The purpose of this wiki is to consolidate noncaptive balloon loan guidance and help the community better understand this alternative financing option. Anybody, with proper trust levels, can edit this wiki and contribute additional content.

Why Consider a Non-captive Balloon Loan

A traditional balloon loan combines features of a lease, such as low payments based on a residual value, with features of a loan, such as direct ownership. This type of financing is sometimes offered by captive lenders, like BMW and Ford, who brand them “Select” or “Option” programs, and offer them alongside more traditional lease and conventional financing options.

However, here we focus on programs available from non-captive sources, most commonly credit unions reselling a program administrated by the Auto Financial Group (AFG). At minimum, these programs offer another marketplace option, which should be considered and shopped alongside captive programs. At best, given the right mix of market conditions and program terms they can offer compelling options superior to captive programs.

Benefits of a non-captive balloon loan

The biggest benefit of a balloon loan is the flexibility of multiple termination options. At the end of your loan term, you can either return the vehicle, and walk away, or you can keep the vehicle, by refinancing into a new loan product. Unlike a lease, a balloon loan is also titled and registered in your name. Other balloon loan benefits include:

- Finances a new purchase, capturing rebates only available to cash/retail.

- Finances a used purchase, including a loan refi or lease buyout.

- Permits transferring plates and registration, a savings in some states.

- Excess miles can be purchase for only $0.10 per mile.

Example: Where a vehicle depreciates fast.

When faced with financing a vehicle which will most likely yield negative equity over the loan term, the walk away option keeps your TCO fixed. Consider a short term (24/36mo) with no down payment and focus on finding a low monthly. This is good for many EVs or other heavily discounted vehicles.

Example: Where a vehicle holds value well.

When faced with financing a vehicle which will carry positive equity over the loan term, the buy-out option lets you capture that equity at any time. Consider a long term (72mo) with a down payment large enough to yield the minimum monthly payment to satisfy funding. This is good for rare/exotic vehicles or brands known for holding value.

What Is the Downside of Using a Balloon Loan

A balloon loan carries extra risk. In all cases, the sum of the payments doesn’t bring the loan balance to zero, and a final balloon payment is due. This can lead to hardship as you may be forced to return a vehicle, when you want to keep it, or face refinancing at prevailing rates, which may not be favorable. For most, this risk is manageable but unfortunately balloon loans have a bad reputation. Other risks to consider include.

- In most states, you will need to pay full sales tax upfront. Consider using a trade-in to offset the tax balance.

- Balloon loans generally do not residualize options very well. The best build is a base trim level.

- The interest rate is usually higher versus conventional financing. (to cover RVI)

- Some credit unions may charge an extra origination fee for high-value vehicles.

That’s right… Walkaway, like a lease

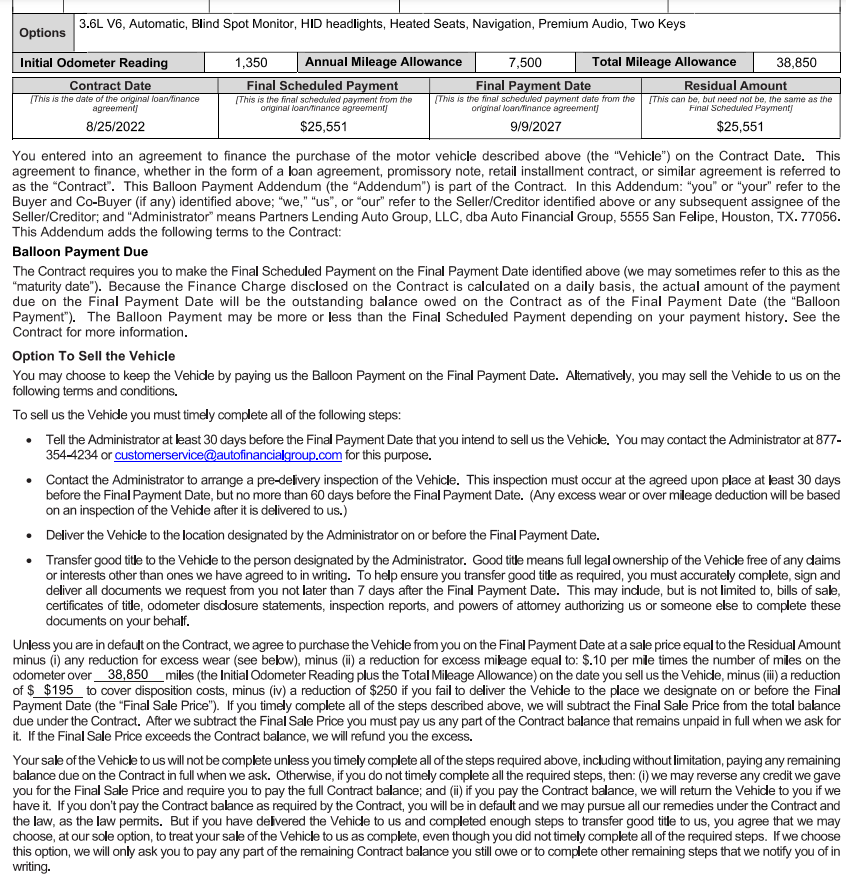

Every AFG-backed balloon loan includes a vehicle return rider. As the market changes, this option can help to insulate oneself from potential depreciation. Returning a vehicle requires paying a small disposition fee, and like a lease, also assess for any extra wear & tear or mileage overages. Examples of the return rider can be found here.

