Would love input on this deal I got lined up for a lighting lariat. New to the community so love the help!

6.5% off isn’t bad.

What did you do to qualify for $9000

It’s usually ~$5000

Yet another $80K Lariat. (no soapbox this time)

The rebate stack is $9K with Tesla conquest or possibly a private offer.

While $5K dd normally pretty good, we just saw a $8K dd drop.

2 Likes

I think December is gonna be the month for these trucks. Fords gonna shit their pants if they dont offload these, especially the rumors of eliminating ev credit.

CHEVY PLEASE WAKE UP!!!

1 Like

Ya not a fan of 80k lariat and tried to get xplan pricing but 74k was dealer holdback pricing and tried grinding them harder but wasn’t possible. Flash levels definitely they can go harder. This was just delivered and I probably could’ve done better on one that’s been on the lot for 110 days but didn’t like the color and it had the propower and max trailer and I didn’t want to pay for that. Are you all seeing deeper discounts ?

My thinking as well but now I’ll be out of town last week of December so figured may as well get close to end of this month.

My goto Ford dealer is also right around $5K off Lariat, but occasionally you see deals pop up at $7K or more. Like this one-

That is a killer deal. California fees and taxes will always be higher but am wondering if I can shave off another few k the sales price now. All in all doesn’t sound like it’s the best but still pretty good. Appreciate everyone’s input!

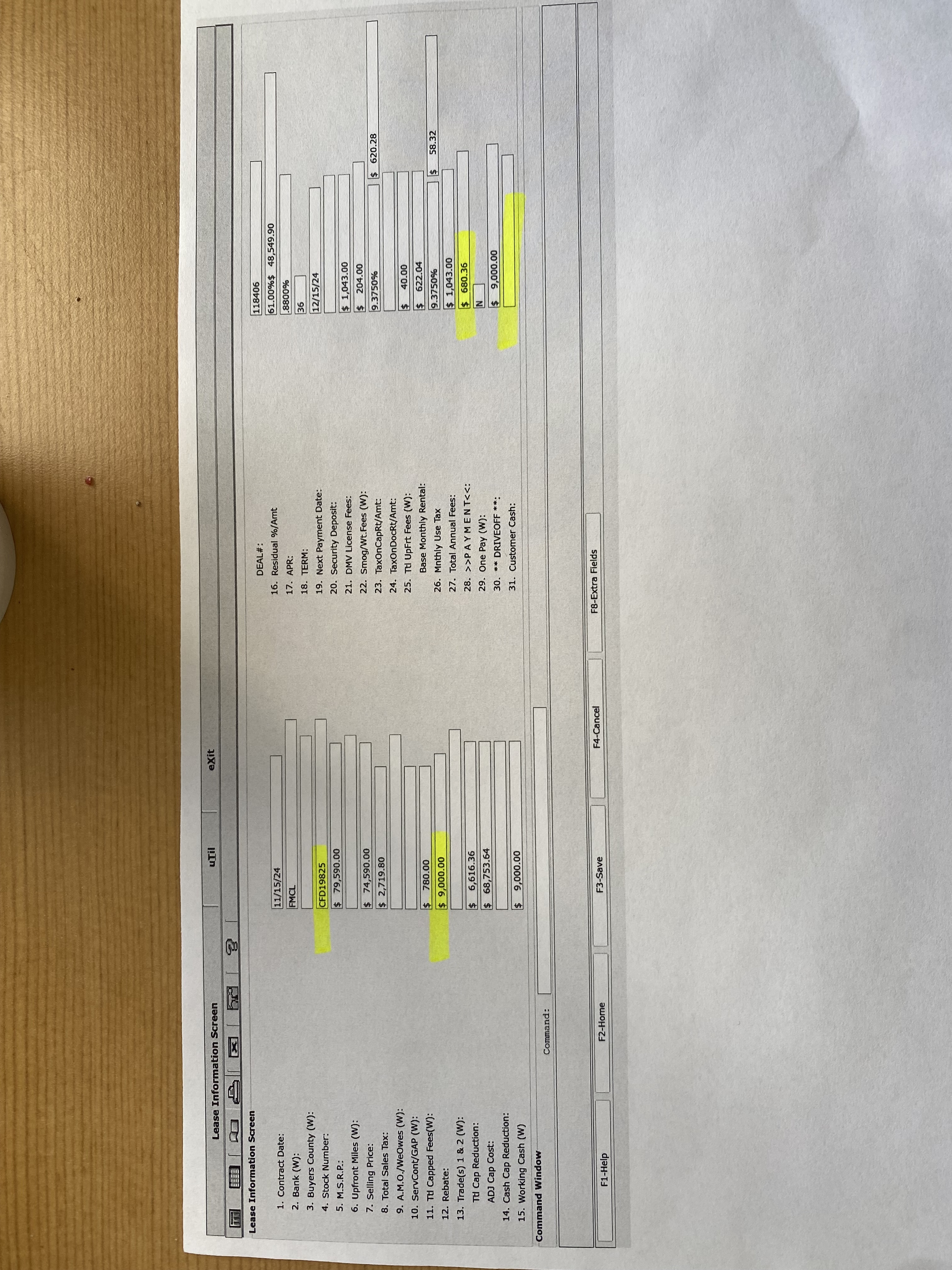

The monthly base payment of 622.04 is inaccurate. It should be 603.50. The easiest way to compute the payment is to use the Excel PMT function as follows…

Base Pay = PMT(.0088/12, 36, -68735.10, 48549.90, 1) = 603.50

Consequently, the contractual payment should be…

603.50 x 1.093750 = 660.08

EDIT:

The CCR is also inaccurate. It should be 6634.90 which means the adj. cap should be 68735.10.

