Working with several dealers I understand they are allowed to mark up MF and Residual to a certain extent. I have found a few who will not mark up at all and then many who will, often to an obscene degree, and act as if they have no control over the corporate finance rate. Ihave have not found a negotiating tactic that works on this.

At the end of the day do you just send them a monthly payment number and if they agree to it, who cares what the mf is? I feel like this is the right answer but if the mf is high and I want wear/tear coverage on top, it’s going to be hit with some pretty high interest.

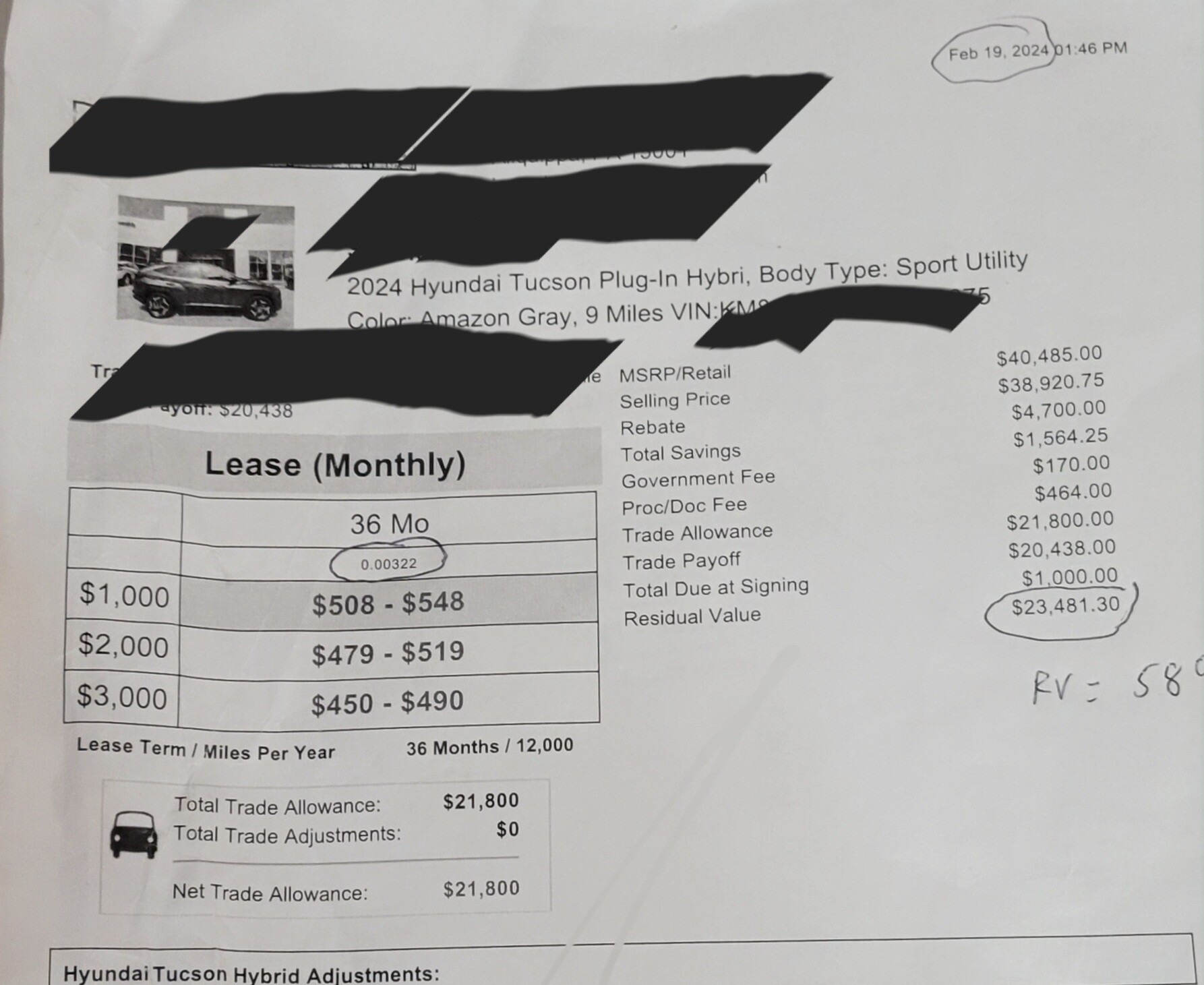

No dealer can change the residual value. That is set by the finance company / leasing bank.

Pick a stock # for the vehicle you are interested in and make them an offer. Who cares if the MF is marked up , as long as they agree to your target monthly.

And they are definitely marking up RV as well. At least in PA they are. At least on their offer sheets.

See, I was always told not to focus on monthly payment but on price. So this is new to me.

So I research a car and see okay my payment should be $400 a month based on the going markup and rv, and if I can get $1000 off MSRP ($40k car, I’m not looking for an amazing deal). And they go ok $600 off MSRP and Jack up the MF/RV and suddenly I’m looking at a $600 lease payment!

Share a deal sheet here, since as we’ve stated that is impossible.

Here is my approach. Get the RV and MF numbers from either Edmunds, or if you become a super supporter of LH, you will have access to these numbers. Then, plug all this info into the LH calculator assuming base MF. Your pre-incentive discount will determine your monthly payment.

Have you look at broker deals in the Marketplace for research purposes? It will help you determine a target deal.

Theres a big difference between focusing on an arbitrary monthly payment amount and establishing what the monthly should be for a specific due at signing amount and offering that.

Starting with a monthly payment blindly and creating a target deal, establishing what the monthly AND das should be, then using that to communicate your deal are two VERY different things.

That much discrepancy sounds like you had the rv/mf of the gas version vs the hybrid, but it may have been a different bank. If youre seeing that kind of difference, that may be why. Sometimes its a case of them using a different program with a larger rebate, etc.

The dealer cant mark up the rv either way. It is set by the bank.

Having a current example where one could actually compare against the current programs to see what they should be would be helpful. Theres teally no easy way for us to do a post-mortem on last month’s programs.

Neither of those are current, so we cant verify what they should be, but notice the significant increase in incentives that accompanied the change in rv and mf? Thats either a mid month program change, in which case you need to look at the whole thing or a different bank.

How is your credit? It appears some dealers using banks outside of Hyundai to source the lease…regardless, you should put together your own deal using Hyundai numbers to come up with your target payment in the LH calc…or find a broker in your area via Marketplace to take care of deal for you.

Also, go online to Carmax, Carvana, etc to value your trade.

I don’t have a current one because the programs have just changed. Although I did try to get a deal today at Kia where they offered me 61% RV on a car and then offered me 62% to lower the payment. But they took the sheets.

But why do you need to verify it to believe me? I’m showing you the proof and asking for advice but you’re just stuck on the one part about RV changing. It doesn’t matter if they can adjust RV or if they can choose different banks/programs. How do I get them to agree to what I’m expecting based on the research I’ve done when we are $100-$200/mth apart?

My credit is 800+

I know the amount I want but (most of) the dealers are so far off and it’s usually because of the inflated terms rather than the % off msrp