I’m wondering if paying off a lease early will eliminate some interest owed, can anyone chime in? I know for normal loans, unless you have a prepay penalty you could easily pay down the balance at an accelerated rate to avoid interest carrying. Is this true with leases? I have one with Ally and was wondering if there’s any benefit to doing it…

It’s my understanding that you run the risk of having too much invested in the car if it gets totaled. That said, I don’t think making early payments will affect the interest since you’re “renting” vs. paying down a loan. I could be wrong on all fronts, though!

2 Likes

What did Ally say when you called and asked?

4 Likes

I know what Ally is going to say, but spoilers…

1 Like

Most of the time the interest on the leases is very low, not worth pre paying in most situations

It’s actually highly variable depending on the make and model. Some leases the rent charge is huge compared to depreciation and vice versa. Can’t really generalize there.

3 Likes

On a 24 month tundra lease through Ally, a prepayment saves about $18/month in interest.

Only speaking from my current Tundra lease through Ally. Not a generalization about all of them.

2 Likes

Savings would be very minimal since lease financing isn’t structured around interest, they are not loans. What I have done with my last 2 leases is bank as many payments as I can into a high interest earning account and leave it on autopay. Earned interest still isn’t a lot on such a small amount but you do gain something and also have a cash cushion you could draw against in emergencies. Also there’s no risk of losing the money in the event the car is totaled compared to prepaying it.

4 Likes

Risk reward…def not worth it imo. I have people ask me for ally one pays all the time. While I’m happy to provide it for them, I never recommend it.

1 Like

Leases don’t amortize like a car loan does - your rent charge on the very last month is the exact same as the rent charge on your first month. I’ve never seen a lease agreement that allows you to prepay payments to save on the rent charge, I’d be surprised if any of them did anything like this.

