$6k is grocery money in the scheme of things.

I haven’t seen anyone suggest liquidating securities to raise MSD money.

MSDs are certainly a better use of money than a 3-year CD, with comparable risk.

$6k is grocery money in the scheme of things.

I haven’t seen anyone suggest liquidating securities to raise MSD money.

MSDs are certainly a better use of money than a 3-year CD, with comparable risk.

We’re at record low interest rate environment. CDs would be an INSANE thing to “invest” in right now. Besides, OP said his $6k went to onepay, not MSDs.

Same concept. Put in $6k to save $2k in finance charges over 3 years.

MSDs or One Pay would come from liquid savings in our household.

0.65% APY is the best I’m getting now.

If you go to M1 finance checking account you can get 1%. But i’m putting ‘savings’ into TIPS which are netting around 3-5% annually…

I wasn’t making the point that OP should’ve put $6k into a savings account. Just stating the obvious that they have an opportunity cost.

In my personal finances I’d MUCH rather have the cash on hand to buy equities or real-estate and just pay the extra $55/mo.

It’s nearly risk free in that there’s no chance of the return going down like an investment in the S&P, which could easily go down.

It’s tax free in that an investment of that $6k, to net the same cash flow, would need to be higher by the amount of the taxes.

Can you point to a single investment opportunity that would guarantee a higher rate of return than 10% post tax?

Sure, there are other investment opportunities out there that are higher reward, but they’re also higher risk. I’m yet to see anything that’s the same level of risk come close.

While everyone’s risk reward matrix is different at what point would you consider MSD’s or One-Pay to be worth it?

On mine the savings works out to approximately $98.50 per month by doing a one pay. Granted the net mf reduction was .00130 - it means I get to drive a Tacoma for $311 per month instead of $410.

Admittedly some were getting pretty good deals at the time with US Bank & Ally however I get to keep the flexibility that TFS offered at the time with transfers, 3rd party buy-outs, etc…( which could change ) in the future as we have all seen.

I think it depends on the environment and the appetite for risk. Today we’re in an inflationary environment with very inexpensive lending. So every day it becomes easier to pay off debts.

Auto leasing is just a loan for the depreciation of a new car. Why pay the loan up front when you know that it becomes cheaper to pay it off over time due to inflation?

I think there’s a balance. You can’t optimize for both cashflow and balance sheet. So you find a balance between the two that works for you.

Opportunity cost is not risk.

Specifically the discount on rent fee is tax free. You don’t pay taxes on money saved.

10% tax-free guaranteed returns is stellar even with the inflationary risk we are seeing . If that was available for all my investments I’d take it and retire today. The only reason I continue to work is the stock market can’t guarantee its historical returns over my expected lifespan, especially accounting for sequence of returns risk.

Its not nearly risk free because there is always a trade off aka opportunity cost. Its not an opinion or a hot take… Its just a fact. When you take 1 path, you don’t take a multitude of alternate paths.

You might be right on the tax side. The $6k is an income or cap gain, but the $2k savings is probably tax free.

I can’t point you to anything in the world ever that is risk free… You could do a $6k one pay lease today and then the market collapses and you could get the same lease for $3600.

I don’t see leasinghacking as an investment strategy. Its a way of reducing cash outflows for auto expenses. Sure spending $6k to get $8k of value is great. But is it the best use of the $6k? Are there more fruitful jobs your 6,000 golden soldiers could be out there doing? Probably.

IDK how many times you need to be told this is wrong.

Fair point. Its still a factor that can’t be ignored.

Also fair point. Early in the discussion I was referring to the $6k equity as not being tax free. But looking at it from a savings perspective, that is as you say, money saved and not taxable.

The S&P out paced this marker the last 10 years. Not sure on the 30 year horizon; probably like 6%… But you’re really looking for 24-48 month benchmarks. If that’s your investment horizon for $6k you could safely put it in FAANGMULA and likely beat 10%.

Really though, through this discussion I’ve decided it is really a function of what you’re optimizing for. If your intention is to optimize for monthly cashflow, its a no-brainer to have a $0/mo payment. If you’re optimizing for your balance sheet, you could take that $6k and leverage it up 96% with a cheap mortgage in an appreciating mkt.

Many ways to skin this cat.

