No need to bump two different threads with the same

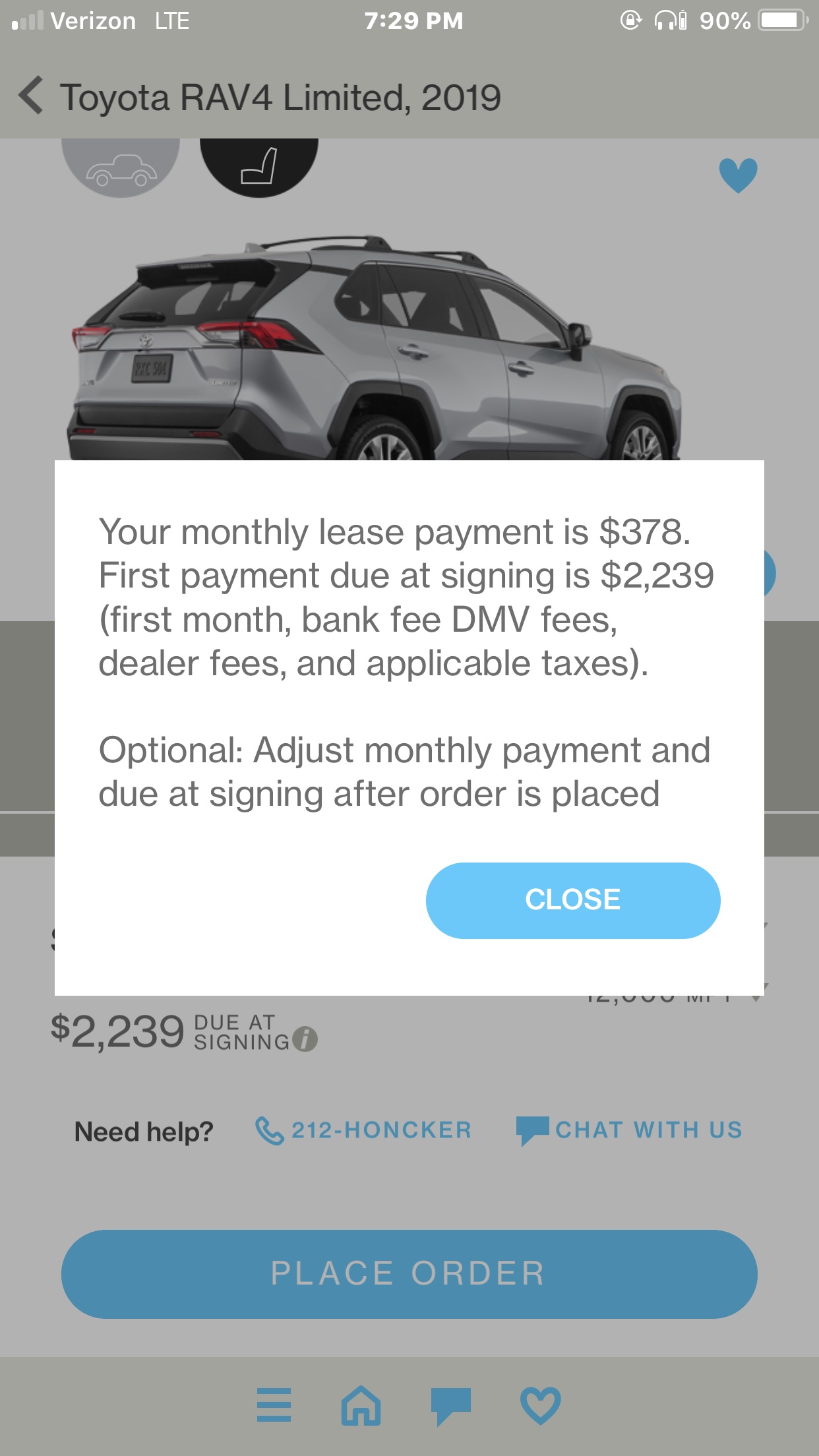

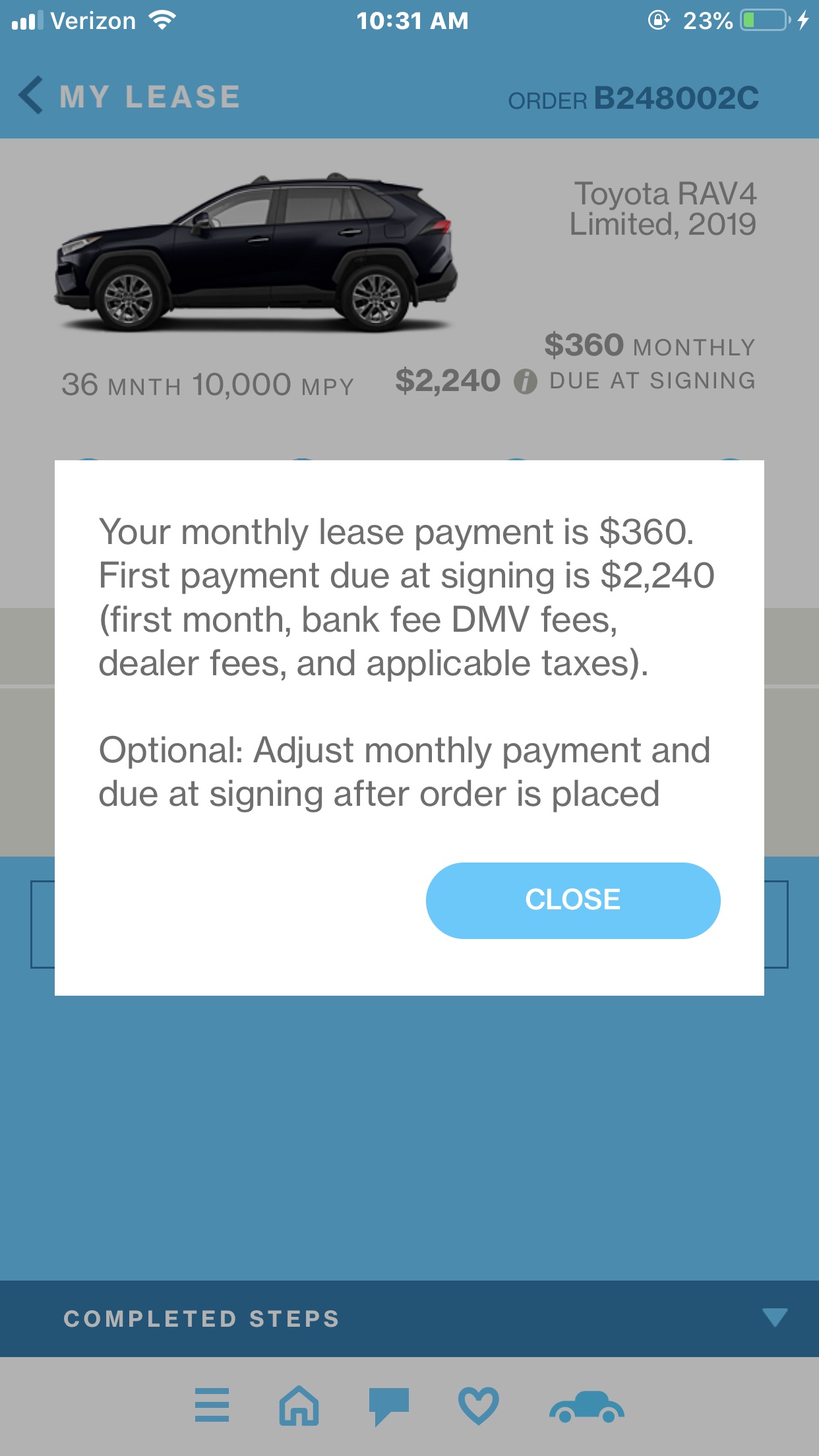

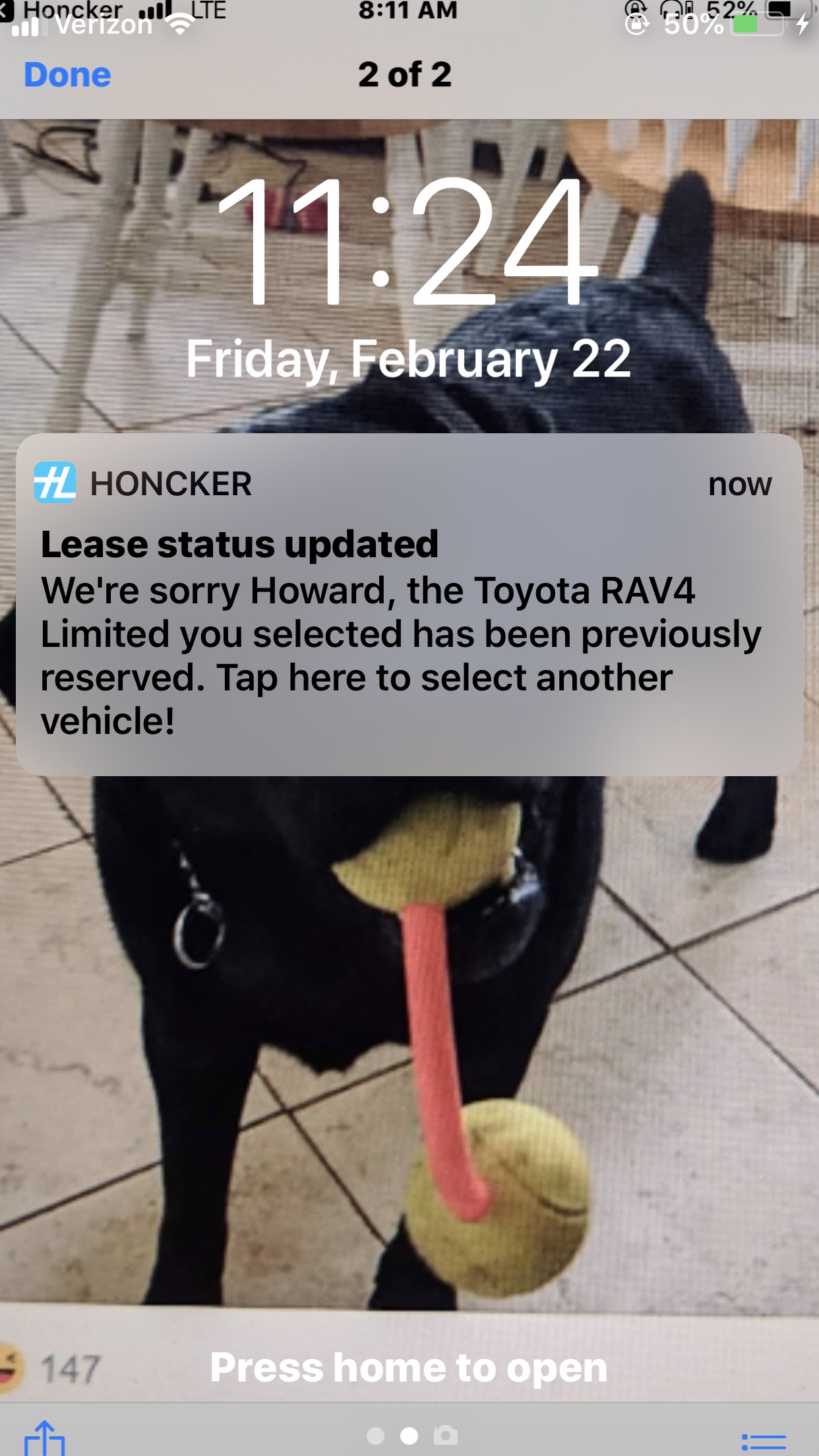

Very similar thing happened to me a few weeks ago. Ordered a car (impossibly low price listed) for a 2019 RAV4, which there are no real “deals” on because it’s so new. Was told car was reserved and processing. Credit score 800+. About half an hour later was notified that the car I chose had already been taken by someone else. So I chose another one and placed the order. Shortly thereafter I received a phone call saying most aggressive price dealer could do was about $40 more PER MONTH with same amount down. Asked why and he said prices listed are NOT actual prices, but the best price someone else was able to get. Told them their site was a scam and deleted app. See pics below.

