Signed this contract last June and I noticed there’s some bad math on this Ally lease contract for a Kia Sorento, that results in Ally collecting an extra monthly payment. I’m wondering if this is something systematic, since I believe the details are mostly generated by Ally’s software and difficult to notice (at least for the customer). This may only apply to deals with rebates (in my case the pass-through EV rebate).

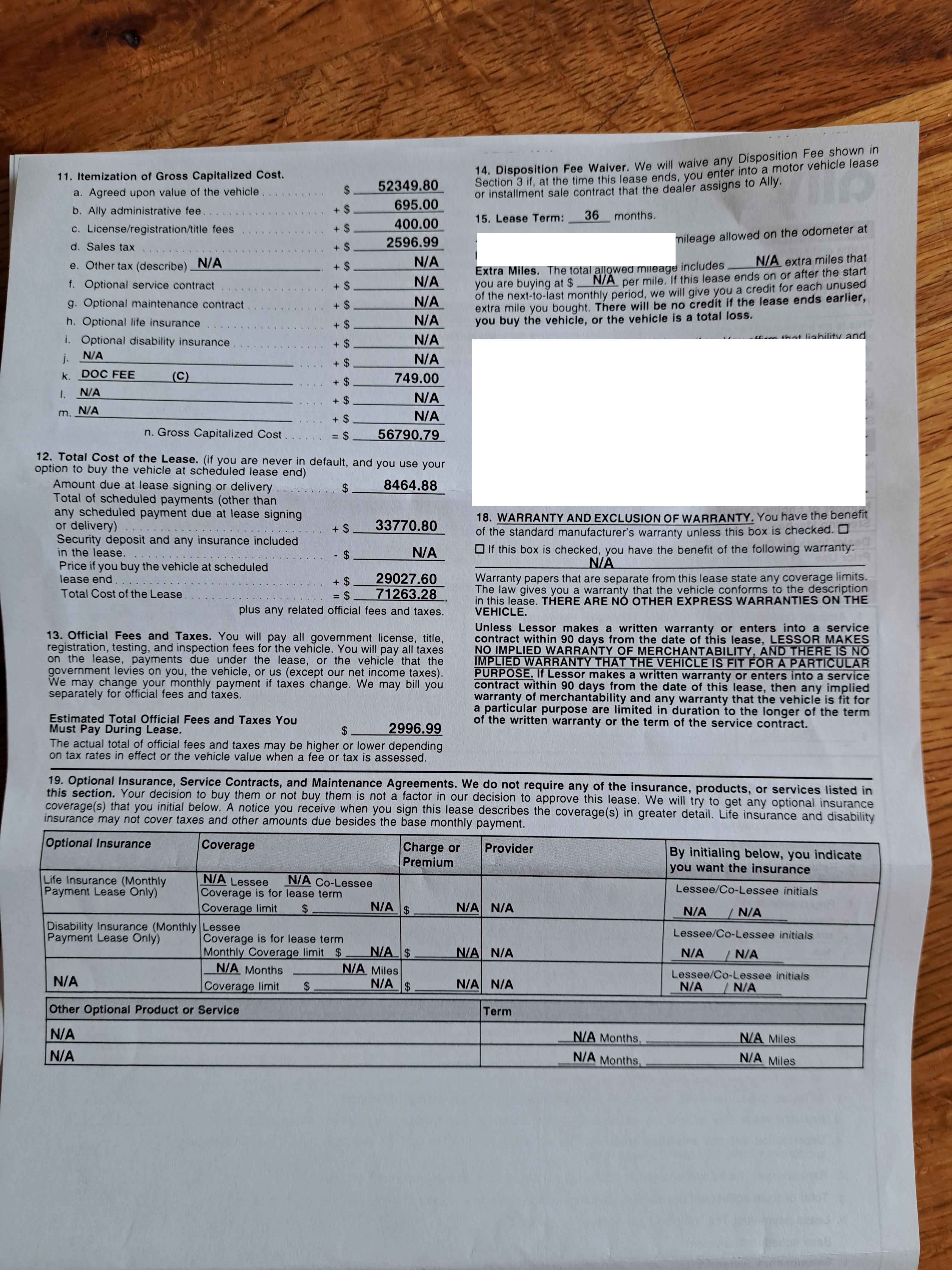

The problem is that the “Amount Due at Least Signing or Delivery” in line 5k is $7500 but then in section 12, the line that is also called “Amount due at least signing or delivery” shows $8464.88. Section 5 indicates that the first monthly payment is being covered by the rebate, but the amount in section 12 adds an additional monthly payment on top of the $7500 to get the $8464.88. They did in fact collect that first monthly payment up front.

This is wrong, because the “Total Cost of the Lease” in section 12 should equal gross capitalized cost + rent charge, $70298.4, but instead shows $71263.28 which is exactly one monthly payment more.

I’m sure this would be very easily missed by the customer so asking if anyone else has had or seen this issue where “Amount due at least signing or delivery” in different in 5k vs line 1 of section 12.

The fact that it says $0 cash due at signing and they collected a due at signing amount is what makes this wrong. The section 12 stuff is only secondary.

