I would appreciate some guidance on my “soon-to-be” first lease deal. Due to nature of my job, i drive roughly 15-22k miles a year and i have always refused to consider leasing, mainly due to milage limitations… in the past i had fantastic Apr for finance and latest new bmw330e vehicle was purchased all cash… however, due to the current market rates for financing and high price of this car, i have to consider the leasing option.

I ran some scenarios on excess wear costs at 10k/yr contract vs 15k/yr contract for average of 20k miles driven each year… i came to the conclusion that i can keep money in my pocket with lower mileage contract and buy out the car at end of lease or within 1 year (as i can take advantage of the 7500$ lease credit for ev).

What i am trying to achieve:

-7-8% discount from msrp from dealer plus 7500$ ev lease credit they are giving (roughly 14k off of msrp)

keep payment below 900/mo

-reduce no of months for lease to 36mo (they showed me these two options, but not the 36 mo term…)

-determine what fees can be negotiated ( need some guidance)

-determine whether i put 10-15k down now, or put that towards purchase within a year from now k need some guidance).

-credit score over 800, i need to determing how lower the rate - keep equivalent to 3% (need some guidance)

I ran the calculator but some fields confused me a bit and it didnt turn out like thr photo… i know i am doing something wrong, as i dont have a detailed breakdown.

I can say with confidence that i have not had a less than “excellent” finance or purchase deal negotiated in the last 20 years, but leasing is new and i have been going through gigabytes of data to learn and get the best deal… luckily i found this site and read through it and i know that knowledge is power, so i count on this fantastic group.

I am pushing for 6-7k off of msrp, but i just learned a few minutes ago after getting off the phone wit& the guy, that invoice on this car is 85k. So i am pushing for 84k, which is 5500$ off of msrp, or an additional 1500$ discount from the 4k they already came down.

Thats close enough to my satisfaction of minimum 5% off of msrp.

Hopefully that makes sense

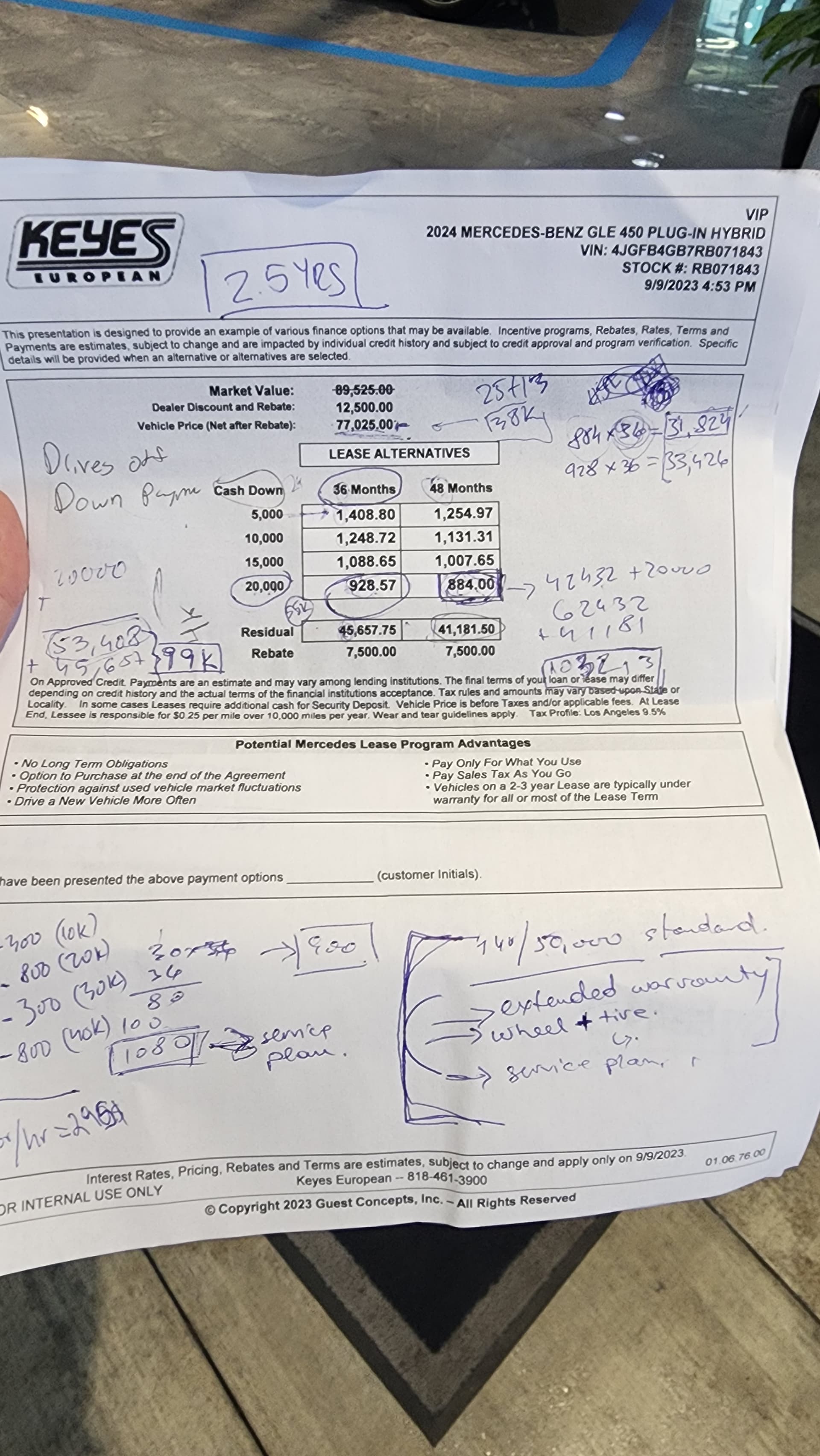

Based on the single paper they gave me and what info i discussed with the rep, i have the following:

