I am in Portland, Oregon. I just leased a 2024 Subaru Forester Sport

I thought I had a good deal worked out. Read everything in the finance office, but then they had me sign on a tablet. Reread, but my eyes aren’t what they used to be.

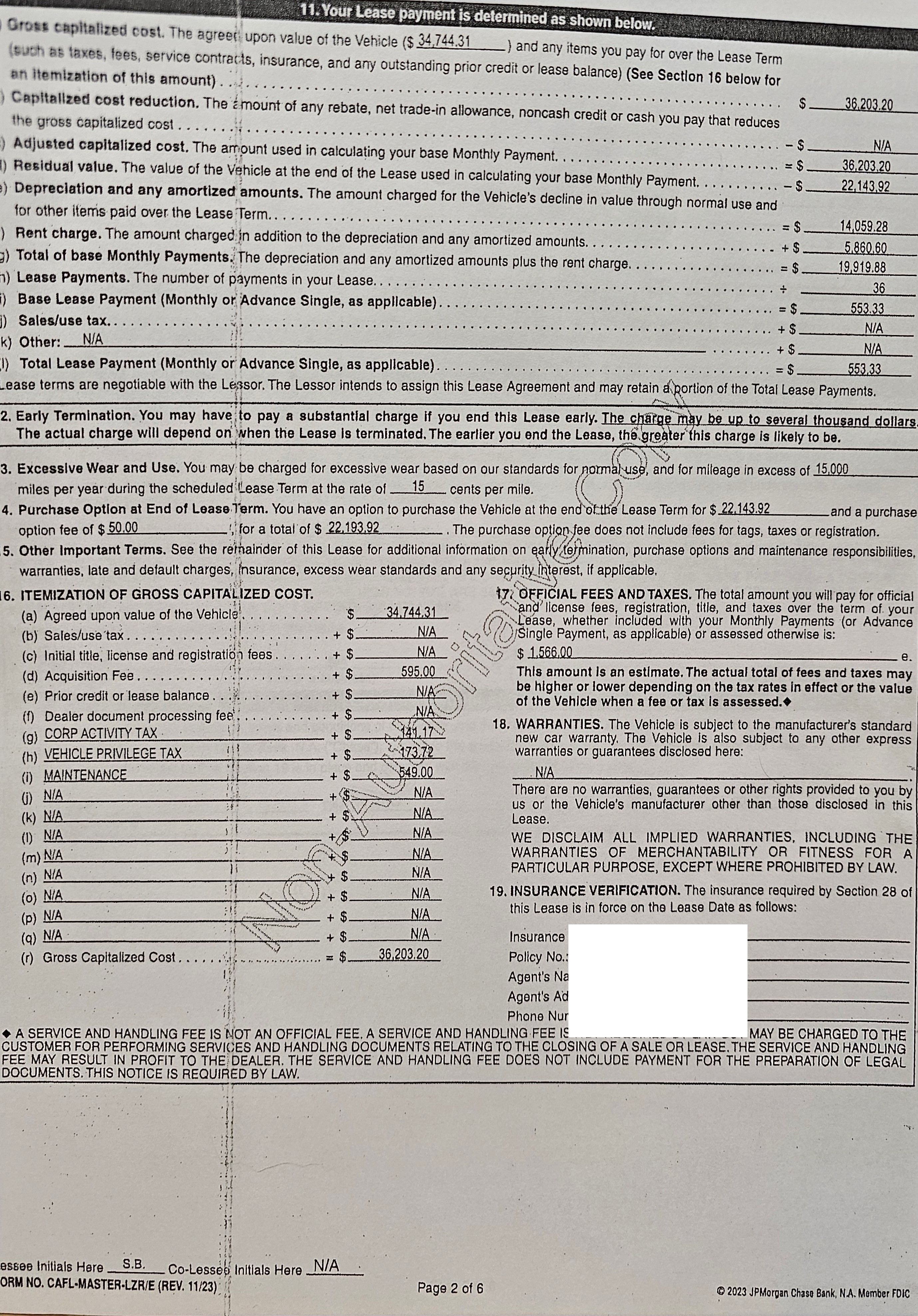

Here is my offer sheet. Adjusted price was the 7% off I was going for. Dealer claimed it was invoice price. I verified this by asking for the invoice. It was provided on the spot.

