Hey guys. I am new here officially, but I have been reading posts on here to gain as much knowledge as I can. I am still trying to get the hang of forums and searching and whatnot. I have a couple questions that I hope you guys don’t mind helping with.

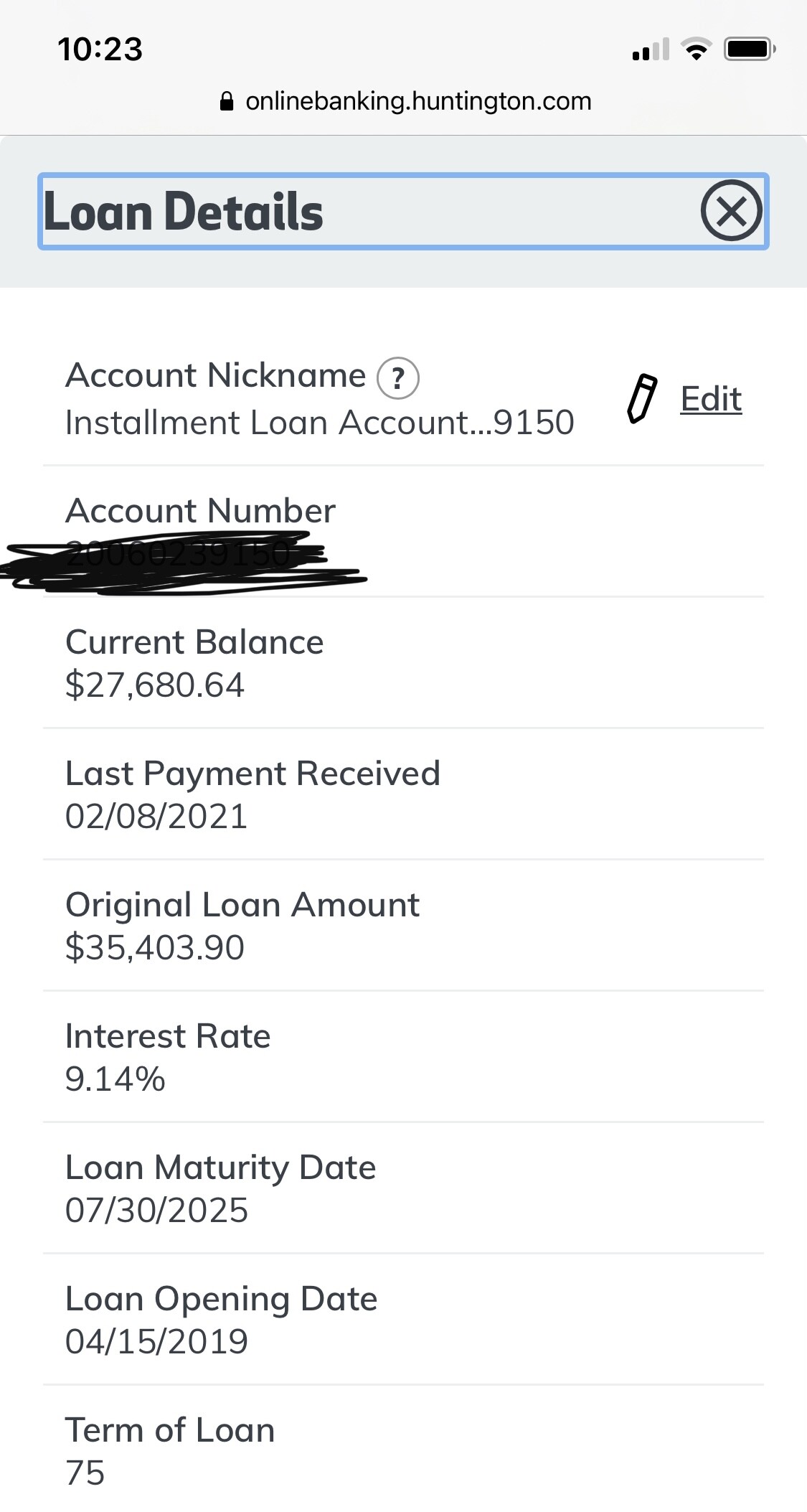

Background info: I currently have a 2018 Mazda 3 Touring with 40,000 miles. I purchased this on a manic episode (before I was diagnosed with bipolar disorder and put on medication) and rolled in a bunch of negative equity from my previous car and all around got a horrible deal. Payments are $623 @ 75 months at 9% with 1k down. Current payoff is $27,680 trade in value hovers between 12,100-13,700.