2 Likes

This is crazy! I would be so pissed if someone ran my credit and raised prices.

2 Likes

They do not run credit until a a deal is agreed upon. I tried the app and it was a complete waste of time. I placed an order and was told the price would be much more but I confirmed the process with Honckr and credit isn’t run until you and the dealer agree.

Which means there’s a possibility dealers can be deceiving clients who are at borderline credit tiers?

the thing is a colossal bait and switch.

1 Like

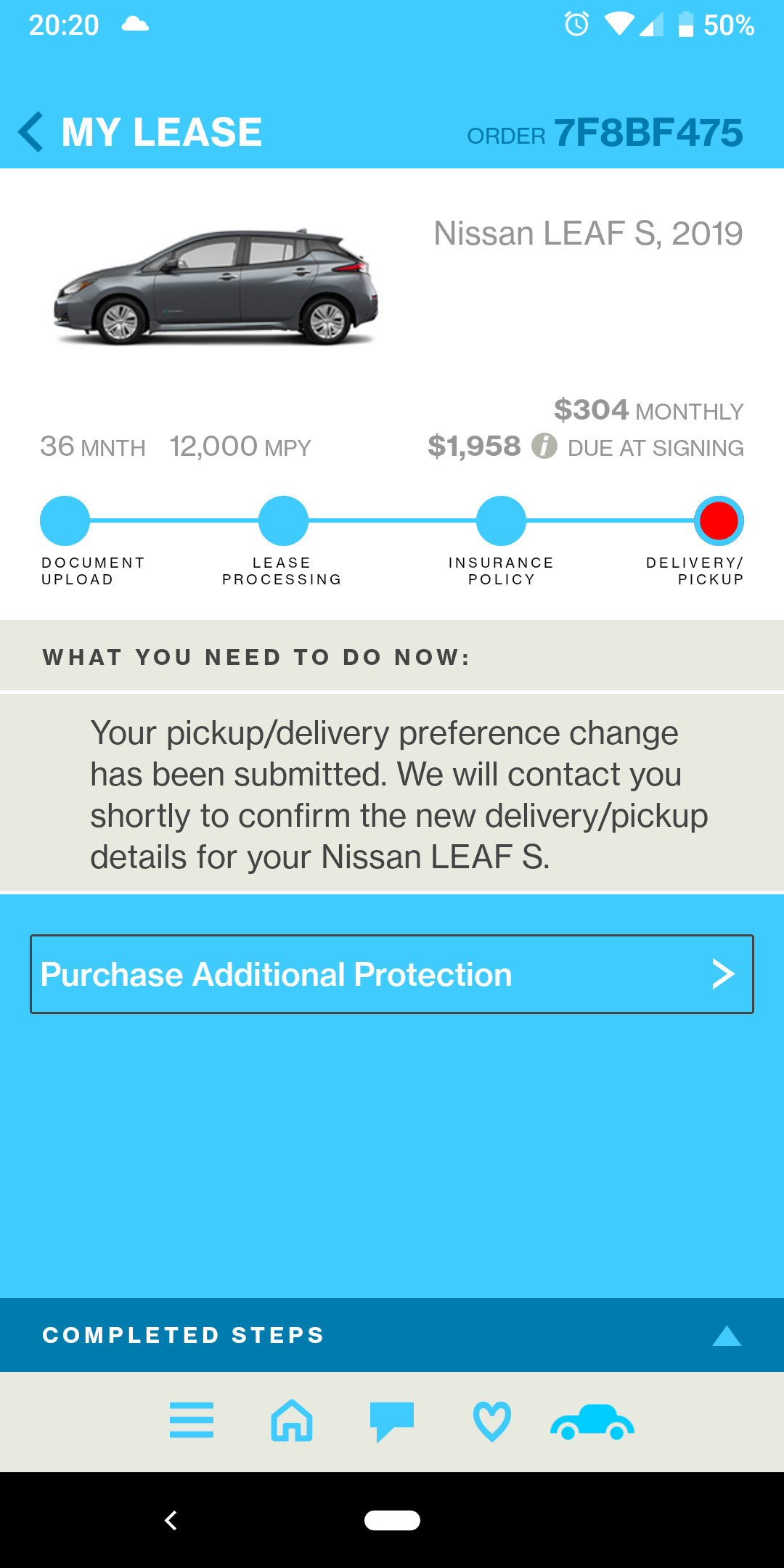

Last week I thought I found a great deal through the Honcker.com app. I’ve been in the market for a lease on a 2019 Nissan LEAF and thought I found this great deal.

