You should be doing a one-pay lease to save money. First, negotiate the sell price based on your own research. Next, ask the dealer to increase the MF as much as possible in exchange for a lower sell price. Deduct .00100 from this money factor to get the one-pay discounted money factor. Finally, compute the reduction in the negotiated sell price so that the one-pay amount remains the same.

Here’s an example. Assume the following…

Step 1 negotiated sell price = S = 59111

initial MF = Fo = .00225 → discounted MF = .00125

New MF= F1 = .00290 → MF = .00190

Term = N = 36

Compute the change in sell price as follows…

Note the sell price must be reduced by 1935.94 So, the new sell price is 57175.06. Your Adj. Cap = 57175.06 - 7500 = 49675.06. So that…

Base Pay = .00190 x (49675.06 + 36780.24) + (49675.06 - 36780.24)/36

= 522.45

One Pay = 36 x 522.45

= 18808.20

Before proceeding, you should determine how Indiana taxes motor vehicle leases and the tax treatment given EV credits (7500). Here’s the link…

Indiana Dept. of Revenue

Continuing, here is an example of what you would owe at lease signing…

one-pay 18808.20

one-pay tax 1316.57 = 7.00% x 18808.20

CCR Tax 500.00 needs to be confirmed

*Acq + Dealer Fees 1041.25 needs to be vetted

Fee Tax 72.89

TOTAL DUE 21738.91

Finally, compute an estimate of your buyout within 30 days of signing the lease…

Ave. Monthly Rental Charge = .00190 x (49675.06 + 36780.24)

= 164.27

I believe LFS computes adj. lease balances as follows…

RV - remaining number of payments x Ave. Monthly Rental Charge

36780.24 - 35 x 164.27 = 31030.79 This should be confirmed by reading the LFS early term purchase option in the lease contract.

Buyout = 31030.79 x 1.07 + misc. fees/other taxes

NOTE: Buyout with MF = .00125 is 32913.09 x 1.07… a difference of 2014.06. In either scenario (.00125 v. .00190), you’ll pay the same amount at signing (21738.91). However, the buyouts are different!

