What are the DTI limits dealers Will work within? I have a strong lease history, 800+ credit, but have income that won’t be considered, and just bought a new property, so DTI appears high. I’d like to get into a new lease but don’t recall DTI limits.

If you’re an 800+ you shouldn’t have any issues qualifying, but if your DTI is high, you won’t have an 800+.

Income isn’t a factor in credit scoring.

In my 7 years of selling cars I never remember anyone not getting approved that was an 800+, and 800+ didn’t have their revolving credit tapped out either

2 Likes

That doesn’t change the fact that income isn’t a factor in credit scoring.

Hence, ![]() is not a true statement.

is not a true statement.

You can also have millions of dollars in monthly debt payments and have no revolving debt.

1 Like

Yeah I’m no credit expert, just going off experience. If you’re an 800+ and the DTI isn’t out of whack, it’s an automatic approval. Income is factored into approvals though, but you just like to argue for arguments sake.

You were my inspiration.

2 Likes

It doesn’t seem unreasonable to me to want to have a credit thread that has accurate information about credit.

1 Like

A friend of mine walked into a Lexus dealer looking to finance a car. First time buyer but the dealer ran their credit (came back at 760) and claimed that since its first time they need to put over 30% down. This is nonsense right? Should be able to finance zero down with that fico auto score pulled by the dealer?

1 Like

To finance? That’s not normal. Tell him to go to the bank and get his car loan there or credit union.

Anyone have guidance on what BMWFS has been seeking on the M8 approvals as of late? ~157k MSRP vehicle in question. I recall hearing they’d gotten tougher, but I have a colleague in the hunt for one and whether it is a prudent financial decision aside, was trying to see if it was even reasonable for her to run the credit check or if this was likely to get denied.

30 years old, 240k annual salary, 760 FICO, no existing debt.

Prior leases?

1 Like

How can this ever be put aside?

2 Likes

Yes; one with BMWFS (that had a co-signer) but closer to the 750/month range for an M car which ended in 2016, and she’s now wrapping up one with Audi (solo) that’s in the 875/month range for an RS vehicle.

To clarify - while I personally wouldn’t spend 1150-1300/month on an M8 at 30 years old with a kid coming in 6 months, I’m also not her or her financial advisor. And I suppose it very well could be a fine financial decision depending on their individual circumstances, so I probably shouldn’t have made that comment anyways since how she spends her $$$ is ultimately her call. My b.

1 Like

I know she doesn’t have my financial advisor, we fight about leasing (at all) every 3 years.

Your friend should apply then if they want this M8 that bad, hopefully she picked out a carseat to match the interior.

2 Likes

Please let me know if this completely OT… I’ll remove it … But given it’s THE “credit thread”, I’ll give it a shot.

Little background:

I moved to the US in 2011 so that’s my starting date for credit. 2 cars previously financed (all paid off), 2 current leases (1 mine, 1 I’m co-signer for the wife), mortgage, never missed a payment on anything. I come from Italy and the “going on credit card debt” concept doesn’t even exists: you spend what you have, the bank pays automatically the credit card bill at month end. Long story short, refinanced my mortgage 2 months ago and had a 774 credit. I have about $50K available in credit cards, but never go over a $2-3K balance per statement.

Then …

7/11: father in law passes away

7/12: had to buy a space at cemetery (no payment, no space): $27K, had no idea as I never had to do it, I had my Chase with me, put it there (didn’t have my check book on hand)

7/14: card statement closes ($27k due 8/14)

…

7/27: I randomly go check credit: 664!!! 110 points down because of 66% credit utilization!! I lost it … I paid it off immediately (I could have done it then but with funeral and everything going on who knew) and opened a dispute with Equifax (that was still showing 716, but still) and TransUnion.

Is the above really absurd?! Is there anything else I need to do? How long it will take for the score to go back where it was? Next credit pull will be on 8/3, so I’ll see what happens as now the credit utilization is basically 1%.

Thanks all!

Sorry for your loss.

