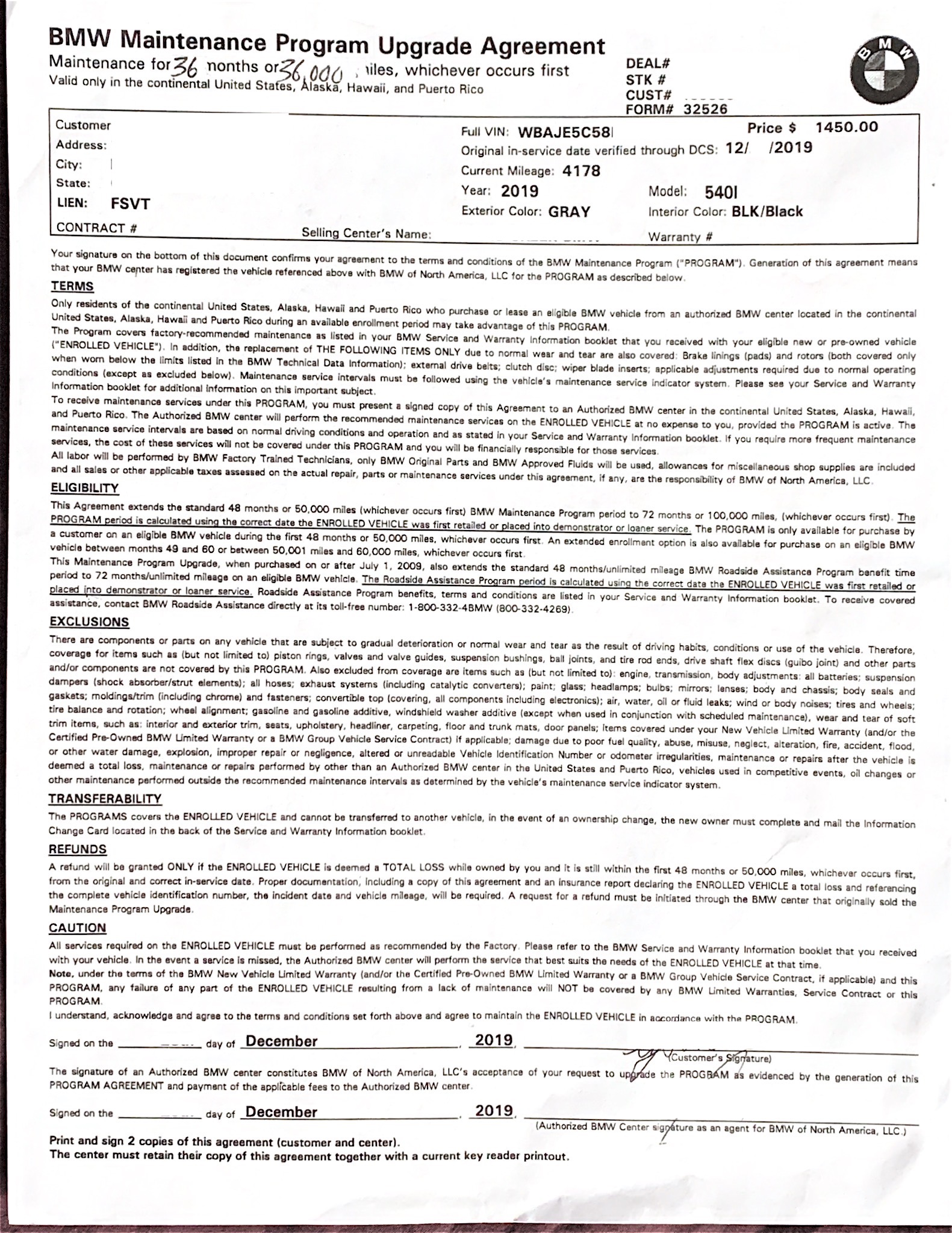

We get to the maintenance part. He hands me a single sheet which is titled “BMW Maintenance Program Upgrade Agreement”. At the top it has printed “Maintenance for 72 months or 100,000 miles, whichever occurs first”.