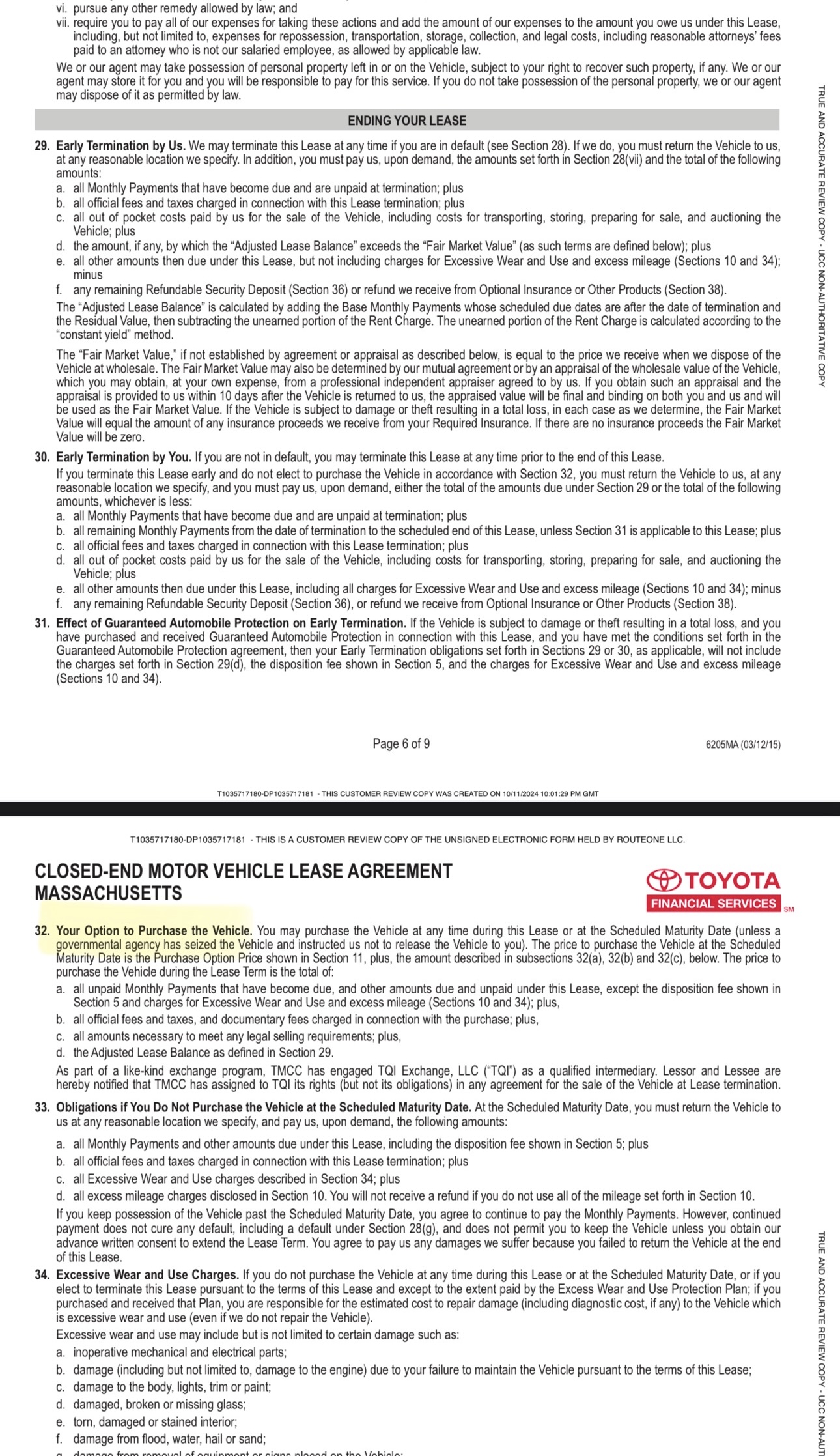

So now you have the methodology for making all pertinent lease calculations for a one pay lease as well as the buyout calculation (assuming LFS buyout calculations are the same in TX and in IN).

You stated…

Where did the 7500 come from? Is that the rebate? If so, that doesn’t count as a dealer discount. The dealer discount is still only 3101.

You also stated…

Why? Most people that immediately buyout their leased vehicle, do so by wisely constructing a one-pay lease. Compare a one pay buyout with a traditional lease buyout within 30 days and see which of the two is more expensive. I assume your goal is to minimize the cost of the lease and buyout transaction thus achieving ownership at a substantial discount (7500). The 7500 would not be available if you bought the car instead of leasing it.

You need to get a sound understanding of dealer fees. Look around this website.

Ah, you will. Lease payments are always made one month in advance. So, if you do an immediate buyout within 30 days, the interest for those 30 days is considered earned. That’s why the above ave. monthly rental charge was multiplied by 35 and not 36.

Here’s what I suggest moving forward…

Forget about dealer profit, holdback, invoice sheets (they don’t mean squat as they don’t reflect dealer cost). Don’t waste time trying to decipher a dealer’s worksheet or chasing after them. Otherwise, you’re allowing them to control the deal. They often omit a lot of relevant detail such as money factor, monthly base payment, monthly contractual payment, fees not itemized and even make mistakes. You need to rely on credible outside sources (e.g., LH marketplace and signed deals, Edmunds, etc.). Do your own research and establish a reasonable selling price in your market. Be sure to get a copy of the factory window sticker. Check for non-factory add-ons or dealer-installed options. And, if possible, eliminate those you don’t need or want. Get a list of all customer and dealer rebates/incentives including VIN#-specific discounts/incentives, if any. And, yes, the dealer has such a list.

The only thing useful about dealer lease worksheets is the input data. All data should be vetted such as acquisition fee, doc fee (regulated by some states), cost of money (e.g., money factor), gov fees, residual, rebates/incentives, sales tax rate, etc. Make sure the residual matches the term and annual mileage requirement. Check available tax credits/incentives via the fund provider who may cover taxes or, at minimum, may assess a lower sales tax rate to energize sales for some models (e.g., Texas).

Organize all relevant data in tabular format with the goal of creating a lease proposal that reflects your target deal. The idea is to create your own target deal (proposal), not replicate the dealer’s deal.

Craft a lease proposal (example below- the round peg, round hole won’t work) and email it to the sales manager (SM), not a floor salesperson as they’re often Mickey D order takers and lack knowledge.

All numbers should be accurate otherwise, you’ll lose credibility. Negotiate via phone/email. Once an agreement is reached, ask the dealer for a review copy of the lease agreement and all contract addenda BEFORE you go to the dealer and sign. Moreover, it’s helpful to know the terms and conditions of the lease contract such as early termination liability criteria and purchase option criteria as well as lease amortization methodology and excess wear/tear criteria. If all is as agreed, tell the SM that you’ll come in to sign asap. You don’t want any surprises or dealer excuses like …. Oh, we made a mistake. That’s unacceptable and shouldn’t be tolerated.

If the dealer isn’t transparent or is uncooperative or showing signs of incompetence, WALK AWAY AND MOVE ON!

Leasing is time-consuming and requires a good deal of study and attention to detail. If you don’t have the time to commit, perhaps your best alternative is a good broker. There are some outstanding brokers on this website. However, if you’re willing to commit your time and resources, always control the deal. That can only be achieved with education which breeds confidence and increases the likelihood of success.

??? Let me know.