How many accidents lead to requiring a new engine? Not a lot. But for EVs even small accidents can damage the battery which is a $15K cost to replace. That’s why it’s so much more expensive.

Except that isn’t really what the numbers show. The price to repair EVs has stayed relatively stable over the past five years while the price to repair ICE vehicles has gone up significantly. Data suggests that’s because EVs like Tesla were early adopters of many of electronic gizmos that are increasingly in even most new non luxury ICE cars. As ICE cars catch up technology wise, their cost to repair continues to increase.

There are also confounding variables that make simple answers much harder to determine. For example per mile driven it is significantly more dangerous for drive in the South than in New England. Perhaps that is partially because New Englanders are better drivers but it is mostly because the speeds are just much lower due to density. Since there are more bad accidents in the South would except repair costs to be higher per accident in the South. And that is significant since EVs are much more popular in New England versus the Southern States.

Most people are looking for a simple answer but the insurance companies, who have skin in the game, show us how complex the numbers actually are.

3 Likes

Your chart literally (and I’m using literally the literal way not the milenial way) confirms what I said. Non Tesla is $8K to fix on average, ICE is $5K. Gee I wonder if an EV costs 60% more to fix on average if that leads to higher EV insurance costs. It’s almost as if that’s what I said.

But no let’s go with your South = dangerous theory. LOL. That must also explain why EVs cost more to insure in Canada. Lots of Southern drivers there I guess.

EV fanbois have reached vegan territory in ridiculousness. You’re not quite at CrossFit level yet but close.

Maybe give the chart another look over. I think you might have missed the header. $8k yes…in Canada. The delta is $1k here

I included a citation from about the most reputable source available for American automotive data. Facts… something something…feelings.

1 Like

That’s still a 20% difference which is fairly significant

Of course. But in 2020 the gap was double that. So the question is why is the delta narrowing.

The research in the Mitchell international report (the company processes insurance claims) seems to indicate that the vastly different repair costs in 2020 was due to almost all EVs in 2020 being new so having all th fancy modern electronic gizmos whereas there were lots of older ICE cars on the road that were still easier to repair due to their simplicity. Now that cheaper ICE cars are getting more complex… .

EVs have a lot of issues, mainly difficulty selling without government incentives, but the repair cost situation may be something of a red herring. Issue may be more that any expensive car filled with electronics, regardless of powerplant, is going to be expensive to fix.

Received my 6-month “renewal” - went DOWN $5.76 same vehicle no other changes.

Earlier this week on a personal finance forum, someone questioned the need for UMI ![]()

I’m enrolled in their “certified mileage program” – which is not an OBD/GPS device but is verified using public data. This disclosure is new and the most detailed I’ve seen in one of my policy renewals.

Next renewal will have a different vehicle and undoubtedly be more, but nice to NOT receive an increase.

1 Like

Data point:

Just added my 2025 Tesla Model Y Performance as a 4th vehicle with 3000 miles driven per year and it is $452 for 6 months, my total for 6 mo for all cars is $1812

I have my 2022 Model Y LR as a 7500miles/year and that one is $641 for 6 months-in process of being sold in a few days

Mirai 3k miles/yr $398

Ioniq 5 3k miles/yr $322

After I take off the sold Tesla, I will tweak my mileage to 4K each Ioniq and Tesla, leave the Mirai at 3K and see what my quote changes to, I am in SoCal and CONNECT from Costco is the insurance

