Nope. Looks like you forgot to divide by 2.

14441.28 /36 = MF x (96916.50 + 66153.30)

MF = .00246

I did confirm all the dealer’s calculations manually and they are correct.

FWIW-

All data should be vetted such as acquisition fee, doc fee (regulated by some states), cost of money (e.g., money factor), gov fees, residual, rebates/incentives, sales tax rate, etc. Make sure the residual matches the term and annual mileage requirement. Check available tax credits/incentives via the fund provider who may cover taxes or, at minimum, may assess a lower sales tax rate to energize sales for some models (e.g., Texas).

Organize all relevant data with the goal of creating a lease proposal that reflects your target deal. The idea is to create your own target deal (proposal), not replicate the dealer’s deal.

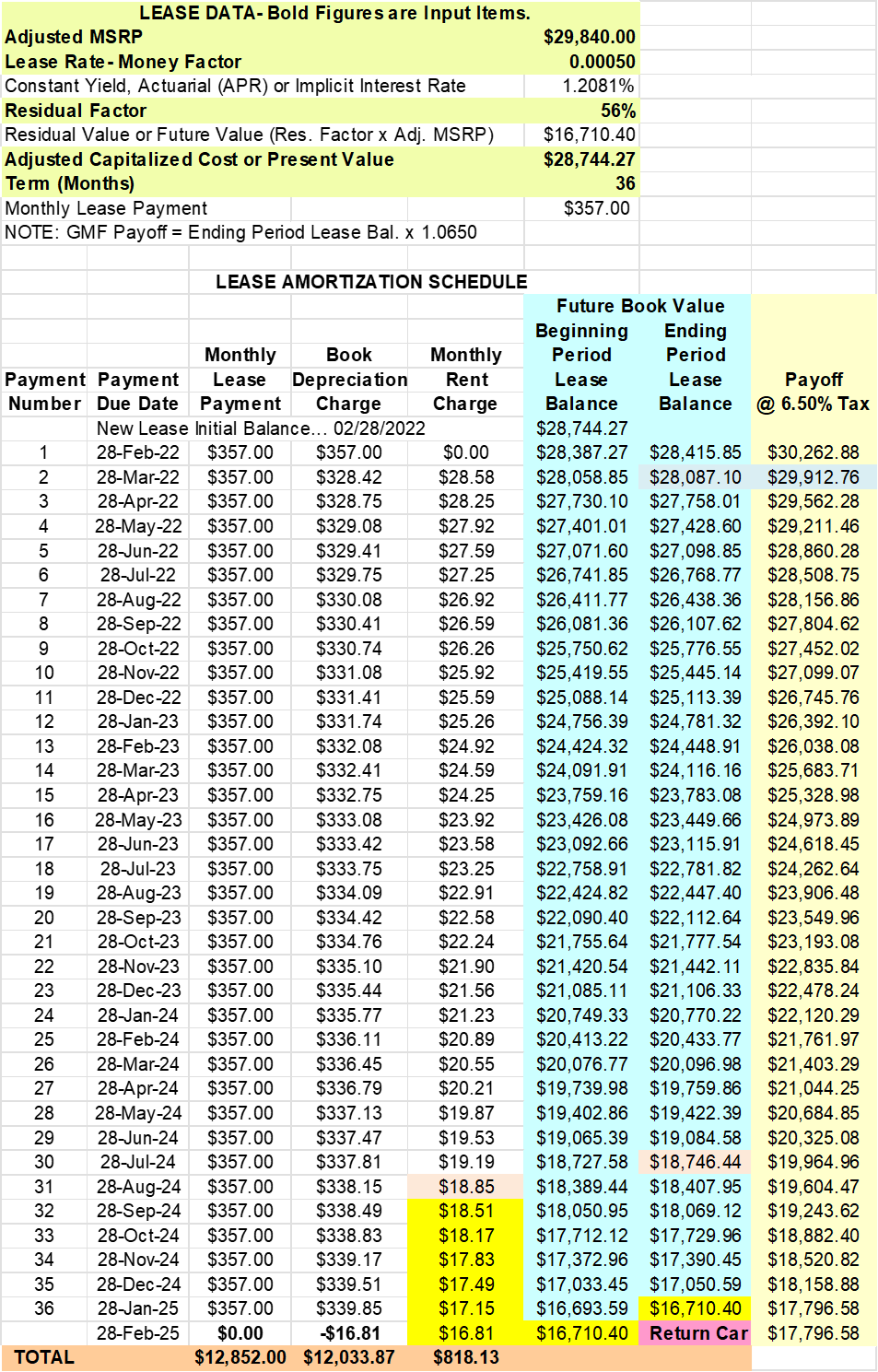

Craft a lease proposal (example below- the round peg, round hole won’t work) and email it to the sales manager (SM), not a floor salesperson as they’re often Mickey D order takers and lack knowledge. Be sure to contact the SM first to let them know you’re emailing them a one-page lease proposal b/c you want to close the deal ASAP. Be nice but firm. Unless they’re very stupid, once they see your magnificent proposal it will speak volumes. They’ll immediately know it’s time to put away their toys and Crayolas b/c it’s time to get down to business absent all the BS.

All numbers must be accurate otherwise, you’ll lose credibility. Negotiate via phone/email. Once an agreement is reached, ask the dealer for a review copy of the lease agreement and all contract addenda BEFORE you go to the dealer and sign. Moreover, it’s helpful to know the terms and conditions of the lease contract such as early termination liability criteria and purchase option criteria as well as lease amortization methodology and excess wear/tear criteria. If all is as agreed, tell the SM that you’ll come in to sign asap. You don’t want any surprises or dealer excuses like …. Oh, we made a mistake. That’s unacceptable and shouldn’t be tolerated.

If the dealer isn’t transparent or is uncooperative or showing signs of incompetence, WALK AWAY AND MOVE ON!

Leasing is time-consuming and requires a good deal of study and attention to detail. If you don’t have the time to commit, perhaps your best alternative is a good broker. There are some outstanding brokers on this website. However, if you’re willing to commit your time and resources, be sure to always control the deal. That can only be achieved with education which breeds confidence and increases the likelihood of success.

??? Let me know.