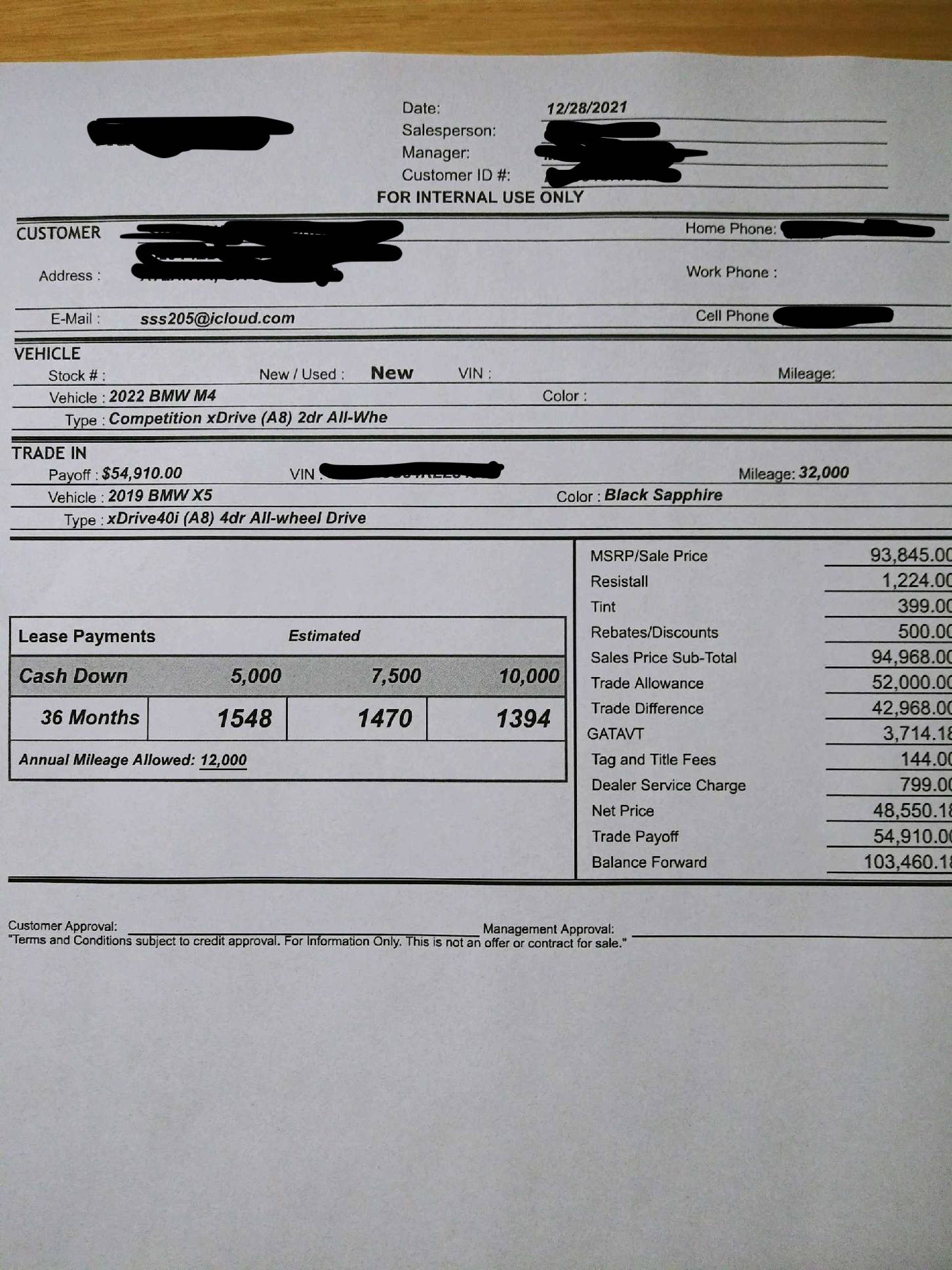

Wanted to get input on the below lease offer I’ve received via emailing with the dealer for an M4 Comp Coupe XDrive. I got my X5 from them in 2019. This is the first offer. Looks like max marked up .00151 MF, whereas the car is supposed to be .00111 MF with the 56% residual.

I’ve countered with asking for what’s in the below calculator, basically removing the dealer adds and base MF, along with a net zero out of my trade with the payoff (Carvana and Vroom both quoted 56k so about even but would like to avoid the tax hit of buying out the lease and then selling).

Located in Georgia.

Totally understand that this is overpriced for an M4, but this market is absolute garbage and we’re planning to get a house in early summer so would like to clear up any large credit-based purchases a couple months before that (lease technically ends in May).

I think sticker and buy rate with no dealer adds is more than fair of an offer.

Lemme know if you don’t get anywhere with your counter offer. Don’t know enough about your trade to say if they’re jamming you up on that end but that worksheet seems high. Resistall dealer add tells me it’s a GROUP1 shop…

Unless you buy it out cash, how are you clearing it off of your credit? Nice choice, I am actually thinking about an M3 Comp X-Drive this spring, but I will be ordering a much lower MSRP build and purchasing it if I go that route.

Haha sorry I think my phrasing was poor. I mean I’d like to get any credit based purchases wrapped up at least a few months before that so they don’t interfere with the underwriting process.

I think max more than understood your point. Leasing a 100k dollar car the same year you buy a house will definitely look weird during underwriting regardless of how many months of buffer you have.

You could be two years into the lease and they’ll still consider the lease.

That’s a large payment that will definitely impact how much they’re willing to loan. I’m guessing you make more than enough money so it shouldn’t be a problem.

Sooner the better. The BMW FS account took a couple months to show up on my report. If you’re set on a house, I’d consider waiting on this until after closing…big lease accounts are still a PITA. I had to pay for some points because my lease messed with my DTI a bit. From my understanding, they look at the total lease cost, so this would look like a $51k loan, even with base MF.

I think my DTI should still be fine, but you guys got me thinking it might still make most sense to wait until after Closing just to make sure there’s no issues whatsoever.

The silver lining might be a better overall market as well.

If you are well qualified for a mortgage, it won’t matter when you lease (or buy) the next car.

Don’t overthink this.

(Regardless of what you do with the car decision, get your mortgage FICO scores now to see where you stand. Get your co-applicant’s also, if applicable).