The deal was:

Monthly payments: $304

DAS: $1958

I talked to a few dealers who all said it was a great deal and so I decided to take it. As soon as I clicked on the deal, provided all my personal information and uploaded my driver license my credit was polled. It was a hard inquiry on my credit. I checked my credit and saw a new hard inquiry. At the end of that day my order was just waiting to be delivered:

The very next day a customer representative named Ari Cohen called me to inform me that the deal does not exist. He was very rude and pushy trying to get me to accept the new deal which was now $330 a month before tax. I rejected and asked to talk to a manager. He said a manager will call me the next day.

After two more days where they have not reached out I called them back to talk to a manager who was not available to immediately talk. A couple of hours later one of the VP of Sales at Honcker called me. His name is Talles Guimaraes who again explained that the deal doesn’t exist. He further explained that this is a common situation and usually the customers like the new deal even though it isn’t what they accepted. He basically admitted to the fact that their business model is the classic bait-and-switch.

I tried to challenge the fact that my information was given to the dealer before they had approved the deal. Talles Guimaraes explained that it is how their system works (whatever that means), and they can’t validate every deal. I tried suggesting that they could have the dealer confirm the deal before getting the customers information, but it was obvious that the conversation wasn’t going anywhere.

In summary, the numbers on the Honcker.com app are either a bait-and-switch scam or simply not a good lease offer.

Avoid at all cost!

9 Likes

Did Ari post a middle school picture in his LinkedIn account?

3 Likes

Please retweet: https://twitter.com/ohad_benjamin/status/1110037200740052992

Sucks to hear. We have been waiting for months to get added as a dealer. The dealer does control the pricing so it’s up to them the be honest and upfront

2 Likes

While I agree that the dealer is responsible for being honest and upfront, it is my opinion that Honcker has the responsibility as the platform owner to enforce that. It would be extremely easy for Honcker to add to their API a final confirmation of the offer by the dealership before they get the information.

It’s a matter of caring about their customers’ personal information, which they don’t!

Ouch. I feel like the legal ramifications here are pretty big — sounds like this is a very common occurrence at Honcker. There is no way any company should be able to run your credit and then change terms of the agreement afterwards. Surely there must be someone smarter than me who can weigh in on this — I would be absolutely livid if they were running my credit and changing the terms afterwards. Especially if this is their status quo.

Is that even legal to make a hard pull without an actual willing to make a deal?

How is this different than the dealer pulling your credit before you’ve even settled on price? In fact isn’t it fairly common to check the credit early so they lock you into the 4 square game?

1 Like

There is difference between a soft pull and hard pull. Honcker clearly pulls a soft bureau – Dealers should have access to it. Pricing should always be locked in before a hard inquiry.

This is very troublesome. Many lenders have strict guidelines on hard pulls. A hard pull is done typically once pricing is agreed upon and funds are scheduled to be dispersed.

I guess people should use Honcker as a negotiating tactic.

Have you not read this thread? What’s the point of discussing fake prices that could be bait-switched?

4 Likes

I did use it as a negotiation tactic! What do you do when you’re told by multiple dealerships that they cannot match or beat that price? Would you not take it?

Well, you shouldn’t as it is a bait-and-switch, but I only know that now…

1 Like

Hi SC204, Make an offer is a new feature and we are still improving. When you place an offer, the dealer gets notified. They have the option to accept or counter offers. In some instances, it may take some time for dealers to respond. We recommend that your offers are reasonable, to improve your chances of getting a response. Have you heard back on your offer yet? If not, please PM me and I can investigate further for you.

Huh? To even get a response? So your dealers can just ignore what they consider unreasonable requests? Just like without your app.