2 Likes

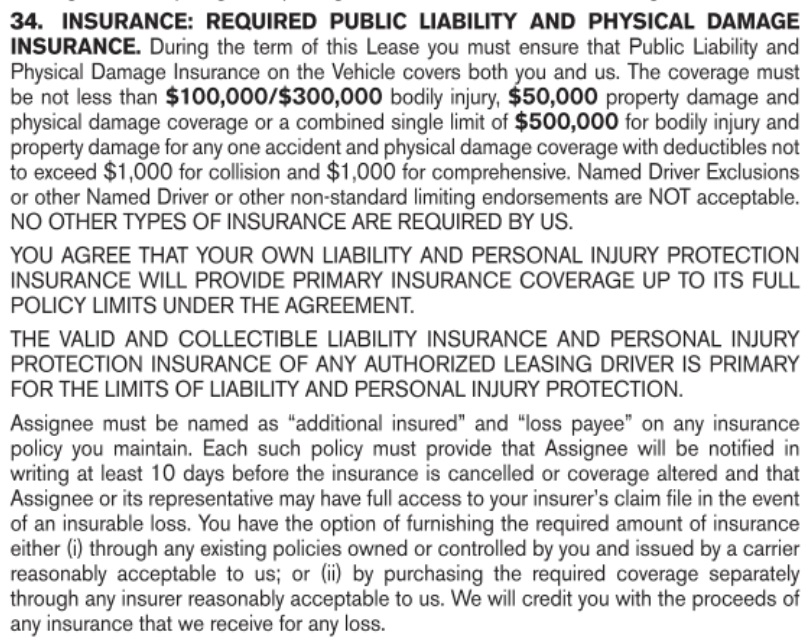

The Insurance clause of this lease contract is interesting:

IANAL but this reads to me like the stated limits have to be in your primary insurance policy (or does “You have the option” leave the door open for that?), and an Umbrella is ok but not required, as long as it is above these limits.

Also that you have to give the bank 10 days notice if you change insurance carriers or coverage limits, even if they comply with the stated limits (e.g. you didn’t have glass coverage and then add it). Understanding the “10 days notice of cancellation” is material change if there is NO replacement coverage, you are technically cancelling coverage if your change carriers. The insurance carrier and policy are included in the lease agreement that is signed along with the terms and financials.

Not surprised. I’m sure uninsured/underinsured is running rampant these days with all the increased insurance costs.

I fear the gotcha moment because right now it seems that only progressive is reasonable in MA. GEICO wishes to exit and their premiums went nuts. I just quoted Allstate and they wanted $5600/yr for the same limits I have with Progressive. I am going to quote Plymouth and Safeco, but $2800/yr for 2 cars with a clean driving record is nuts to me. Pre-Covid I was paying less than a grand.

Is it a death spiral where the higher prices get the more uninsured so prices keep going up? I make a very good living and the price doesn’t move the needle for me but I have a hard time believing that all the people I see driving around in late model, basic cars can afford $200+ a month just for insurance.

1 Like

Have you had an independent agent quote it? I have Safety and Quincy Mutual and both are pretty reasonable in MA.

Not yet. There’s not a lot of agents in this area that do anything other than Allstate and Commerce and both were nuts.

California owners, do you have earthquake insurance ? If not, did you pay to retrofit your home to minimize risk? It used to be around $300 per year, now $1000 plus.

You can get Earthquake insurance for only $1,000 a year?

I’m not on a fault line, not in a high fire risk area, with only moderate liquefaction risk. And earthquake insurance would have been like $10,000 per year. I’m just happy to have any home insurance at all.

If there’s another big earthquake, we’re all screwed anyway. 1 inch of rain will knock out power to tens of thousands.

EQ insurance in CA is somewhat of a scam. You don’t get 100% coverage for a loss and have a huge gap to fill out of your pocket.

I’m waiting for my quote from State Farm. It looks like a have a $65K deductible on what they have on their initial letter. On the CEA page you can increase different amounts of coverage. I’ll probably get it, because as one gets older, the risk aversion decreases.

1 Like

Rates from USAA, go figure:

Added $151k MSRP 2025 Range Rover, 6 month premium $547.26

Removed 2 year old BMW iX worth estimated $55k, 6 month premium $534.93

EVs are double.

Make sure to shop around as well. I left USAA years ago. They aren’t competitive anymore in my opinion. After 10 years or so I left. I believe that was 7 years ago? Last year I ran a quote with them when I was shopping around and they were almost $2k higher than Erie.

3 Likes