This is the first time I am leasing a vehicle. So pls excuse any errors below.

Promo: Lucid September $549/mo lease deal on lowest base model (Ends Sept 30th 2024)

$7500 Pure credit ; $7500 Lucid EV credit ; $5000 onsite model = $20K in manufacturer credits

Plus, used a random owner Referral code for $750 referral credit

Total incentives = $20,750

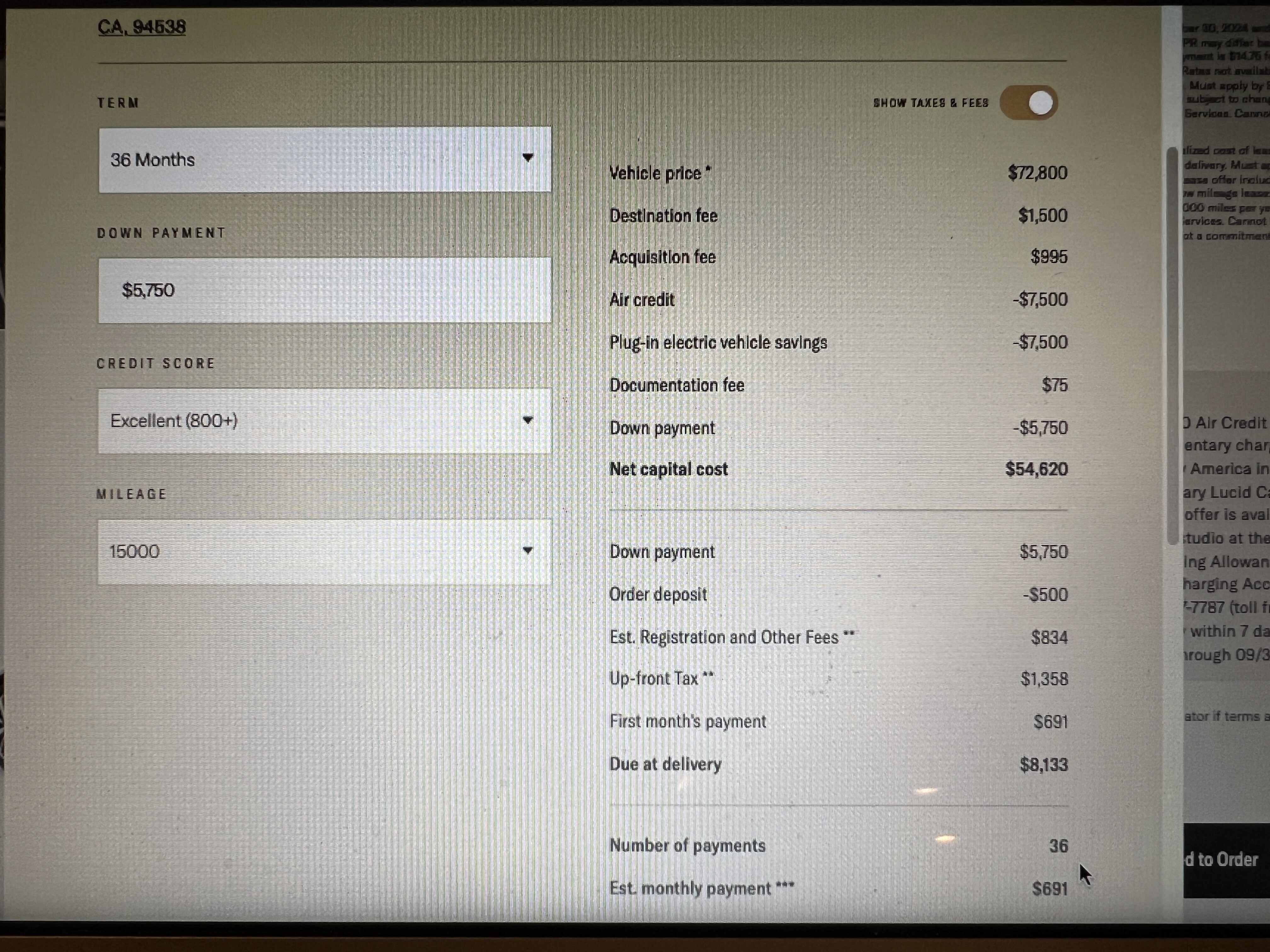

2024 Lucid Air Pure base “onsite” model, White ($59,900), Surreal Sound Pro option ($2900) = $72,800 MSRP. A $500 deposit was paid to secure a VIN number. (Original deposit)