-48 month lease

-10k miles

-RV at 41k (46%), which is something i cant compare with other deals since majority are for 36months. I asked for breakdown at 36months as well

-MF at 0.0032 (i think thats higher than what he said said equivalent apr is) - this is their tier 1. I asked him if they are adding anything on top so they make their cut on the finance, he said no… i get what the bank qualifies me for

-due to credit score, i expect no issues in moving up to their top tier, A9, as he described it…this will offer a better MF…i have to see it on paper and run calcs

-incentive is the 7500 ev lease credit for the plug in (which i didnt know they were doing)

-discount is what ive negotiated so far, 4k, pushing for $5500

Again, my overall plan is to purchase/finance this car within 1-2 years .

I am concerned that they want to run the credit to hold the car, even when i put 5k refundable deposit… this is another tactic to ensure that i am “locking” myself in this car, since not many customers want to have their credit pulled multiple times…

Find a great lease, take it to term, and throw keys back at the end.

Lease to take advantage of credits on a car you intended to purchase, buy out immediately and avoid paying any more rent charge than you need to.

The big caveat in your plan is that you don’t know what value a 4yr old GLE450e with ~80k miles is expected to have.

Your first post also begs the question: how does your proposed strategy solve any of the challenges you brought up, namely that the car is too expensive and rates are too high?

I know what you mean and i agree, there might be some contradiction to the overall “strategy”, however in 1-2 year timeframe i would hope rates lower, overall financed value drops more, sales tax in ca will be on a lower value, and i take advantage of 7500 lease credit.

Buy rate mf is .0029 and that’s with your 850 credit score.

36/10 residual is 51% so that’s that.

With 5% off you’re at $1258/mo plus tax and about $3200 DAS

With 10% off you’re at around $1,100/mo plus tax but i don’t think any dealers in so cal are going to let a GLE450e go for 10% off…

GLEs are not really hackable unless you find a rare loaner that you actually want (most loaners are GLB, GLE, C class).

If it comes down to interest rate, you could see if 5% is possible through a credit union but paying all the tax up front will likely negate the savings.

So 0.0029 is 6.96%, based on the formula, correct?

The payments outlined above are without additional downpayment? Ex…15k?

I am assuming that 0.0029 is bottom they would go at mercedes?

Lastly, unfortunately, there are no “fully loaded” loaners or CPO available for this vehicle… i broke the internet checking. Anything new i found within my scope of options is outside of california and im not okay with addining more costs for transportation.

That’s a big IF and that’s also something that can taken advantage of at any time (via refinancing) with a financed vehicle.

The higher the MF, the less of your payment goes towards depreciation and lowering the payoff amount.

After, say, $20k of payments your payoff was only reduced by $10k, would you call that a great outcome?

You’re paying sales tax every month. You’re not saving on sales tax by prolonging a lease that you’re not comfortable buying out.

There are many ways to lower your TCO, with or without a tax credit.

An expensive lease that you intend to buy IF rates come down and pay an exorbitant amount in the meantime, without any data on where the car will be valued in the future with high miles and what your negative equity situation will be, doesn’t sound like the best strategy.

Thanks Max, i get what youre saying, what do you think would be some alternatives or an example of a better approach…

Where and how do i make up for the 7500 lease credit?

Regarding financing, id pay around 8% even with top tier credit score, with 30k down and 85k sales price, id still pay close to 104k for the 60 months.

I just got back from the dealership and i put a hold on the vehicle, which arrives in about two weeks…

I negotiated the discount to 84k (1k below invoice), and got the A9 rate, which saved an additional 1k split up over life of lease, along with that 7500.

Now… i have two weeks to determine whether a 36 or 48 month loan is better in the long run, ss i plan to keep the car. As you can see below, the lowest payment i could get is 884, with total of 20 down to cover otd costs and downpayment.

From a monthly perspective, i am okay with that payment, but in the long run, i am concerned with the overall buyout process.

Or you can just finance it now. $85k out the door. Finance $65k, 60 months at 5.5% through a credit union, $9500 in interest, total of payment and cash down = $94.5k.

Can I just say that if you can afford to put $20k down and are buying a Mercedes GLE instead of a Kia Sorrento or Telluride, you can afford $1260/mo on a loan vs $928/mo on a lease. If you can’t shell out that extra $300/mo without so much as an eyelash batting, you shouldn’t be buying this car.

Dunno about you, but I don’t qualify for the EV rebate because I make too much money. Only way to get this rebate for me would be to lease then buy out

It is not 85 OTD… more along the lines of 94k-95k. Sales tax , registration, other fees, etc are 9k+.

I need the phev for the hov sticker in california, and either x5 or this one will be suitable for my needs and at the top of my budget.

If i were to finance, i would put 35k down. Therefore the plan with the lease was 20k at lease and 15k at buyout from lease.

Okay, in reality, i would be in line with what youre saying on the finance side, 95k-35k downpayment, comes out to 60k financed. Only issue is that i know they would not go down below invoice, like they did on the lease, if i were not financing with them through MB finance, at the 8%…

Now this car doesnt qualify for federal rebat either, so i am not seeing that $… with a finance at that rate, the total at end of the 5 years, i’d be around 102k ish .