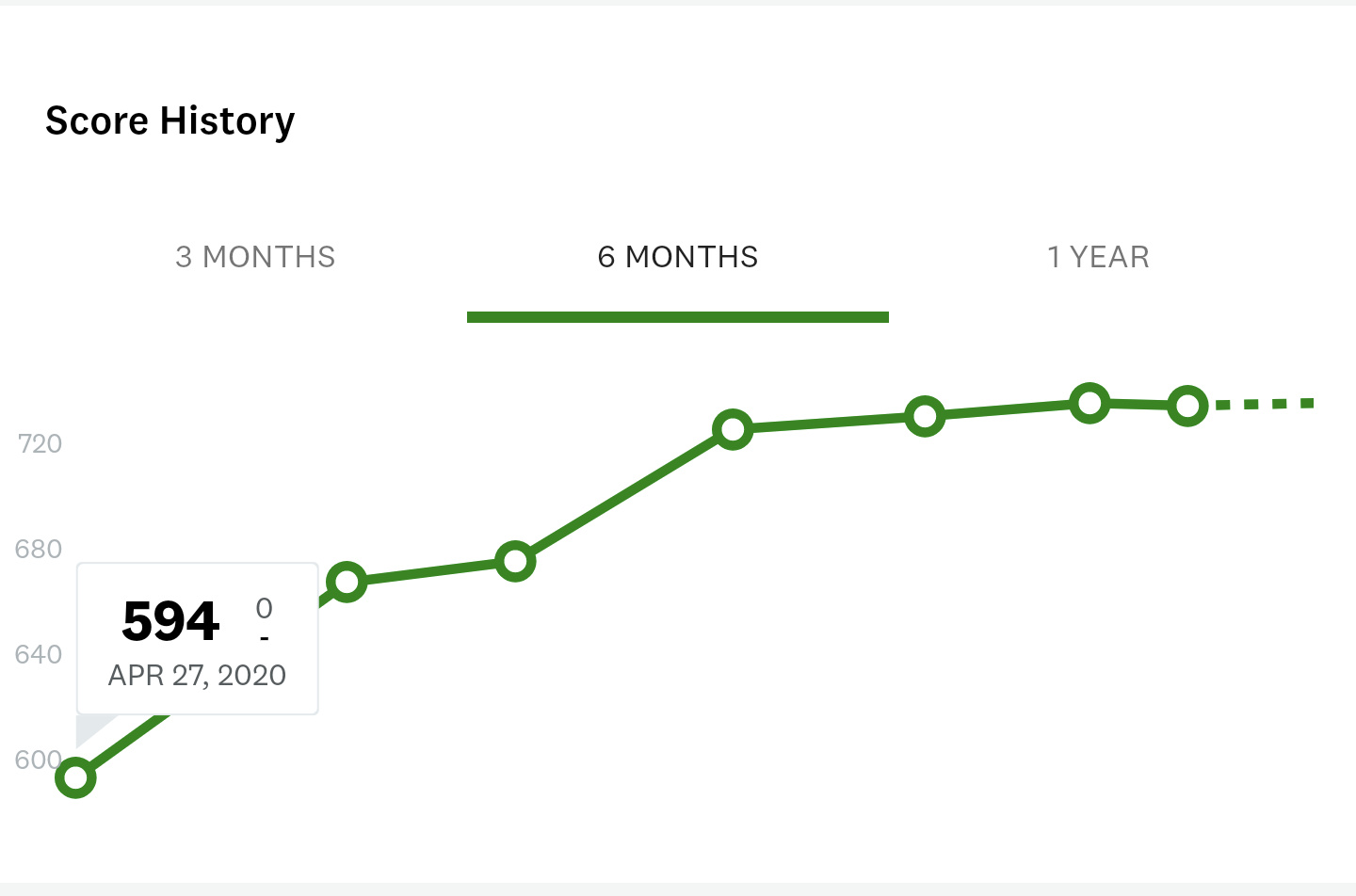

I actually just went through something very similar due to an earlier hospitalization that cost me >100k and suddenly pushed me to >80% utilization out of nowhere. Took me ~3 months to get back on track, even after paying it all off. 760 → 594 → 741 so far this year in just a few months, so it can recover quickly.

4 Likes

Thank you! You made me already feel better. You know, stuff like this isn’t something that (hopefully) happens every day, so I tried not to get even more frustrated with the “could/should have” story …

I’ll see what happens and let you know!

Luca

1 Like

As soon as your next Chase statement closes on 8/14 and reports a zero balance (or much lower than $27k) your score will rebound.

In terms of credit reporting, essentially all that matters is how much balance each card shows when the statement closes each month. The fact that you may pay everything off in full once the statement closes doesn’t matter.

As long as you’re not applying for a mortgage or a car or anything like before next month then these monthly ups and downs generally don’t matter, don’t stress out over it.

And the credit reporting was correct, you really should not have filed a dispute. Save your disputes for when something is really wrong. If you can somehow cancel your dispute I would.

1 Like

From the context and the graphics in some of the preceding posts, it looks like some of you guys are getting your scores from Credit Karma.

Credit Karma provides Vantage Scores. Virtually no company that extends credit or manages consumer credit accounts uses Vantage Scores in their business.

They’re really quite useless except to help consumers understand some basic principles of credit scoring.

A lender is almost certainly going to pull one flavor or another of a FICO score, which could be dozens or a hundred or more points different from what you see on CK.

2 Likes