I’m a serious newbie to this so please be kind.

I can sell my 2019 Hyundai Kona Limited to CarMax for $6,050 over lease payoff. Please explain why it’s a bad idea to take the $6K and use as a down payment on a new 2022 Kona lease? TIA.

I’m a serious newbie to this so please be kind.

I can sell my 2019 Hyundai Kona Limited to CarMax for $6,050 over lease payoff. Please explain why it’s a bad idea to take the $6K and use as a down payment on a new 2022 Kona lease? TIA.

If you wreck the car as you drive off the lot you loose that 6K

What is the MF, and how much will you save in rent charges vs. not putting the money down?

That’s how much you’ll pay to insure against an extremely remote risk of a catastrophic loss.

I’m not saying put the money down or don’t put the money down. Just evaluate the cost vs. risk.

Also, consider the implications if you decide to transfer the lease to someone else before the end of the term. Very few people do this, but it can matter to those who do.

With that equity out into the new lease what numbers are you looking at? Is it the same exact trim as the 2019? More options? How much of a difference in payment are you looking at?

There’s no transfers with Hyundai leases.

Generally when it comes to more inexperienced people, I think the bigger risk with putting a lot of money down is convincing oneself that the lease is a good deal because of the artificially low monthly payment due to the large down payment.

So no transfer issues.

That leaves the risk of the car being completely incinerated by a troupe of nuns on a meth-fueled rampage.

I wish there was a solution to people who lie to themselves.

Look at it this way: someone who has not reached disposition is asking, “should I peanutbutter $168/mo in equity across this 36 month lease?”

![]()

Unlikely, no. Now:

That’s the important question …

The 2022 Limited has 25 more HP, a better DCT, digital instrument cluster and 10.25 touchscreen infotainment screen.

I’m afraid the average customer will also be led into a bad (or horrible) deal because of the $6k of “free” money. You can’t justify a new bad deal by coming out of a good one. I would use no more than half of the money and pocket the remaining. When shopping for your deal, leave the money down out of the equation for simplicity. Its basic math to factor in the money down by dividing by the term of the lease, and subtract from your monthly.

Bergstrom, ehh, must be near my neck of the woods. Immediately, two seconds of looking at the offer, I would say pass. No way in hell am I paying ~$458/mo to drive a $30k Hyundai.

But then again, the 1% rule is irrelevant so what do I know.

Have you compared this to other recent Kona deals and broker listings?

For the 2022 model I have not found deals to compare with nor any brokers.

Have you looked to see which incentives are available for you and which ones are already put into the offered discount? Has the dealer provided you with the MF and RV to compare with Edmunds values?

In a previous proposal he sent the MF was listed as 0.00227. Edmunds responded that the MF is .00187 with 56% RV.

Also, if you’re looking for anything of next years model year… it generally makes a deal more difficult. I also did a bit more digging. The residual isn’t horrible, but the money factor is (you would be paying a high rent charge for this vehicle). That in combination with minimal discount (not even 2%) and no incentives, yield a not so great lease…

Do as you may, but this is a very poor deal IMO.

Correct, that is what I had come up. I wouldn’t want to pay the .00187 in this case, let alone the marked up MF. That is nearly 5.5%!!

You need to stop asking the dealer for information and work out your target pricing independently. Talking to the dealer is for finding someone to do your deal, not for figuring out what that is.

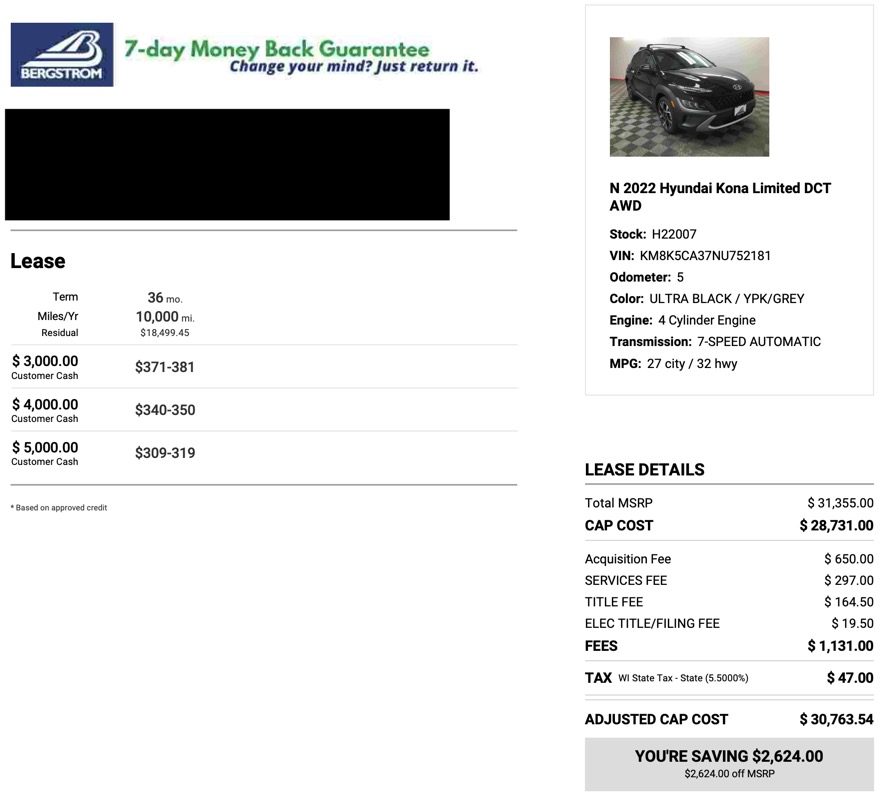

I used the lease calculator and feel like this is a good target deal (I could be wrong). Feedback?

And with all those subtle changes what would be the difference in the lease payments you pay on your 2019 vs the new 2022 lease?