I am looking at what options I have for getting out of this. I will be closing on a house in a little less than two weeks, so I obviously will be looking to do this after that. My credit was ran for my pre approval from all 3 and they used my middle of 705.

I need assistance on which vehicle would be possible to complete this type of transaction. I can’t seem to find (or maybe understand?) what vehicle has a high residual value, incentives, and low money factor.

I was trying to find something that has MSDS but seems that only luxury brands and Toyota seem to offer that? (From what I could find) I have around 3500-4K to use for MSD or cap cost reduction. I am able to handle my current payment but would not be want it to be any higher if I chose to lease something.

I am also open to refinancing and keeping my current car. I have 52 months remaining. I was going to do this option before house shopping, but was preapproved with no issues with my DTI with my high car payment (which is what I was worried about) but am unsure if it is wise to 1. Sink 3k into a refinance and still be very underwater

2. If they will allow me to refinance due to the amount of neg eq

Would this be something that a broker could help me out with? I am open to that route as well.

Your best bet here is most likely going to be refinancing to get your current rate down and then paying that thing down as fast as possible. Anything you roll it into is going to automatically get hit with taxes again.

Also, rather than look at trade in values, get an actual purchase quote from carvana, shift, vroom, etc so you have an actual actionable number to base your evaluations off of

Will your broker let you roll the car loan into your mortgage? That will be the easiest and fastest way to refinance the car to a good APR (and improve your DTI ratio at the same time).

As bad as that payment is, you will own that car in 4.5 years and late-model Mazdas are solid cars to own long-term. The damage from the old negative equity and high APR is already done, so don’t dwell on it. Rolling this negative equity into ANOTHER new car will put you deeper in the hole. Focus on lowering the APR, get gap insurance, pay the car off (or at least pay it down to zero equity), and then decide what you want to do.

My advice would be to keep the car, refinance to a lower interest rate loan (maybe 3 or 4 year loan?).

Since you are so underwater on your car – Make sure you get GAP insurance through your insurance company. If your car got totaled in an accident, you’d only get market value for your car (not the pay off) unless you have GAP. Personally, I’d probably make sure that the new bank holds the title for the car to ensure that GAP insurance would kick in the worst case scenario (e.g., I know some Light Stream auto loans will just give you cash instead of putting a lien on the car)

I wouldn’t be looking to sign a new lease right now, especially without Tier 1 credit for most banks/captives. Try to refinance your loan and pay it off as quickly as you can. Even with cars that have a ton of manufacturer incentives, you are just going to find yourself in the same place you are now.

Here is a glass half-full side of things: it is a newer Mazda with lower mileage. This car sounds like it has a lot of life left in it. I am not a mechanic by any means, but keep up with routine maintenance (oil changes, transmission fluid changes, etc.) can have a great effect on extending the life of the car. Less money spent on big repair means more money that can be spent paying off the loan.

There is nothing on the market with enough lease incentives to unbury that much negative equity. You will end up rolling the majority of it into the new lease.

Do like @mllcb42 indicated, and refi, and apply extra money every month to principal to pay it down quicker. I would not recommend rolling into the new house as someone else suggested, as you will likely skew your ratios and might end up having to pay PMI as well. Further, you’re now burying your new home in debt, and should you need to get a HELOC for repairs, you won’t have much, if any, equity for a good while.

Take as much money as you possibly can and refinance this beast. You are so heavily underwater you’d have to get into a high MSRP vehicle with a TON of incentives just to undo the negative equity, then there’s no chance for a good deal, anyways.

Just refinance and aggressively pay off the car as fast as you can.

I never thought about asking to roll it into my mortgage…is that possible? I asked to finance a fence into it and it was a no go, so I highly doubt they will allow me to do my car.

You’d need a home equity line to do this in addition to your mortgage.

Don’t do it, even if it were possible, and without knowing the specifics of what you’re buying vs what the current value of the home is, nobody can tell you outside of your mortgage agent. You’re going to set yourself up for disaster in the short-term.

It sounds like there was some sizeable amount of negative equity rolled into the 3.

@dervin, every time you roll negative equity forward, you get slapped again with tax on it, so it just compounds over and over and over. This is a really easy way to snowball out of control. I would do everything you can to focus on getting rid of the negative equity rather than just compound it in a new lease.