If you have self control to own this for 5 or 6 years, finance with a credit union.

If you’re going to be bored of this in 24-36 months and want a new ride, then lease.

If you have self control to own this for 5 or 6 years, finance with a credit union.

If you’re going to be bored of this in 24-36 months and want a new ride, then lease.

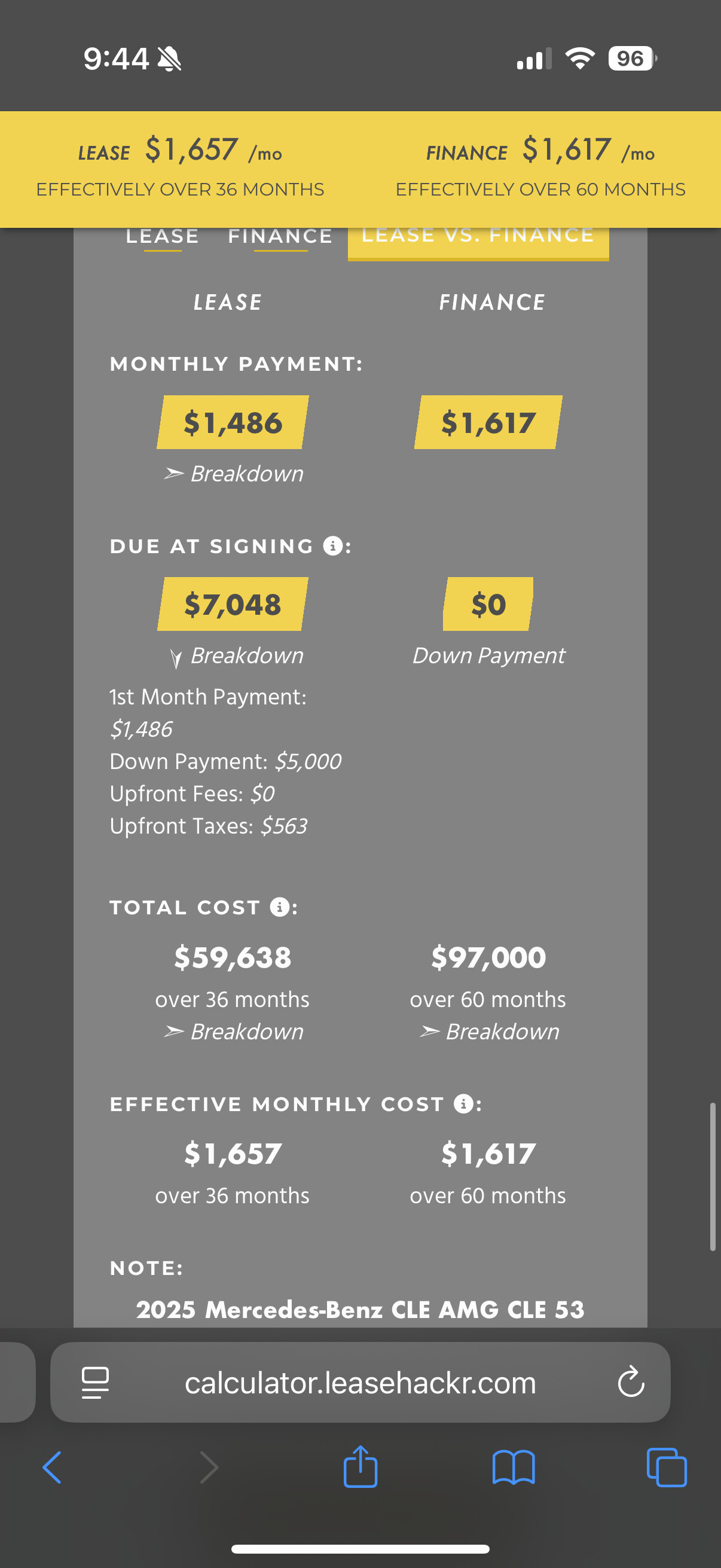

I expect to only drive for 3 years max and move on to something else. I used the leasehacker calculator tool and this is the output with $5k down

36 months of use before your next new Benz makes you an ideal customer for Mercedes. It’ll be expensive, but for you… rolling leases and clipping lease loyalty incentives is better than the credit union option.

Make sure to use the tips you learn from LH to negotiate the lease economics and get the buy rate money factor.

Check out this thread for credit unions with the best finance rates.

@Yfc596 get psyched about your CLE53…

what i meant was, what is better financially? will my monthly payment be less if i finance it or lease it? say i want to lease it for 3-4 years, 0 money down except taxes/required, 10k miles/year. what would give me the better monthly payment? if i finance it i’ll probably end up paying it off in a few months

why put 5k down on a car you’re renting? i was always taught not to put any down on a lease unless you are 100 percent sure you are keeping it

Don’t use the monthly payment to determine “better”.

Rather, you should consider what your expected duration is to be in the vehicle, how many miles you need, and the cost of funds to access that vehicle for the period.

If your plan is to roll into a new vehicle by month 36 like @Yfc596 … then leasing makes sense. The buy rate on the coupe is 0.00137 (3.3% apr). If there is positive equity at the end of the lease, then you can pocket the upside. The lease limits downside… this optionally is one of the reasons leases have an origination fee while a simple loan does not. Leasing ICE (no government subsidies) over and over is expensive since it means paying to drive an expensive Benz during the worst part of the depreciation curve.