“Huh? How come this says 72 months, not 36 months”, I asked.

“Oh, let me change that - this is just the standard sheet we use for every maintenance package”.

He proceeds to take out his white-out fluid, cover up the 72 months 100,000 miles and writes “36 months or 36,000 miles”.

I thought this was pretty shady. In fact, further down the page the original text conflicts with what he wrote, still saying

“This agreement extends the standard 48 month or 50,000 miles (whichever comes first) BMW Maintenance Program period to 72 months or 100,000 miles (whichever occurs first).”

Lesson 8: If the F&I guy does something that seems sort of shady, it almost certainly is shady.

Two things to note:

- The reference to standard 48 month maintenance program means the form being used is pre-2016… when BMW changed to a reduced 36 month maintenance program for new car buyers/leases.

- Nowhere on that page does it mention anything about “Cancellation terms”, even though I was vaguely aware from BMW forum posts that California was fairly aggressive on allowing the consumer to cancel up to a certain period of time. It turns out to be 60 days, which I plan to use to my advantage.

Whatever.

I was now a beaten dummy. I had been in the F&I room for over an hour going through numbers - and I was at that typical “let me out of here” moment. I signed the bottom of the maintenance document.

He stuffed the lease agreement and warranty document into a white envelope and I escaped.

I get home and go over the lease numbers from the actual BMWFS lease document - which are of course more detailed than the lease worksheet he shows on his computer screen. I find more posts online about “Ultimate Care transfers to the first leasee of a dealer demo/loaner vehicle”. I spend most of the night awake as I fume over my stupidity and the connivery of the F&I guy.

- The next morning I wake up and contemplate my options.

I’m normally not a confrontational guy, but I was determined to go down and complain - particularly about him not explaining the warranty and Ultimate Care carryover.

I read up on the California Civil Code regarding these maintenance packages and ability to cancel up to 60 days.

I looked over my single page maintenance sheet and realized how stupid I was to accept that. But nowhere on there did it mention the “Cancellation” option - even though the law sees it must explain how to cancel. I decided I needed more documentation about the maintenance agreement - perhaps I could hoist the F&I guy by his own petard.

