I really only wanted GAP and Oil change / tire rotation.

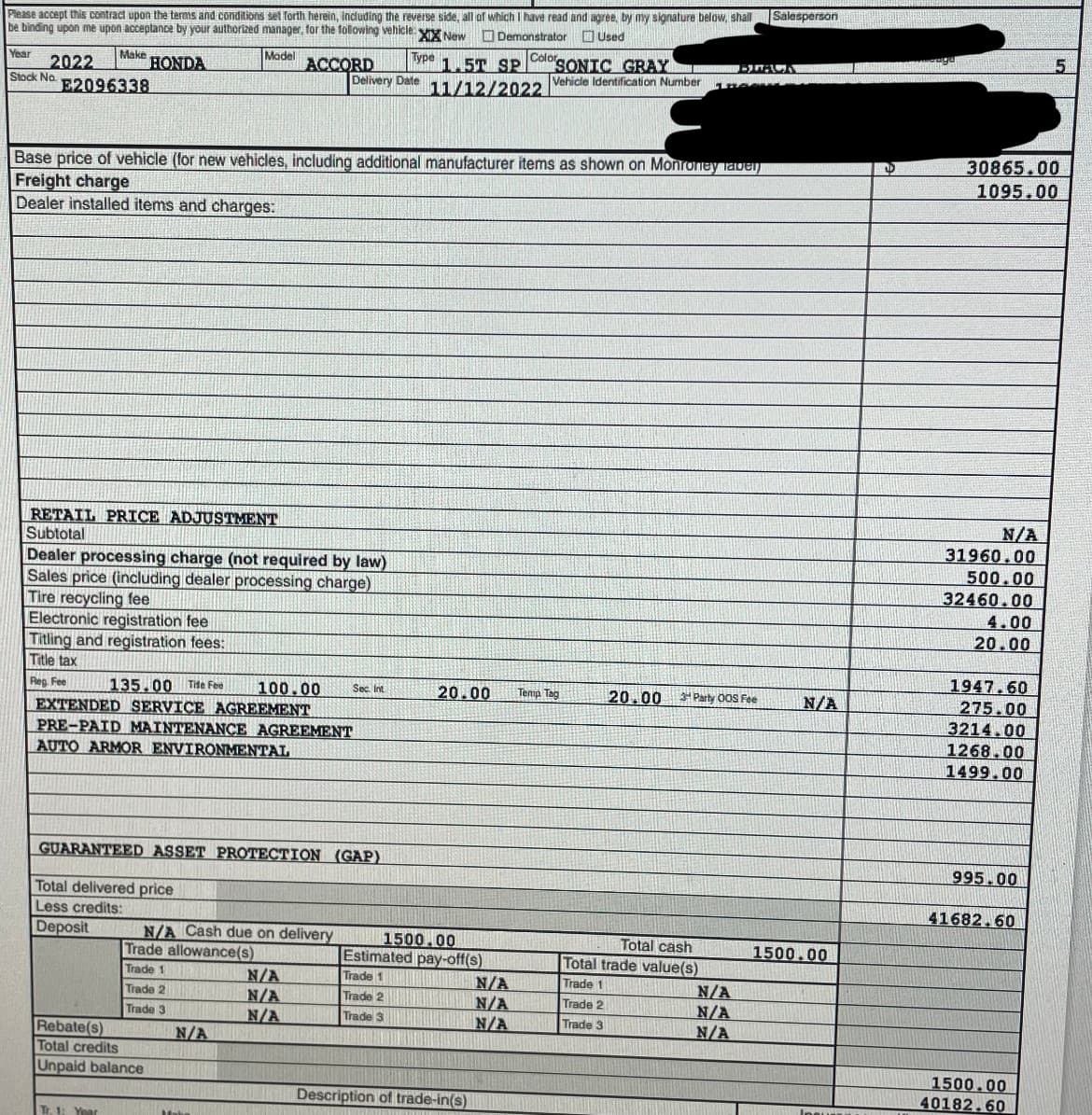

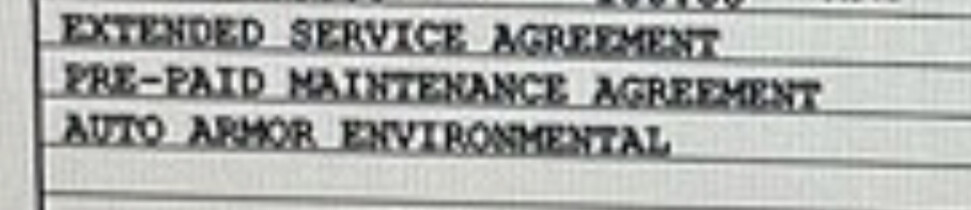

But they said they couldn’t do that and it was a package deal, had to get GAP, Oil change package, some 10 year 100k mile service contract (forgot what it even covered) and basically a ceramic coating (don’t think they even did the undercarriage).