The 9000 rebate is used to cover the CCR and the remaining amount of 2365.10 used to cover lease inception fees as follows…

1st pay 660.08

CCR Tax 622.02

DMV Fee 1043.00

Title Fee 40.00

Total 2365.10

Rebate Credit 2365.10

DAS 0.00

Bottom line: Zero drive off followed by 35 monthly payments of 660.08 each.

1 Like

Thank you for that! How do I best bring this to the dealers attn

im not understanding how the CCR is inaccurate–can you point me to that pls?

This is tough… I’ll give it my best shot…

FMC uses an interest rate, not a money factor. In your case, the interest rate is 0.88%. The formula for computing the CCR is very complicated, and it’s highly likely that they’ll never understand it. To make matters worse, this formula was derived by me and exists nowhere except in my head. And, yes, it is correct. Here’s the formula…

Substituting the assigned values, CCR = 6634.90. The dealer incorrectly calculated 6616.36.

Next, determine the adj. cap cost…

Sell Price 74590.00

Capped Fee 780.00

Gross Cap 75370.00

CCR 6634.90

Adj. Cap 68735.10

RV 48549.90

Term 36

Monthly Interest Rate i .0088/12

Now compute the monthly base payment using the Excel PMT function…

Base Pay = PMT(.0088/12, 36, -68735.10, 48549.90, 1) = 603.50

Or use the formula…

![]()

Whether you use Excel or the formula, you’ll arrive at the same base payment of 603.50. However, using the dealer’s data, they’ll arrive at a base payment different than the one they calculated (622.04) in their quote…

Base Pay = PMT(.0088/12, 36, -68753.64, 48549.90, 1) = 604.02

So, they should have calculated 604.02, NOT 622.04.

Compute the contractual payment (includes sales tax)…

Payment = 603.50 x 1.09375 = 660.08

Last, construct the lease inception fees…

Lease Inception Fees

1st pay 660.08

CCR Tax 622.02 … 9.375% x 6634.90

DMV Fees 1043.00

Other Fee 40.00

TOTAL 2365.10

Rebate Credit 2365.10

DAS 0.00

Observe that the 9000 rebate exactly covers the CCR (6634.90) as well as the remaining lease inception fees (2365.10) including 1st payment…

6634.90 + 2365.10 = 9000.00

Bottom line: Zero drive-off followed by 35 monthly payments of 660.08 each.

Commentary

What’s important is the lease contract, not some half-assed dealer quote. If any of the numbers in the lease contract are incorrect, FMC will NOT fund the lease. However, it is important to compute all numbers correctly BEFORE completing the lease agreement.

Understand that a dealership is a sales organization so they’re not rocket scientist geniuses otherwise, they would be working for NASA. IF you’re lucky, you might find someone within the dealership that understands the math but that’s a long shot.

It’s very foolish and nonproductive to waste hours sitting in a dealership negotiating. This can be a huge distraction. You need time to think things through and formulate questions within the privacy of your own home. This leads me to suggest…

Craft a lease proposal (example below) and email it to the sales manager (SM), not a floor salesperson as they’re often order takers and lack knowledge. All numbers should be accurate otherwise, you’ll lose credibility. Negotiate via phone/email. Once an agreement is reached, ask the dealer for a review copy of the lease agreement and all contract addenda BEFORE you go to the dealer and sign. Moreover, it’s helpful to know the terms and conditions of the lease contract such as early termination liability criteria and purchase option criteria as well as lease amortization methodology and excess wear/tear criteria. If all is as agreed, tell the SM that you’ll come in to sign right away. You don’t want any surprises or dealer excuses like …. Oh, we made a mistake. That’s unacceptable and shouldn’t be tolerated.

If the dealer isn’t transparent or is uncooperative or showing signs of incompetence, WALK AWAY AND MOVE ON!

Leasing is time-consuming and requires a good deal of study and attention to detail. If you don’t have the time to commit, perhaps your best alternative is a good broker. There are some outstanding brokers on this website. However, if you’re willing to commit your time and resources, always control the deal. That can only be achieved with education which breeds confidence and increases the likelihood of success.

??? Let me know.

3 Likes

Honestly, if you have to convince the dealer that they made mistakes, they don’t deserve your business. I wouldn’t waste time defending a Ph.D dissertation explaining their screw ups. I would walk.

BTW, nowhere is the 204 smog fee incorporated into their calculations unless it’s included in the 780 capped fee which I doubt. If you move forward with this dealer, be sure to get an itemization of these fees. I suspect the 780 includes the acquisition fee and dealer doc fee.

delta737h you were right – they were playing games with CCR + MF – once I got into the finance room the payment came up 1.30 more. So then I opened up the quote and realized CCR was different and the apr went 1.24. there were all sorts of humming and hawing once I started grinding them, but once I stood up to walk out, went back to .88 and, shocker, the payment got to that 660. I ended up taking the wearcare plan so out the door for 670 (500 credit with Tesla towards that) given i’ve read that Ford tries to find anything wrong at end of lease.

thank you all for the help!

Do any of the Lightning’s qualify for the $7500 ev incentive in a lease? I am questioning because I was considering a flash, however, I have read xlt, pro and lariat could qualify but not the flash. I thought only stackable rebates ($3500 rcl, $2000 power promise, etc) were the only ccr, can you or anyone clarify? Is the $7500 ev incentive only available with purchasing not leasing?

Ford is keeping the 7500 and offering a $5500 in its place.

1 Like

Its confusing, been a few days i been looking around and i see they offer it on their breakdown. For example…

Stop looking at dealer websites. They’re useless for evaluating what incentives are available.

2 Likes

They are mixing leasing rebates with purchase rebates in there

It makes their discount look good but doesnt mean the bank will give it

2 Likes