MSRP: $65,635

Sale Price: $65,635

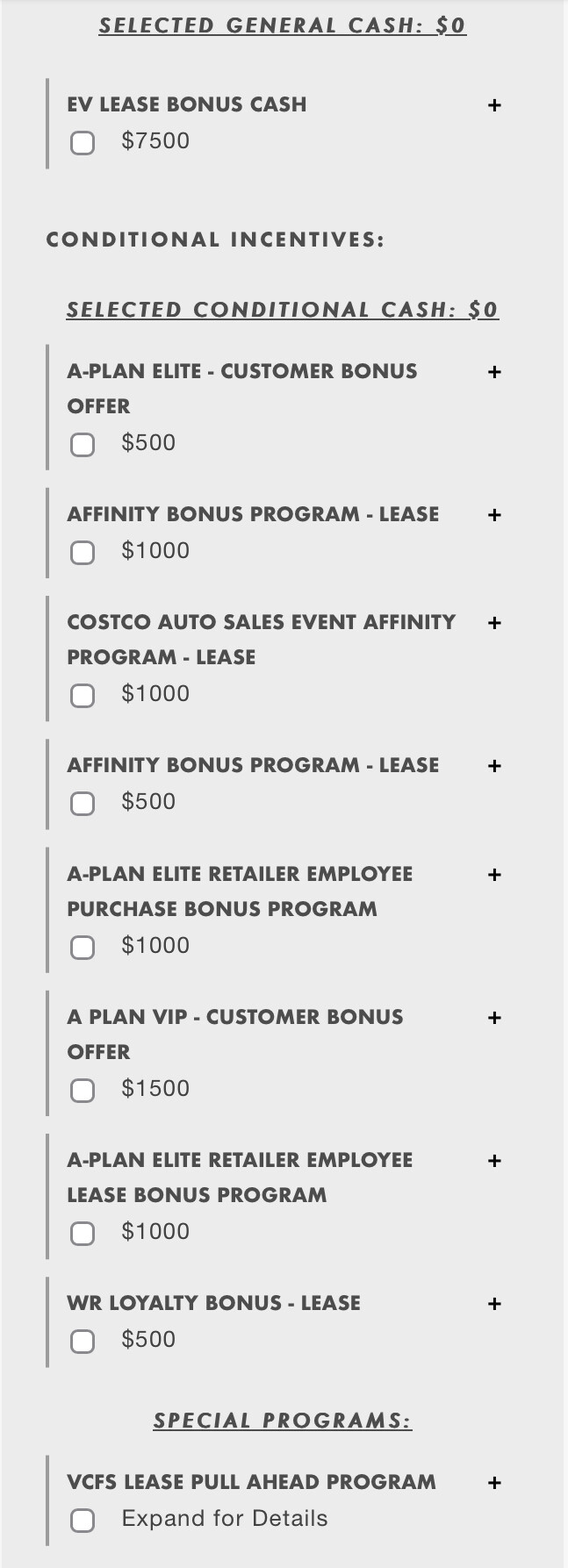

Incentives: $10,000 ($7500 EV lease credit, $500 A-Plan, $1000 CostCo, $1000 Memorial day)

Net Trade-in: $26,000

Residual: $32,817.50

Fees: $455.25 Taxes, $924.25 Gov’t Fee, $125 Doc Fee

Terms: 36/10,000

Money Factor: 0.00353

Payment: $249/mo

Our plan is/was to lease to get the EV Credit and then buyout immediately at ~4.99% APR from a local credit union.

My questions are:

How are they getting the $249/mo lease payment? I am assuming since the depreciation is negative, this is just the finance fee? In this scenario, are we better off then just applying as much of the trade-in value to get to $0 depreciation, then apply the pocketed amount to the lease buy-out financing?

I am also guessing that the quoted MF of 0.00353 is not what they are applying then since this appears to be closer to 0.00384 to get $249/mo. The sales rep said the MF is set by the bank and they cannot mark it up so I think I need to escalate this to the business office to get some better terms since RateHackr has 0.00293 for this make/model. Inventory is scarce in our area so I’m not too hopeful on getting a better deal. There are no XC60s on the lots here and everything coming in is taken.

When I put in the numbers on the calculator using the trade-in, the payment is $163. Without the trade-in it is $977. So even comparing the $163 to their quote of $249, I think the negative depreciation is what is leading to $163 on the calculator.

Any thoughts on if this is a natural next step to escalate the MF discussion to the business office or financing to come back with a better figure? Our credit score is 780+ so I could ask them to run our credit and come with a counter offer?

The MF markup doesn’t matter if you are doing an immediate buyout, but an MSRP + bumped MF is a terrible deal, unless they are over-allowing for your trade by a ton. Which is why you need to separate the trade from this deal to assess it.

Thanks, that makes sense. One reason why we are opting for the Volvo is that we were getting trade-in values closer to $23,000 from other dealerships. Taking out the trade-in and the MF mark-up, it’s a difference of $1100 in our “favor” I guess? We’re getting $3000 more on the trade-in vs. others but the MSRP + bumped MF is $1908 for the dealership.

Thanks for confirming! I checked my regional forum (midwest) but didn’t see any recharges available unless I completely missed it. Definitely would have preferred that option as peace of mind of a good deal.

We’re getting the car we (my wife) wants and out of a car that has been springing issues lately (new tires, electrical, etc). For those reasons and potential gas savings (majority of our commutes are < 15 miles each way), I think we’ll go with this deal unless I can find a broker option!

I know regions can differ, but the XC60 is an aging design. Out here (SoCal), they are knocking 10% of MSRP, and then giving the credits on top of that. Check with Edmunds or True Car as to the selling prices in your area, but sticker for the XC60 is crap.

That was my question for the sales rep and he said I would need to meet with the business office. I couldn’t get to $249/mo payment with the negative depreciation. Assuming they may as we save part of the trade-in equity that I’ll just apply as a down payment? Since we are buying out it’s this or apply it as a down payment on the auto loan when we buy out.

Do dealers usually handle negative depreciation a certain way?

I checked both Edmunds and TrueCar early in our search and with our zip code I was coming up with 1-1.5% off MSRP. I am feeling that the lack of inventory is handcuffing our options to negotiate on price, which sucks. The other dealership in our state hasn’t had a Recharge in stock for a few months now……

We qualified for the EV Credit, A-Plan Elite (Healthcare), CostCo ($1000), and the dealership had a Memorial Day $1000 off MSRP. So we had a total of $10,000 in incentives.

Haha, no worries. I appreciate everyone’s input! It’s nice to have folks look at the numbers and deal with me since it can be daunting. I know I didn’t get the best deal out there and we’re in a market where the consumer has less leverage. We’re happy with the car and are going in with full understanding of what our payments will be after the buyout.

I am interested if anyone has insight though, the business manager mentioned that we should wait 3 months into the lease before buying out. He indicated there may be some incentives for early buyout that kick in then? We have never leased before, but is/could that be true?