Was going to put $1000 down, payment was $511 per month (doing bi-weekly payments though).

But after this bundle, the payment went up to $588.xx or $598. So I put $1,500 down and the finance manager said it would $270 bi-weekly.

But when I get home to look over the paperwork it’s $584.36 per month ($292.18 bi-weekly).

Should have walked. “Package Deal” was a lie. Not sure I would pre-pay for Honda maintenance either, that’s never been expensive for my Honda’s every 10k miles so I’d rather set that money aside and not pay the finance company the amount every other week

Might have to look at the add on contract, respectfully did you not look when you sign, and noticed the discrepancy in payments stated and contractually?

It was all done electronically, and the finance guy said it was going to be $270 bi-weekly (with $1500 down). Guess I should have asked him to show me on paper first lol.

You should have paperwork for each add on. Call the toll free #’s on each. On your pic it says JM&A fidelity so that’s probably it.

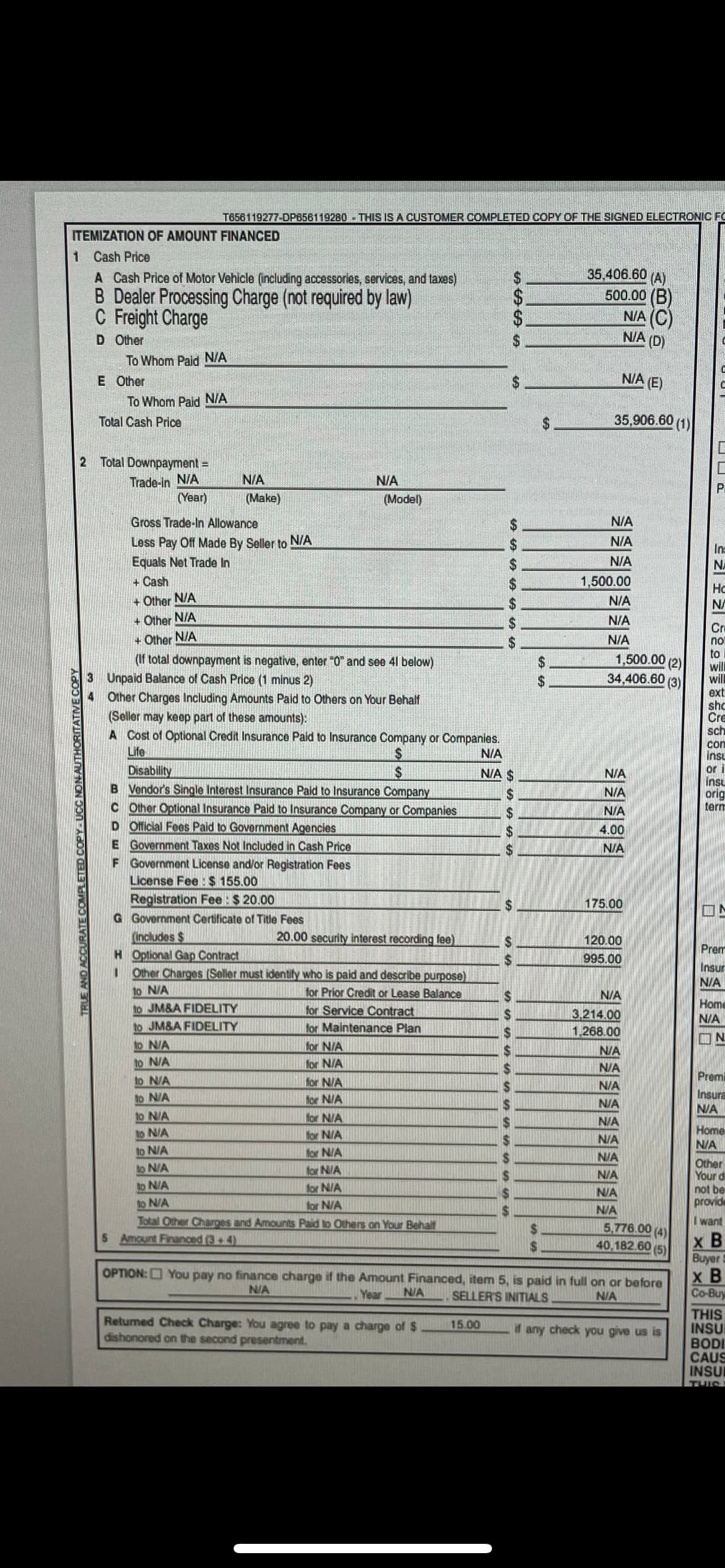

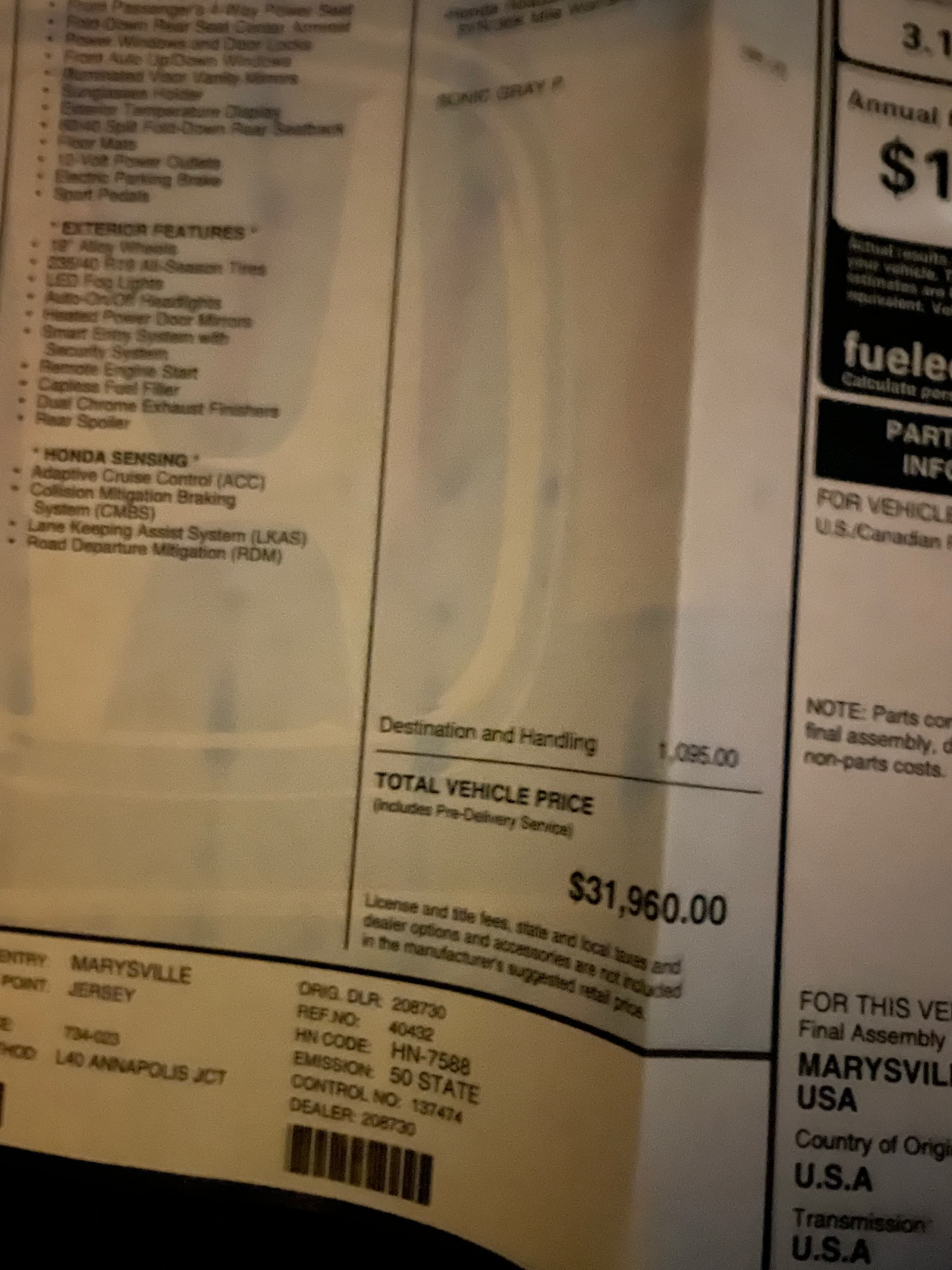

Edit: I looked at your contract again and it looks like they added freight to your total. Freight (also known as destination is already in the msrp. Do you have a window sticker or know the msrp)

They put you into a 7-year loan. In general, the longer the term the higher the rate.

It looks like you were bamboozled, hoodwinked and hornswoggled because you were shopping by payment.

(Lesson for next time, don’t do that. It’s among the most certain ways to get ripped off, and mentally splitting the monthly into bi-weekly halves for “affordability” probably quadrupled the chances of that outcome.).

Shopping by Payment on a Lease usually a smarter way. $0 down 36 months, shopping by payment means you know what you are getting. Hard to hide add ons except by changing the Down and Term but those are obvious on a lease.

The best way to know what youre getting is to actually know what youre getting, not look at a post-calculator number thats presented in a manner intentionally designed to make large cash flows feel more palatable.

Delivery Date is 11/12 — tomorrow is day 3 of the cancellation period. Go into the dealer and cancel all of those add-ons. Not sure about your state but you can usually unwind it within 72 hours or at least within 30 days with no charges (but refund applied to loan balance and not monthly payment).

For refinancing, check out other credit unions. There is a thread here but I’d recommend at least checking out Interior Federal Credit Union if your Equifax FICO 8 is > 720.