According to the contract, you owe nothing upfront. My question is: How much, if any, did they collect from you at lease signing? The 7500 rebate is supposed to cover the cap reduction and your first payment. All other charges are capped in the lease. So, nothing should have been collected at lease signing as the REBATE covers the upfront charges. Regarding Section 12, I have to agree with you…

7500 (rebate) = 6535.12 + 964.88 … this is how the 7500 was allocated (Sec. 5)

plus

35 x 964.88 = 33770.80

plus

29027.60 purchase price @lease end

TOTAL = 70298.40 …

Total cost of the lease are those costs paid on your behalf (e.g., rebate) plus your total out of pocket costs.

Another concern is (1) How much of a dealer discount, if any, did you get off the MSRP? and (2) Do you realize that you’re paying an 11.190% interest rate? I believe Ally uses an interest rate, not a money factor. If you compute the money factor on this lease it’s a funky 0.00473254. That is not a credible money factor which lead me to believe that an interest rate was used.

Don’t know your dealer discount but I believe you may have gotten hosed on the interest rate. In case you’re interested, below is the formula for the payment…

Where:

P = Monthly base payment i = Per Annum Lease Rate/12 Adj. Cap = Adjusted Capitalized Cost RV = Residual Value n = Term (months)

You may notice that the exponent, n +1, appears underneath RV in the formula instead of just n. That’s because Ally discounts the RV one month nearer to the present for some unknown reason… it’s a rip-off because it artificially lowers the RV. At least, that’s what they used to do and, apparently, they still do. There is no other interest rate that will give you that payment… it’s unique.

Questions? Let me know.

EDIT 1: corrected a few grammatical errors.

EDIT 2: BTW, artificially lowering the RV raises your payment by a few dollars.

EDIT 3: 6.25 to be exact.

One other thing and, for what it’s worth… Sections 1 thru 4 describe your total monetary obligation under the Fed’s Consumer Leasing Act AKA Reg. M and NOT Section 12. The 8464.88 in Section 12 is clearly a mistake as it fails to recognize that the 7500 covers the 1st payment and the 8464.88 double-counts the 1st payment as well.

Everyone saying it’s horrible lease, thank you you’re correct (though that $71k total cost includes the rebate amount so it would in fact be 7500 less than that if held all the way through and bought out). But the point was to get the $7500 rebate and then buy it out right away, which is what I did. Back in June MSRP was the lowest you could get them.

The only issue to solve at this point is the extra monthly payment they charged up front, which they clearly shouldn’t have. At this point the only thing I can think of is to take Ally to small claims court (hopefully there’s an easier way but calling them repeatedly hasn’t worked), but if they do this to everybody then it could be a bigger case and I’d rather they not get away with it even if I get my own money back.

Anyone leased through Ally with an EV/PHEV rebate and NOT had this issue?

If Ally did charge him the 1st payment at lease signing, then they owe him that money. It’s crystal clear that he didn’t owe anything upfront. The only sections that matter are 1 thru 6. Section 12 doesn’t mean do-da. OP should not have paid anything at lease signing.

Section 12 is the whole issue, if you say ‘ignore section 12’ then OP’s argument is invalid.

Every lease has the 1st payment baked in (look at yours, if 36 it says 35, if 24 it says 23 payments), so other than a wrong amount on the wrong lines on section 12, there is nothing wrong with this lease.

Sections 5 & 6 tells you that nothing is due at lease signing because the 7500 rebate covered the upfront charges (cap reduction plus 1st payment). All remaining fees were capped (see Section 11). Section 12 doesn’t mean anything. What matters most is sections 1 thru 6.

Your experience shows why it is so important to be in control of the deal. Do your research and submit a comprehensive professional-looking one-page lease proposal and it must be dead-on accurate; otherwise, you lose credibility. Never ever let the dealer control or dictate. This requires knowing how to calculate payments and residuals. I wouldn’t touch Ally with a 10-foot pole. It’s your responsibility to collect and vet all relevant data (acq. fees, doc fee, cost of money (e.g., money factor/interest rate), residual factor, etc.) before creating your lease proposal like the one below…

Before I go to the dealer to sign docs and pick up the keys, I always ask the dealer to send me a copy of the completed lease agreement as well as the lease worksheet to ensure that there are no mistakes or surprises. People get screwed because they lack knowledge or haven’t done their due diligence. KNOWLEDGE IS POWER.

Finally, as @trism said, get on leasehackr and ask questions BEFORE you sign a lease agreement. Always helps to have several qualified pairs of eyes scrutinizing your research and proposal. We would be happy to review your lease proposal. Lots of talented and smart folks on this website. But you need to do your homework first. GOOD LUCK!

No, it’s not. OP has Sections 1 thru 6 to fall back on. That’s his proof that he owed nothing at lease inception yet, he was told to pay the 1st payment which was already covered by the 7500 rebate (section 5). He should have a receipt for that 1st payment he paid at signing.

I agree with you. The issue is that, apparently, the dealer collected the 1st payment from him at lease signing. The lease agreement clearly shows that nothing is due from him… nothing due out of pocket. If OP claims that he paid the 1st payment out of pocket at lease signing, the first thing I’m going to look at is sections 5 & 6, not section 12. Sections 5 & 6 alone tell you that he should not have been charged. That’s his argument.

He never claimed that, he said they did collect it…different words. They paid his first payment from the rebate.

If he said I wrote them a check for $968 and they have no record of it…well then I wouldn’t worry about section 12 and start looking at the rest of the contract.

Did you pay the 1st payment out of pocket when you signed the lease? I got the impression that you did. If not, no harm, no foul. You have no claim against Ally.