The Right Conditions for a Balloon Loan

Once you have decided that the balloon loan risks align with your personal financial strategy, the next step is to assess if your target vehicle is a good candidate. Most vehicles will not have a competitive program. Research will be necessary to compare payments, and total cost of ownership, across program options. The best way to evaluate a program is by using the AFG calculator, linked later in this article. Focus on finding either a large gap between estimated retail value and purchase price, or a residual value which is way above actual market value. If you do find a good opportunity, act fast, because AFG will change program terms between months. However, once you have been quoted for a program, AFG will honor (lock) those terms for 60 days.

Here are examples where a balloon loan program was useful:

- Challenger - Captures power dollar rebates only available with a retail purchase.

- Tesla M3 - Allows for a quick buyout to captures positive equity during the time Tesla’s were rare.

- Dodge RAM TRX - Takes advantage of a favorable gap between purchase prices and MRM.

- Toyota Tacoma TRD Off Road V6 - Takes advantage of a strong RV for this brand.

- 2022 Jeep Wrangler Willys - Takes advantage of a vehicle which holds value well.

- 2023 Ford F-350 SRW XLT 6.7L - Both a favorable MRM to purchase price gap and a high RV.

- 2023 MB EQS 580 SUV - Both a favorable MRM to purchase price gap and a high RV.

- 2022 Grand Cherokee 4xe - Takes advantage of an MRM much higher than actual market value.

- 202x Ford Raptor - Takes advantage of a vehicle which holds value well.

- 2025 Ram 1500 Laramie - Takes advantage of an MRM much higher than actual market value.

- 2024 Mercedes GLE 63 AMG - Takes advantage of an MRM higher than actual market value.

Where can I get a balloon loan

The most common institutional lender offering balloon loan programs is Auto Financial Group (AFG) and they do not offer the program direct to the public. Instead, the program is offered via affiliated credit unions. Thus, most credit unions who advertise a balloon loan are almost always reselling the same AFG program. Some credit unions may call these programs something like “better than a lease” or “payment saver” and may charge different rates and/or fees – but they are all fundamentally backed by the same paper. The below list provides suggested credit union offering this program.

CapEd Credit Union (https://capedcu.com/) Payment saver auto loan product offered at moderate rates across various terms. A one-time donation to the CapEd Foundation permits membership. You can join and apply online, you will be assigned a loan officer who will follow-up over the phone. Can close quickly, great customer service.

First Eagle Federal Credit Union ( Flex Auto | First Eagle ) Low rates with full access to the AFG balloon loan portfolio via Flex Auto program offering. Membership is possible by joining their Financial Fitness Association. Must join as member first, before applying for auto loan. Poor customer service.

Hanscom Federal Credit Union (https://hfcu.org/) Better than a lease auto loan product offered at a generally higher rate than above choices. A one-time donation to the Nashua River Watershed Association permits membership. You can join and apply online, you will be assigned a loan offer who will follow-up over the phone. Good customer service.

AmeriCU Credit Union (https://americu.org/) Paysaver auto loan product offered at low rates and across various terms. A one-time donation to the American Consumer Council permits membership. You can join and apply online, but I recommend pro-actively calling a branch and working directly with a loan officer. Can take longer to close.

Park City FCU ( Loan Rates - Park City Credit Union ) New option offering low rates and backdoor membership by joining a supported non-profit organization. Hard to reach, no first-hand experience. Looking for more feedback.

Another institutional vendor, CULA, is often discussed as another option. However, it appears that these programs are only accessible to dealers and not the general public. These means to access these programs, you must use a dealer from the network.

How Do I Use A Balloon Loan Calculator

- AFG Default Payment Calculator AmeriCu Calculator Use this calculator first, to determine the loan balance, interest rate and monthly payment for your preferred term. The following calculator is an example setup for a Ford Mach-E purchase in NJ. Since we will not be returning the vehicle, the lowest mileage option has been selected.

- Balloon Loan Reverse Calculator Balloon Payment Loan Calculator |- MyCalculators.com Use this calculator second, take the data from the previous calculator to solve for the final balloon payment and generate a complete amortization schedule. Where-as the final balloon payment is the buyout at the end of the term, the amortization schedule will provide the buyout for any month in the term. The following calculator continues our example, solving for the Ford Mach-E 24-month final balloon payment.

Acronym’s & Terminology used in this wiki

MRM / CRV / Estimated Retail Value - This is the value of the vehicle assigned by AFG. It is based on the Maximum Residualized MSRP, which consists of the MSRP of the typically equipped vehicle and value adding options giving only partial credit or no credit for those options that add little or no value to the resale price of the vehicle.

Purchase Price - This is the price you can purchase the vehicle from a dealer.

Down Payment - Upfront funds used to reduce the loan balance.

Total Amount Finance - The amount of the loan

Conventional Rate - The rate commonly offered on traditional finance.

Balloon Rate - The rate offered with the balloon product.

Annual Mileage - Mileage affects the residual value of the vehicle.

Residual Value - The forecast value of the vehicle at the end of the loan term.

Balloon Payment - The final payment due at the end of the loan term. Same as RV.

MMR - Manheim Market Report, the wholesale value of the vehicle at a given point in time.

{kind=link}