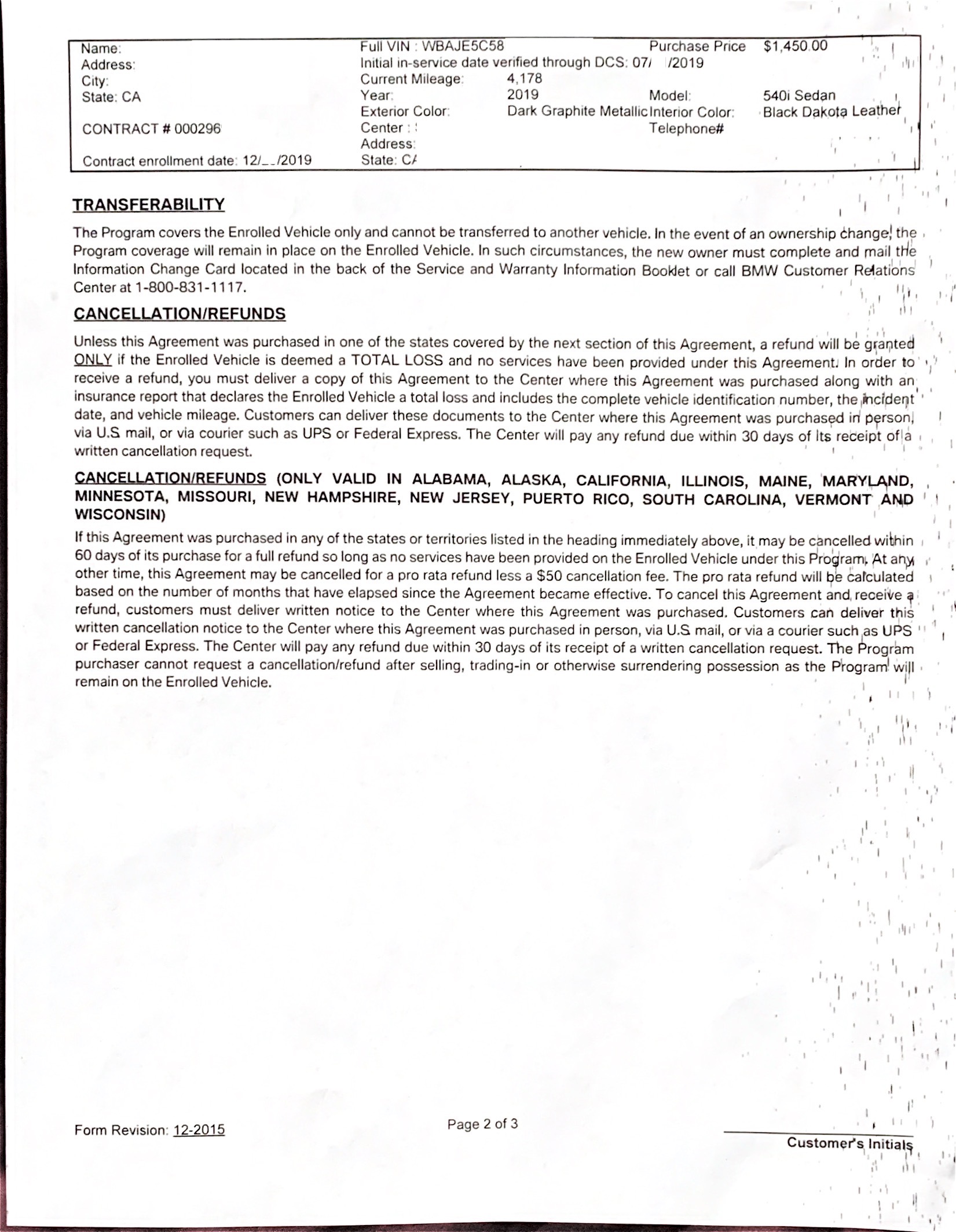

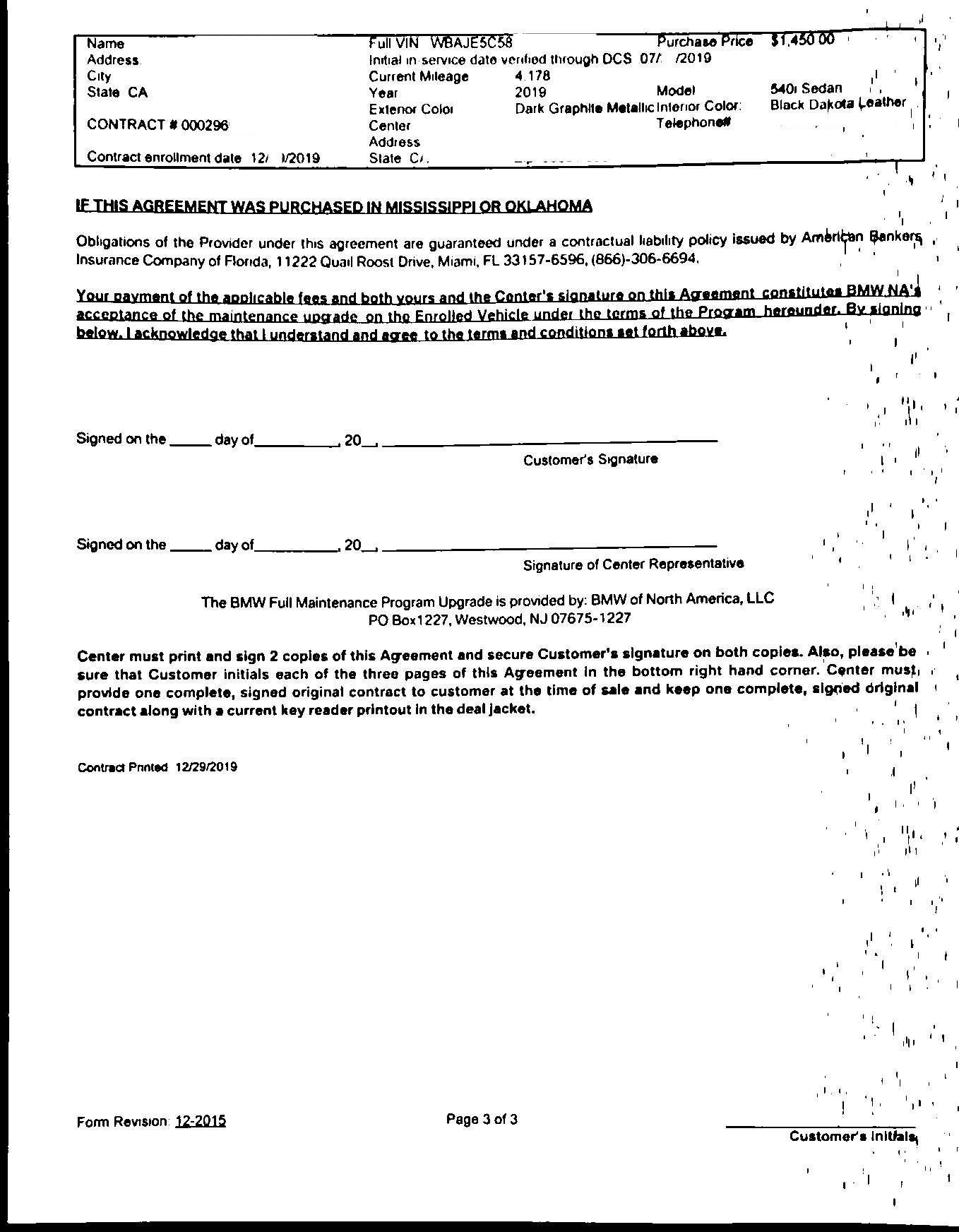

I drove to the dealer and asked for the same F&I guy. I was ushered into his den of iniquity. I politely said, “Hey, I was looking at the maintenance agreement and it seems like there should be more than just this one page. Do you have more detail? A booklet perhaps?”.

“Oh yes, here - I’ll print it out for you”. He turns to his computer and prints out the following three pages.

I quickly scanned - saw that it indeed was just BMW Ultimate Care+ that I had been sold - something that has a MSRP of $700 - and saw the California Cancellation option on the second page.

“Thanks!” and I sauntered out to contemplate my next move.

If you look at the BMW Ultimate Care+ forms, you’ll see that it was pre-printed with all my information, but there are initial lines on the first two pages and a signature line on the last page.

At the bottom of the final page, it has in bold type:

Center must print and sign 2 copies of this Agreement and secure Customer’s signature on both copies. Also, please be sure that Customer initials each of the three pages of this Agreement in the bottom right hand corner. Center must provide one complete, signed original contract to customer at the time of sale and keep one complete, signed original contract along with a current key reader printout in the deal jacket.

So here’s where I must make a decision.

-

