I’ve been able to negotiate close to 8000 off MSRP (11.82%) . Essentially covering all of the added trim packages and some.

The issue i’m currently running into is that even with my excellent credit score, they won’t give me the tier 1 rates or the current buy rate of (0.0007-0.0008). The manager basically told me he can’t go below 0.00110 because they need to make a cut somehow too. I was also told the residual value for the vehicle is 51%.

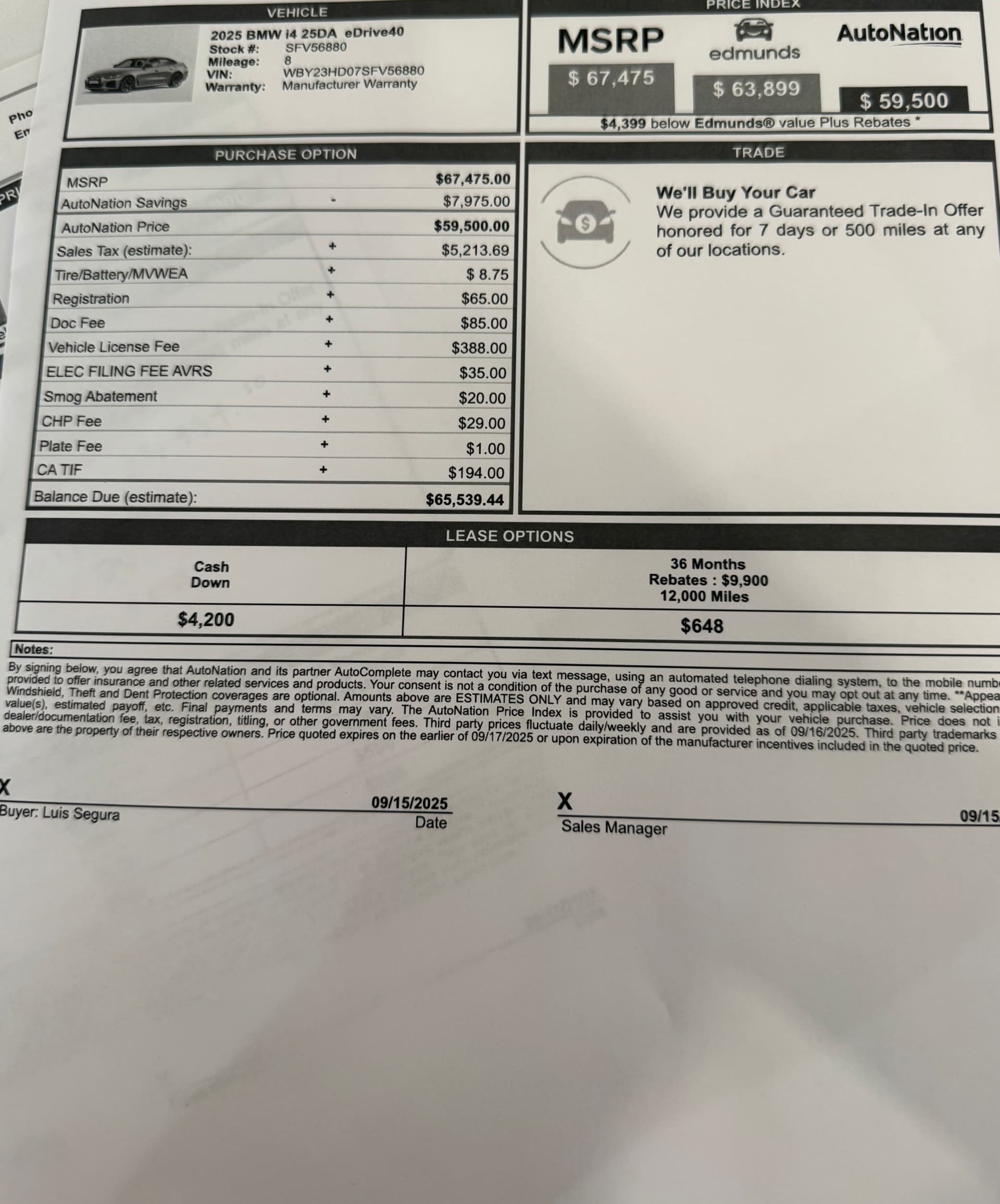

That being said, i posted three pictures with 3 different scenarios

• 1st photo: $0 down ($683/mo)

• 2nd: 6 MSD’s ($4200) applied ($648/mo)

• 3rd: $3000 downpayment ($588/mo)

When i plug these numbers in the lease hackr calculater (which i did with them personally and had them verify) we come to similar numbers without any downpayment or MSD’s and they can’t figure or explain why. Are they telling me one MF and residual value % and inputing another?

Here is the correct calc. At 36/12K the residual is 50% - not 51%. They made have made an error telling you the residual, but the calc matches the dealer worksheet.

Your effective monthly in this deal is (with $3,500 driveoffs) is $668. My effective deal in SoCal with broker fee accounted for on the exact same MSRP is $610 with the exact same structure. $668-$610 =$58.00 * 36 =$2,088.00 in savings. Even with transport that’s $1,600+ in savings.

I would suggest this: if this spec is good and you actually like it —> you can push for 12% & buy rate.

If they don’t give you that, I would not take this deal. If you’re open to transport or even picking up in SoCal, text me at 949-775-1714. Can save you money + no back & forth

As always having great credit makes you eligible for the base MF but not entitled to it.

In any event getting into the weeds with the dealer about the MF is a complete waste of time. As long as the overall deal is good and meets your target (payment & DAS) then who cares if the dealer marks up the MF.

If 12% pre-incentive and base MF is your target (based on the good advice above), then figure your target payment and DAS based on that, and tell the dealer you can sign today if they can get to X payment with Y DAS. Let the dealer decide how they make their money.

Thank you for correcting that. 51% is what they told me at the dealership so thats what we carried on with. I am new to leasing so a lot of this in new territory for me so forgive me if some questions seem rather clueless. The dealer’s worksheet (the one with $0 payment). Is the effective monthly payment $683 then? And if so, what accounts for the extra payment vs the one you calculated using their numbers? I assume the DAS is being rolled into the monthly payment? Or am i expected to pay $683/mo + $3500 due at signing? I just want to be clarify this.

And i appreciate the offer. I will definitely consider if we can’t find common ground. I do like specs. Its ideal color combination (CYG/Cognac with M sport package) so i am leaning towards getting something done. But if i can’t in next 2 days. You’ll be hearing from me

No effective monthly is the sum of all the payments + any driveoffs ($0 in that particular deal) + disposition fee divided by the term (36). My deal’s effective was even cheaper than theirs with broker fee & transport considered & I can also give you a structure that makes the most financial sense and gets you the lowest effective cost.