Agreed upon price: 33216

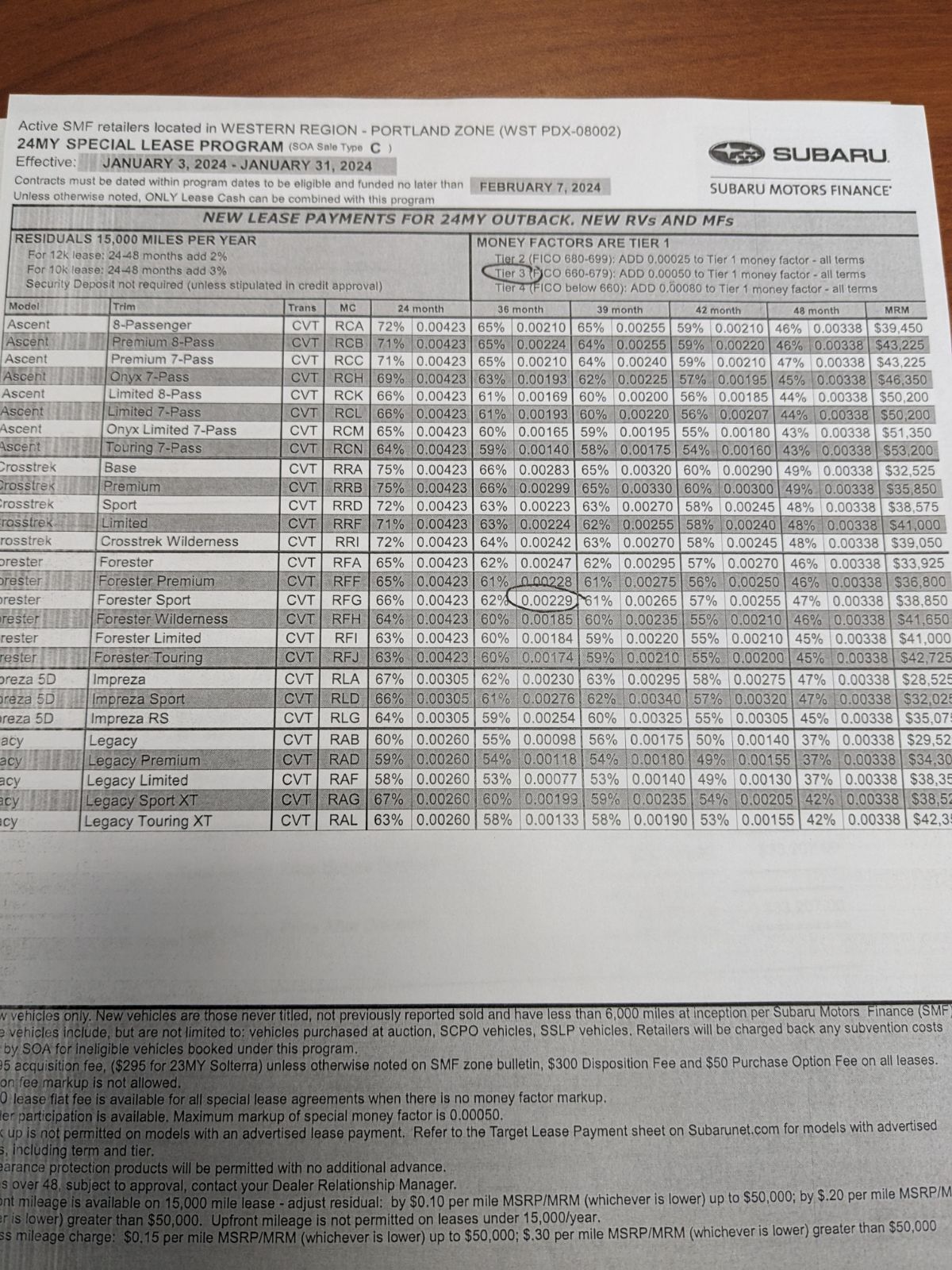

Money Factor: .00229

Credit came back at 721. This offer is a tier 1 offer as far as I can tell. I was happy with this.

The first thing I asked the salesperson was what the MF was. It matched with the expected number.

They came back to me and said they were struggling to get financing approved. did not expect my credit to come back that high. I believe it’s closer to 660, and I expected tier 3. Gave them some paperwork they asked for. Was given a second offer, this time at tier 3. MF still looks good. Payment went up, but the MF was exactly what it should be, tier 1 + .00050.

Asked them to roll in all the costs possible. Expected to owe first month at delivery.

While signing I see $1431.33 due at signing. I ask about this. I was told “We are covering that.” I should have questioned this more, but I didn’t.

Now on the lease the payment and residual is where I expected it to be. Only bought the lifetime oil changes for $549, after talking it down from $599. What I didn’t catch in the office was that they changed the agreed upon price to make this work somehow. However the lease still says $1431.33 drive off.

I don’t understand what they did, and honestly I am not sure if they gave me the money factor I was promised. .00279

I cannot get this to work in the calulator at all. I can get really close, but only with a marked up MF.

Now the end result is I have the payment I expected, and I paid zero before leaving. I don’t know, it just doesn’t sit right. Help me understand these lease please?