2 Likes

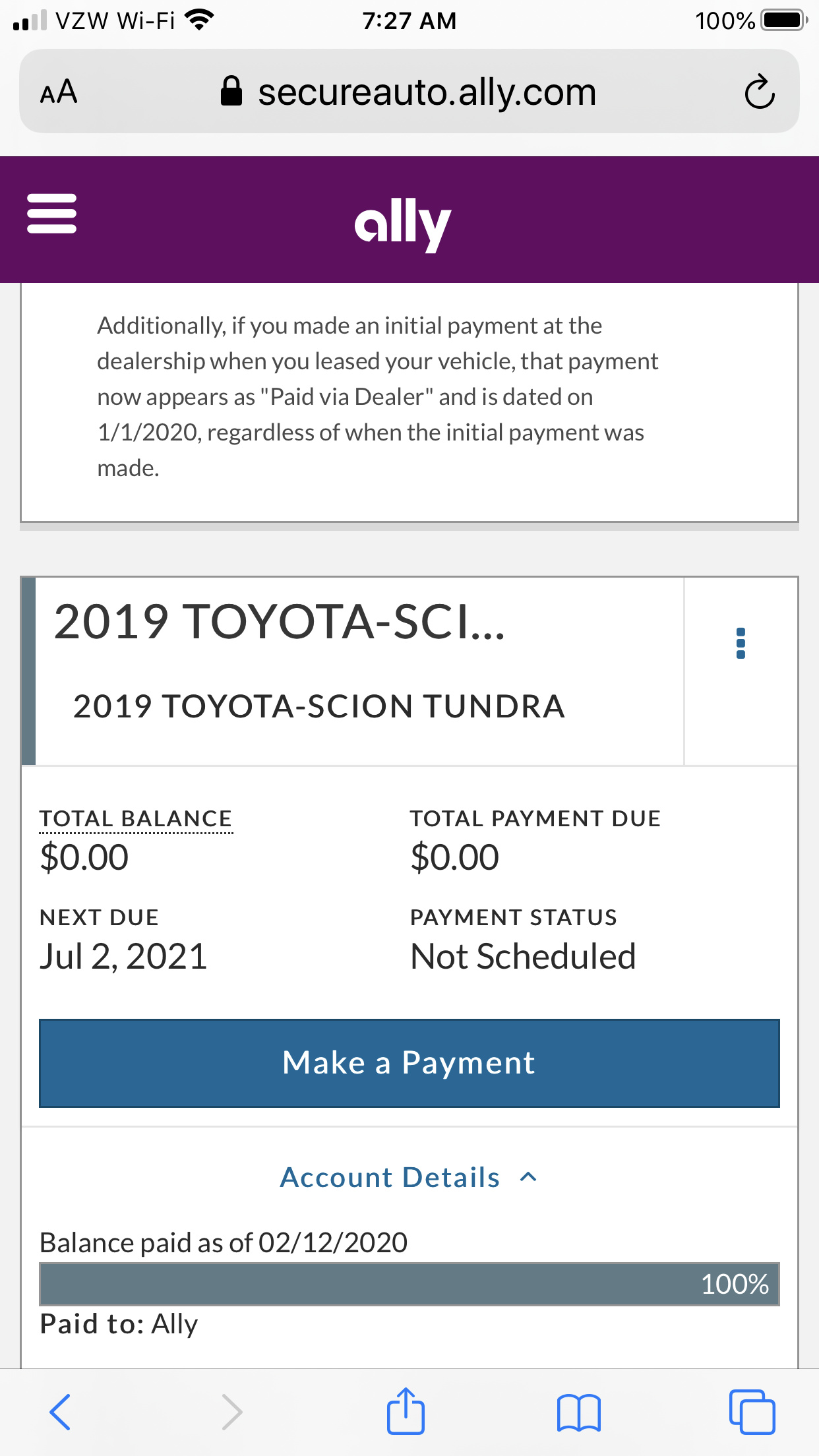

It looks like Ally may atleast on my Tundra.

First time I’ve ever seen it.

May just be based on their horrific website, but I’d be curious what others see.

I made 7 payments of $302 including tax (some look funny because I added a bit more money to account for excise tax) or less at the end of the year because I still haven’t gotten the excise tax bill.

After 7 payments of 302, I made one for 4860 (divided by 17 = $285.xx/month)

I did this to set myself up for a large purchase/DTI ratio. Not something I would ever normally do.

But, it looks like it may save $17-18/month in interest.

1 Like

It’s much different than a typical loan as you are paying interest on the eventual residual as well as the depreciation since you have a $50K asset of theirs for several years. Also compound interest is not being applied since the loan amount is relatively small (vs a mortgage) so they just use the average amount being borrowed.

You multiple the MF by 2400 to get the APR bc it’s 1/2 of the total loan amount (avg amount borrowed) then divided by 1/12 since you are paying per month. 4% = .04 * .5 * .08333

= .001667 MF

You then apply that to the sum of the cap cost and residual to get your monthly rent. You add them together, again, to get the average amount being borrowed, for simplicity sake. Otherwise they would have to compound interest monthly based on amount paid towards the depreciation and current value of the car which is complex.

So you could save some money by paying your payments in advance to cover the interest on the depreciation (if allowed by the captive) but still owe the interest on the car itself until it’s returned. It’s why OnePay saves you money but doesn’t negate interest completely and MSDs are actually a better deal (typically) since you are saving more due to the reduced rate on the car itself which can be the larger amount (especially with BMW).

2 Likes

Isn’t it the same as putting “money down” on the lease?

I’ve never seen any kind of interest credit from making additional payments on a pre-existing lease. I’ve paid off a few early, and it was simply a matter of multiplying the monthly payment times the remaining term. For example, a $400 lease with 6 months left = $2,400.

I never received any kind of credit back for the lease, and I live in NY where the banking laws are among the most consumer friendly. They don’t treat a lease like an installment loan, so the early payoff rules generally don’t apply.

As far as putting money down on a lease, that’s different – because that is done before the monthly payment is determined. In that case, you will save interest (and also have your down payment reduce your monthly “rent” charge). @Britten440 explains it in words a couple of posts above.

I’ve never prepaid a lease but pretty confident that people have posted here about saving interest during an early buy out. It could vary based on state and/or captive. In that scenario, there should be a considerable cost savings since you should get credited back both the interest on the depreciation and car itself. They may take that into account when generating the revised buy out amount.

That’s a different scenario though, as you’re no longer holding the asset after the payoff, so there isn’t an outstanding “loan” to pay interest on.

If you prepay the lease, you’re still holding the asset so there is still an active “loan”. (This is why one-pay leases still have a rent charge)

1 Like

Agreed… I posted about interest applied to the asset earlier… IF a captive credits you for an early prepayment, it likely would be small vs. doing an early buyout since the asset residual value is likely resulting in a significant portion the overall interest.

And most don’t, because the rent is the cost of captial over the term. The MF is discounted on a one-pay upfront, but once you choose payments over the term the rate is the rate, and the lender wants their rent. Whether you make all the payments in month 2 or every month for the term, they fronted you the car and they want all their rent by disposition.

Rent is (cap cost + residual)*MF so paying it off early is similar to paying more for a lower initial cap cost upfront, but obviously more complex because it’s prorated.

Let’s just assume you paid off $10K on the remainder of the lease on a car with a $45K initial cap cost, $30K RV with 24 months (out of 36) to go using BMWs current MF (.00142). The “credit” would be around $340 ($10k*.00142*24), while still paying almost $2K based on the RV and remaining cap cost (which are the same as the RV if you pay off everything). So even if a captive credits you, not much money anyway as it relates to total rent paid and why paying a lease off upfront is not that beneficial.

Take the same numbers and apply BMWF OnePay MF (.00112) vs. paying it off upfront and the rent charge is almost identical, thus how they came up with that specific MF reduction plus the benefits of getting your payments back if the car was totaled since it technically goes into an escrow account.

You could invest the spare cash in Tesla shares and then actually be able to buy a Tesla