Here is my strategy if the “email dealer for quote” method is getting you nowhere. Often times, dealers won’t give precise numbers over the phone/email, since they fear you will just shop that quote to a competing dealer. They should still give you a quote anyways, but whatever.

-

Make a fake Truecar account (come up with some bogus name and address along with fake phone number and email…all you will use this account for is collecting Truecar quotes from dealers). More on why you want a dummy account, aside from avoiding dealer spam, below.

-

After #1 is done, enter the zip code of the DEALERS you are interested in shopping at. Once you spec the car you want, you’ll get Truecar pricing for local area dealers for the car you are interested in (and select all applicable incentives when customizing the car you want). Do this several times until you have entered zip codes for all dealers you realistically will shop at. Each time you run a search, select the largest discounted unit, and make a note of the discounts somewhere (screenshot, excel spreadsheet, whatever).

***be aware that some of the discounts listed will be PURCHASE only, and will not apply to a LEASE. -

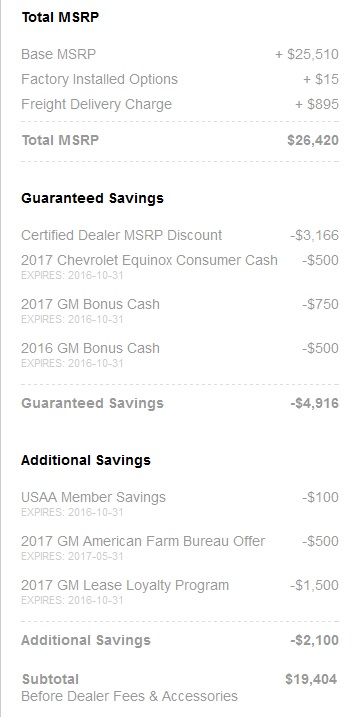

Analyze the Truecar breakdown for the lowest priced unit you are interested in. I’m including an example below for a 2016 Chevy Equinox LS:

The main figure you want to zero in on is the “Certified Dealer MSRP Discount”. That’s the discount the dealer has agreed to give for anyone using Truecar for quotes, before any manufacturer incentives. Dealers typically have to pay Truecar a finder’s fee for anyone that uses the service for quotes…I believe it’s around $300 these days. This is the reason you should use a DUMMY Truecar account, so you can avoid the Truecar fee and instead have that money added back to YOU instead as an additional discount. If the dealer is getting charged $300 for a Truecar lead, guess who ends up paying for that fee? Hint: it’s not the dealer.

So if the Truecar certified discount is $3,000, the dealer should be willing to give a discount of $3,300 if you negotiate directly with them, since they don’t have to pay Truecar. -

Armed with the MINIMUM discount the dealer should be perfectly fine giving out (Truecar dealer discount plus ~$300), now is the time to actually contact the dealer for real. Find the email info for the internet sales manager of the dealership (probably listed in the Truecar pricing breakdown somewhere), and say you are interested in stock #123456 (or a similarly equipped unit). Say you want at least (whatever Truecar discount + $300 is…ask for more of a discount if you are feeling lucky) off MSRP as a DEALER DISCOUNT, and also state what incentives you also should qualify for.

Since the dealer now knows you have hard numbers in mind, it should make negotiations more straightforward. -

Once you hash out an offer from dealer A, it is now time to shop it to dealer B, C (and however many other dealers you want to shop at). Tell them dealer A has offered insert purchase/lease numbers, and ask if they can beat that offer, as you are planning to purchase in the very near future.

-

Get the best counter-bid, and then take it back to dealer A to give them a last shot at beating it.

-

Once you get the lowest/best offer, only then should you schedule an appointment to hammer out the final deal on paper. And be braced for potential surprises, even if you have seemingly struck a deal through email.

Note that even following these tips, you may still get stonewalled with dealers insisting you come in person to discuss any real numbers. And it is entirely possible to get better quotes without even using this Truecar-based method. This is just a way to start off with getting “DECENT” quotes

AND it’s also entirely possible that all local dealers in your area are offering only crap discounts through Truecar. The hope is to find at least 1 dealer that is offering large discounts off a unit that you can then use to negotiate a better deal.