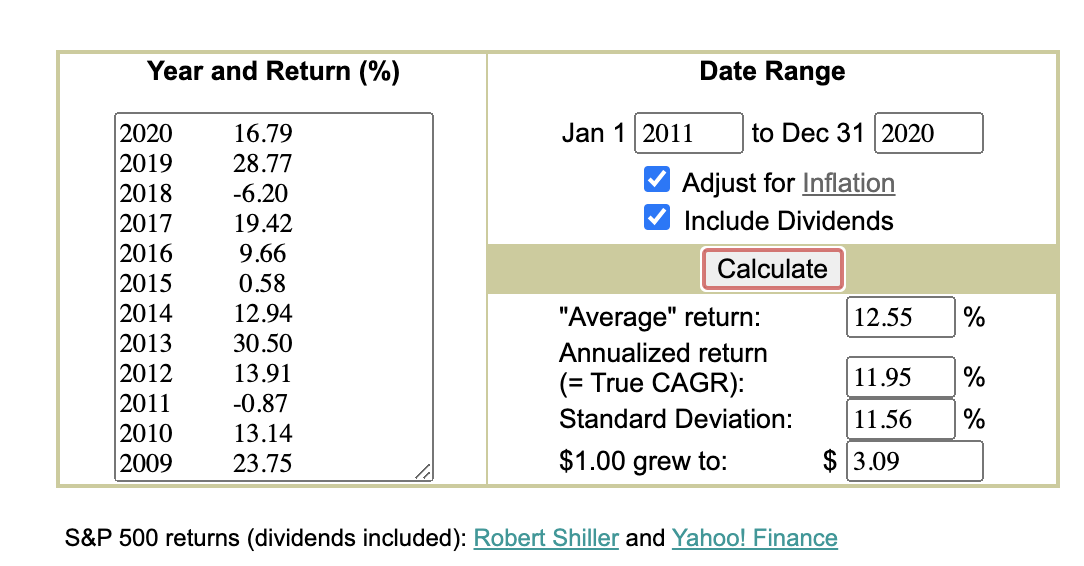

Adjusted for inflation, true annualized return of S&P 500 from Jan 2011 to Dec 2020 is 11.95% pre-tax. So depending on your tax bracket the post tax return can be cut in half:

Even I take last 4 years, the true CAGR is 13.93%.

Source: CAGR of the Stock Market: Annualized Returns of the S&P 500

16% average return from the S&P 500?

You need to hit the books, son!

Or start a hedge fund/ponzi scheme…

Its not a number out of thin air. Look it up for yourself… Even over the last 100 years the returns on S&P 500 are in the neighborhood of 10% averaged. Thanks though, what book do you recommend?

It sounds like we agree that over both the 4yr and 10yr horizon the S&P 500 performed better than 10%. The actual % return would come down to timing.

In any case the top bracket for cap gains is 20%. You’d have to net 12.5% YoY on your $6k during the next 3 years to account for taxes. Its not impossible or even unlikely that you can achieve that.

With all that you’ve stated above, can you explain why you put a ~$5k down payment on your 4Runner purchase when the APR was 2.99%? Why not follow your own advice and invest that money?

Are you talking about the last decade? Well, then 16% is on the money.

But why not use February 2000-2009, where the return was negative 3% a year…cash looked pretty nice then!

Or from the dot-com peak in 2000 to the pandemic sell-off in March 2020…only about 5% annually for TWENTY years…and that’s with reinvesting dividends (don’t forget taxes!).

How about 1965-1974…a juicy 1.2% annual return for those 10 years!

Any period after a bear market (ie. 2009), the subsequent returns are going to be outstanding. Just like the returns from March 18 2000 are fantastic.

There is not a single sector in the market that is cheap these days (maybe China stocks after sell off???). Real estate, art, collectibles, wine are all sky high as well.

Take, for example, Microsoft (MSFT)…from 1999 to 2014, over 14 years, you LOST 30%!!! 15 years is a long time to see a stock not only go nowhere, but actually down…not easy to hold, or to buy. Yet now, after rallying 1000% over the past 9 years, everyone wants to own it.

Point I’m making is that any investment in the stock market, especially at current prices, has a very unknown outcome…especially for under 5 years.

If we look at the S&P performance since 2009 and assume a 20% capital gains, the only time investing your $6k into the stock market for 3 years over using it in this one pay example would have out performed the one pay is if you did so in 2012. Every other year, the one pay wins.

I KNOW MAN TRUST ME!!! If I had known the market would turn the way it did I would have thrown ALLLL my free cash into the market. It was just at the start of the pandemic and I was getting what I thought was a once in a life-time deal.

Doing it again I would take the higher payment. And I actually have around $14k equity in the runner so I’ve been shopping for a smaller car to replace it so I can take the equity out and put it to better use.