Please advise LeaserHacker Community

BMW Financial Services is wrongfully withholding $12,670 from me, as a result of a claim I made with my auto insurance Carrier, Connect. The accident occurred on December 11, 2021. BMW was advised of the accident and had the car picked up the same day. Then, 10 days later, on December 21, 2021, after it was established that the car was totaled, BMW Financial Services issued a demand letter (copy attached) seeking the pay off the amount of $28,069.50, including all associated costs, and even included a sample check-in that letter, indicating that the amount that BMW Financial Services demanded was $28,069.50.

Then, my auto insurance company established, for my benefit, a fair market value, for a replacement vehicle (that I would need to buy on the open market, to replace the one totaled) in the amount of $40,740.44. This amount included the sales tax, registration, and $500 deductible amount for me to buy the replacement vehicle. When I first contacted BMWFS local office, concerned that they received a check in the amount of $12,670 above their demand amount, I was told not to worry, that the difference would be returned to me. Then, since days passed and no check was received, I contacted their office again, to find out how soon I would be receiving the overage check in the amount of $12,670. Shockingly, I was advised that there would be no check sent to me other than one for $100, and when I asked “why”, I was told “No comment”. I guess my only mistake is that I trusted BMW Financial Services to do the right thing, as they first told me they would. Even my insurance company, upon realizing the mistake they made in sending BMW Financial Services the check for $40,470, contacted them, requesting they send back the check and that they would issue a new check in the amount of $28,069.50. They were told that BMW Financial Services had already deposited the check and that they were not going to do anything. What is particularly shocking is that BMW Financial Services has now collected twice for Sales taxed Registration fees, etc…, as they collected it the first time when the lease was first established. This is DOUBLE DIPPING! Please note, this whole situation is both a civil and criminal fraud, as well as a civil and criminal conversion of the money that is owed to me.

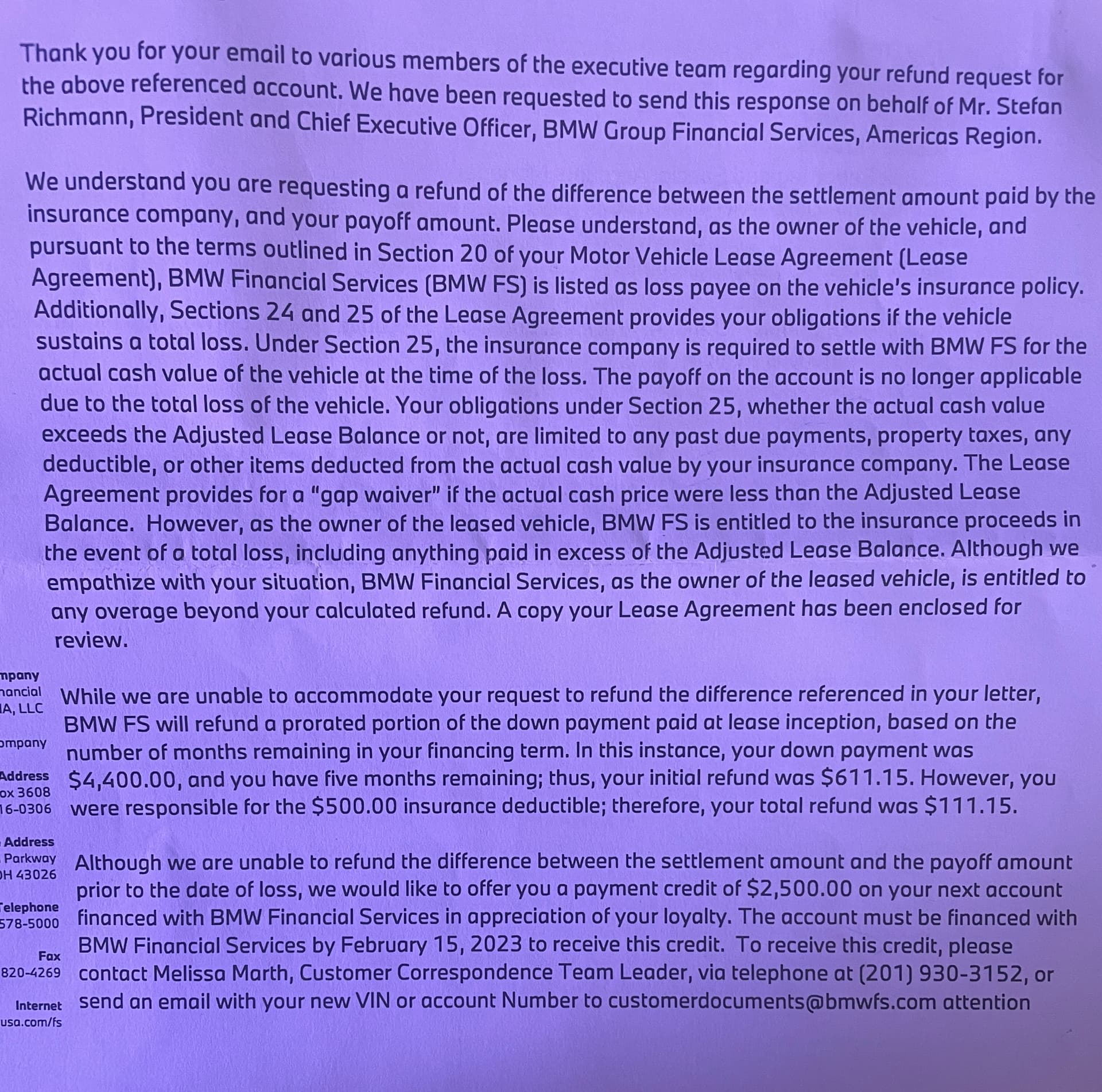

First, nowhere in Paragraphs 20,24, and 25 is there a single word that addresses the issue of a gain or overage between the buyout amount of the vehicle and the current cash value of the vehicle. Specifically, paragraph 25 speaks ONLY to a “Gap Waiver” in which the cash value of the loss vehicle is less than the lease buy-out amount. Even BMWFS Guaranteed Auto Protection Plan pamphlet (copy attached) speaks to paragraph 25 as ONLY a gap payment waiver in the case of a total loss. BMWFS has failed to indicate any paragraph in my lease that gives BMWFS the right to retain the gain or overage when the cash value of the vehicle exceeds the buy-out amount. BMW’s response that “Your obligations under Section 25, whether the actual cash value exceeds the Adjusted Lease Balance or not, are limited to……” is nothing more than an opinion of words that do not exist in Paragraph 25.

Secondly, they are unable to cite and state the law (or for that matter what paragraph in my contractual lease agreement) states that (1) “the payoff on the account is no longer applicable when there is a total loss of the vehicle”, and (2) “as the owner of the leased vehicle, BMWFS is entitled to the insurance proceeds in the event of a total loss…”? As a matter of fact, BMWFS in their letter to me of December 21, 2021, stated that all BMWFS was seeking, with full knowledge of the fact that the vehicle was totaled, was the payout amount of $28,069.50. Just by that one communication to me, they have admitted that I am entitled to the difference between the cash value of the vehicle ($40,740) and the buy-out of the vehicle ($28,069), or $12,671.

BMWFS offer to settle this matter for $2,500 towards a future lease of a BMW with BMWFS, based on everything that has happened in this matter, is a total insult to my intelligence and was rejected.