Should I just follow the cancellation instructions in the BMW Ultimate Care+ contract? I won’t get the $1450 removed from the capital cost of my lease (i.e. it won’t change my monthly cost), but it will be refunded and go to BMWFS to be applied as prepayments of upcoming monthly lease bills. I’ll go back to the dealer at the same time and demand they give me “the original 3 year Ultimate Care package that BMW Customer Care has confirmed should have been transferred over to me as the first leasee of this loaner car”.

-

Or should I be more aggressive? The F&I guy never presented me with the three pages of this contract at the time of signing. I never signed or initialed any of these pages. Instead he has a signature on a different one-page document that appears to be 3-4 years old and no longer current. There isn’t any way that he conformed with the instructions on BMW’s own contract. What will happen when BMW receives that one page with white-out (the only one that has my signature) and no mention of Ultimate Care+ on it. Is he going to fake that I signed and initialed on the 3 pages of Ultimate Care+ contract?

Should I escalate to the dealer GM? Or BMWUSA?

On the one hand, with the $1450 refunded into lease payments and Ultimate Care reinstated, I’ll still have a fairly screaming deal - LeaseHackr score of 11.5 years and an effective monthly pretax of under $400.

On the other hand, that F&I guy really pissed me off.

But above all, please remember…

Don’t be a dummy like me.

already

already