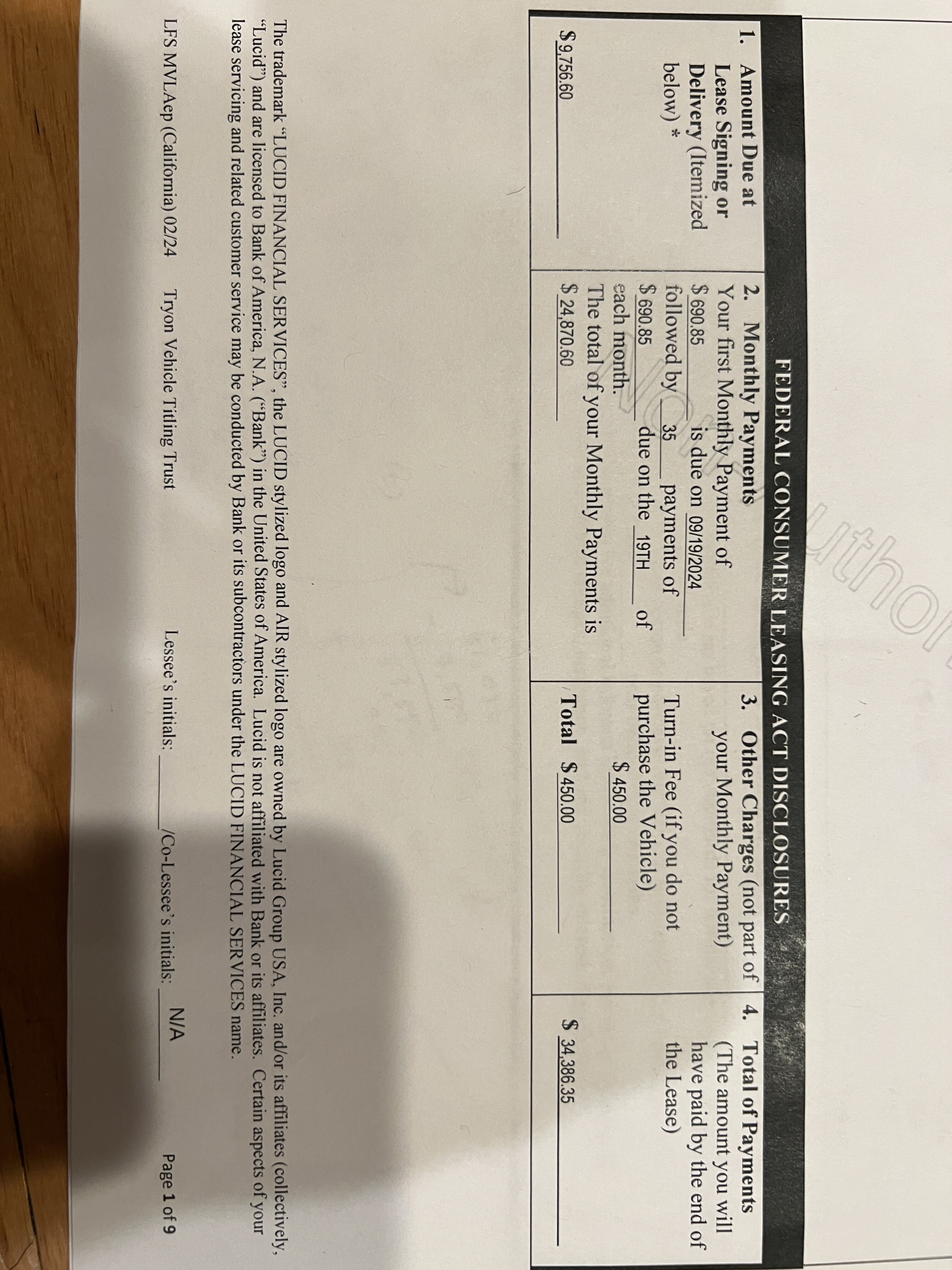

Zero down; 36 months/15K miles computes to a $690/month incl. CA taxes all in.

I have no idea what the Money Factor is. Can someone pls help?

Also, there are 2 identical $7500 value credits which I cannot tell which one is used where in the math calculations. I am simply hopeful the math all adds up taking into account credits totaling $20,750 fully amortized in this lease deal. Pls help to verify the math.

HELP: Also don’t know how to input all the numbers in the Lease Calc Can someone please describe the steps to input into the respective fields?

The Lease Math looks like:

72800 MSRP + 1500 Destination Fee = 74,300

(Q: Why did they add the dest fee to the MSRP??)

7500 Pure credit (Cap Cost Reduction) + 5000 onsite credit + 750 referal = 13,250

(74,300 subtract 13,250) = $61,050 which is the “Agreed upon value of vehicle”

NOTE: The Gross Cap cost is $62,120 ($61,050 + 995 acq fee + 75 doc fee)

Now, applying:

7500 EV credit ; 61,050 - 7500 = 53,550

+995 acquisition fee and +75 doc fee = $54,620 which is the “Adjusted Cap Cost” - the amount used to calc the base monthly payment.

Residual Value = $32,469.10

Depreciation & any amortized amounts = $22,150.90

Rent charge = $407.42

Total of base monthly payments=22150.90 + 407.42 = $22,558.32

(Divided by 36 months) = $626.62

(Add Sales Tax) = $64.23

Monthly payment = $690.85

Purchase option end of lease = $32,469.10 and purchase option fee of $450 plus official fees and taxes.

The math for the “Amount due at signing”:

Cap cost reduction = $7500

1st month pmt,rego,cap cost reduction tax, filing fee, lic fee, tire fee = $2,256.60

Rebates and non-cash credits = $7500

I am total confused with this section, but he said $2,256.60 which is DAS (-) $500 original deposit = $1,756.60. Just make a cashiers check for this amt $1756.60, due at Delivery.

Thanks for any insights and any explanations, and help with data input into the Lease calculator.

I have no idea what the Money Factor is. Can someone pls help?