Consider a hypothetical @KFC123 who wants to keep rolling fresh Benz every 3 years and finances instead of leasing. His monthly payments go up, but there’s a much better chance he has positive equity at the end of the 36 months. But, KFC is 100% exposed to the residual since he bought instead of lease… even if KFC drives the same miles as Yfc.

This is still expensive since KFC is driving an expensive Benz during the worst part of the depreciation curve and disposes the vehicle before the depreciation gets cheaper.

The “better” for a vehicle comes from someone willing to experience the deprecation curve on a car after that initial 36 month period. The fore-mentioned Yfc or KFC both have the option to stick with their rides longer after month 36. If they kept the car longer, the financial picture starts to look better. But that that point it isn’t a case of leasing being better/worse than buying. It’s just a case of tolerance for a used car is cheaper than rolling into a new ride.

@holeydonut Thank you for the thoughtful and well-articulated response—this is incredibly helpful and cuts right to the heart of the buy vs lease decision.

You’re absolutely right: evaluating based purely on monthly payment misses the bigger picture. I haven’t held onto a car for more than 3 years over the past decade, so the lease route aligns best with my behavior and preferences, especially considering the downside protection and flexibility it provides.

I really appreciate you pointing out the buy rate of 0.00137. That’s a key input I was missing and can now bake into my payment calculations. Assuming I can negotiate around 5% off MSRP, I think the numbers could work well and make the lease a clean fit for how I approach car ownership

I don’t know if I would say leasing providing flexibility, esp since MB charges a 4% early termination fee.

Not saying you shouldn’t lease it, but I would caution against thinking that a lease is “flexible.”

this is a great reply to my question, thank you. I might have to pm you in the future lol

so now i understand lease and financing a little better. what about when it comes to leasing vs financing say a 1-2 year old CLE 53 vs a brand new one?

For cars like this… if you’re down to try and own one for a long time and you want a banging deal…

either wait to land a model year end close out 2025 in 8 months…

or hunt used cars that have ultra low miles as CPO since the original financing fell through. That convertible CLE I linked above is a prime example. As is this Graphite Grey Magno Coupe that @theduke knows well.

They bought at auction and needed 4 months to get the title cleared up! That’s 4 free (free to you) months of languish that further depreciates … and now they need to blow it out. They can knock down a few more and you’re almost 20% off MSRP. Check out all those AMG addons. CPO! No night package though.

![]()

Leases used to be flexible in the past. Could transfer out of them or sell/trade without penalty. No longer for MBFS.

Flexibility means picking and choosing the timing of your next deal and MBFS leases don’t offer that.

No way to answer this in the abstract. Depends on the cost of each strategy.

Someone who leases a new Benz then wants to sell it in 3 months is in the same boat as someone who buys a Benz then tries to sell it in 3 months. Assuming the sales price net of rebates is the same.

The Benz lease is more flexible at maturity in that the lessee is not forced to accept downside risk of the vehicle value at that time.

Yes some BMW leases are transferable, and more “flexible” than a Benz lease. But as we’ve seen on this forum, a SAL or private transfer usually takes advantage of a prospect lessee not understanding that they’re overpaying when they take over a second hand lease instead of leasing new themselves.

Let’s pretend BMW offers 12 month leases and also offers CPO leases.

Imagine a $100k BMW with a 12 month resid of 75%. And a 36 month resid of 50%.

If someone takes the first year on a 12 month term, they’re doing 25% depreciation inclusive of rebates. The person who hypothetically re-leases the CPO vehicle for 2 additional years should only have 12.5% of depreciation per annum.

A CPO originated lease on a 1 year old car with 25% depreciation over two more years should cost less. But SAL folks take advantage of people fixated on payments (sound familiar?). They point to the LH marketplace and talk about how their used lease is a bit cheaper than new.

The people who SAL a 1 year old lease (2 years left on the lease) want to trick people into comparing the SAL lease with what a new car would lease for in the market now. That’s a fallacy. Used cars should be way cheaper, not simply compare to a new car payment.

MB Financial probably never offers tax credits on a vehicle like this.

At this time, they seem to be pushing the tax credits on the EVs (to entice some sales)

How do you negotiate a rebate? Either you qualify or you don’t.

You do understand that your “$5k down” correlates to you writing a check for $7048 at signing (based on your caclulator)

Then pick a hackable car. People are paying less for M4s and M8s on here.

The idea of paying $20k per year to drive a 440i competitor is cray cray

This belongs in the Worst Leases thread if signed.

@Yfc596 : don’t let the forum trolls bully you out of enjoying a car that you custom ordered for yourself.

This forum has a few people who only like a car due to its payment. They cannot fathom someone enjoying a car because it’s the exact build someone wants to drive (and thus paying a premium for that experience)

Since you actually derive joy from your vehicle and not your payment, these users aim to elevate their ego by trying to put you down. @DailyDriven can explain more as well.

If you can get the 5-8% off MSRP and buy rate, the lease will be pretty good on a CLE53. Don’t let the haters diminish your experience.