So I am currently on the hunt for a deal on the 2020 Range Rover Evoque SE and the issue I am running into right now is that dealers seem to be offering low residual values for their demos because they are claiming it is not a “new” 2020. I have the MF and residuals from Edmunds.

Does anyone have tips on how to get dealers to work with you on this?

Mf/rv info- program are national. Captive chase numbers.

Mf: whatever the hell the dealer decides and you negotiate. Base mf is 36 month 0.00001 / 39 month 0.00008. Getting base is often pulling teeth.

RV: 36/10 month 57% 39/10 56%

Loaner adjustment .2/mile for Msrp under 50k, .3/mile over. That’s what I used and it was accurate afaik and I haven’t had an update yet but if someone else has take their word.

Can you explain how the residual is adjusted based on loaner miles?

If it causes the residual to become that much lower based on the numbers I was given by that dealer, then it seems better to work down and get a low selling price with new 2020s with no mileage…?

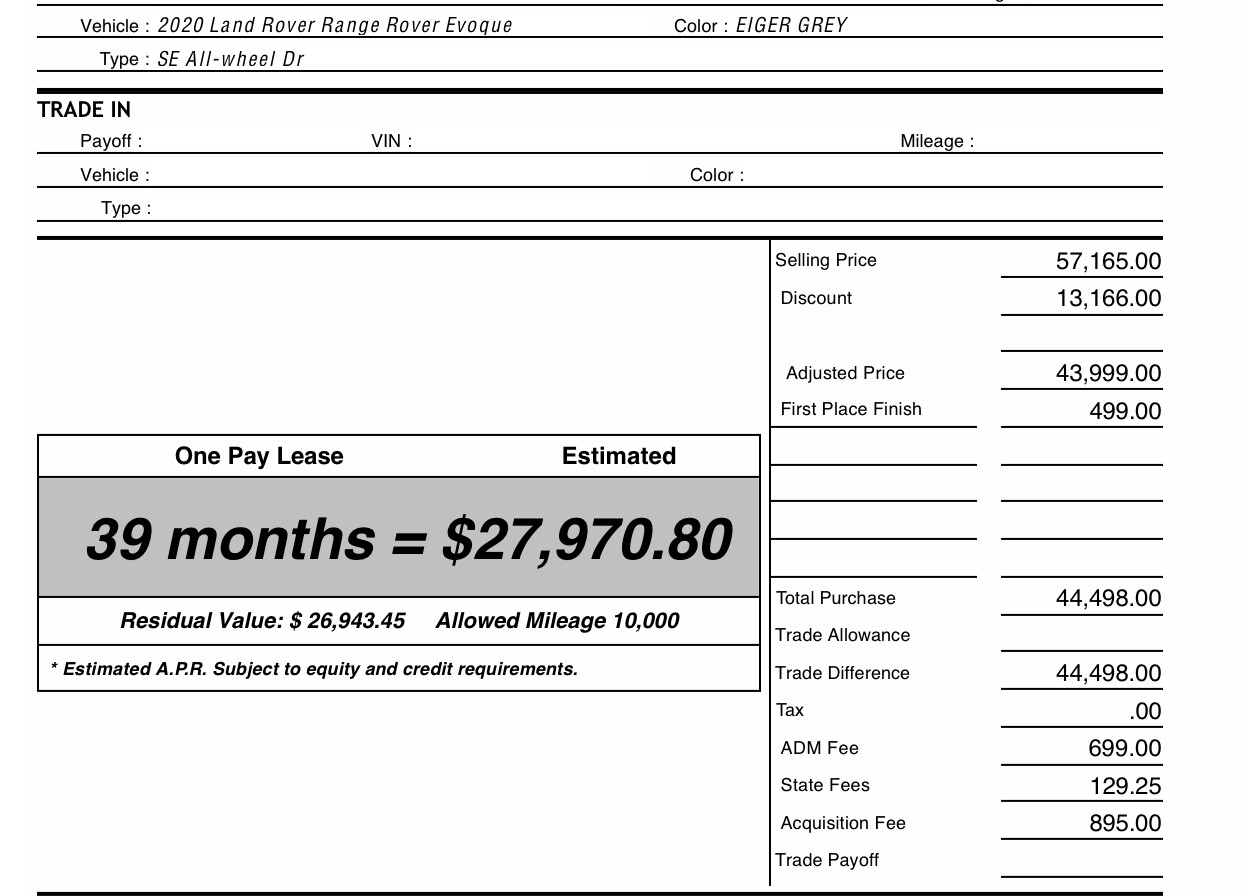

Here’s a quote from another dealer, I’m failing to see where they’re getting their numbers from. The residual on this one also seems high, even if you adjust $0.30/mile considering it’s a loaner. This one had 5,527 miles.

Is $57165 the actual msrp? I have seen dealer sheets like this where they list a selling price that’s over MSRP and then a large “discount”, when it reality the discount is just off their ridiculous marked up price.

Also possible they’re not using captive financing here.

Ha I think you’re right, I can’t see where it has the options to merit that kind of price. Their site doesn’t list as MSRP, it listed as “Was” vs “Our Price.”

Probably more likely than them not using captive financing.

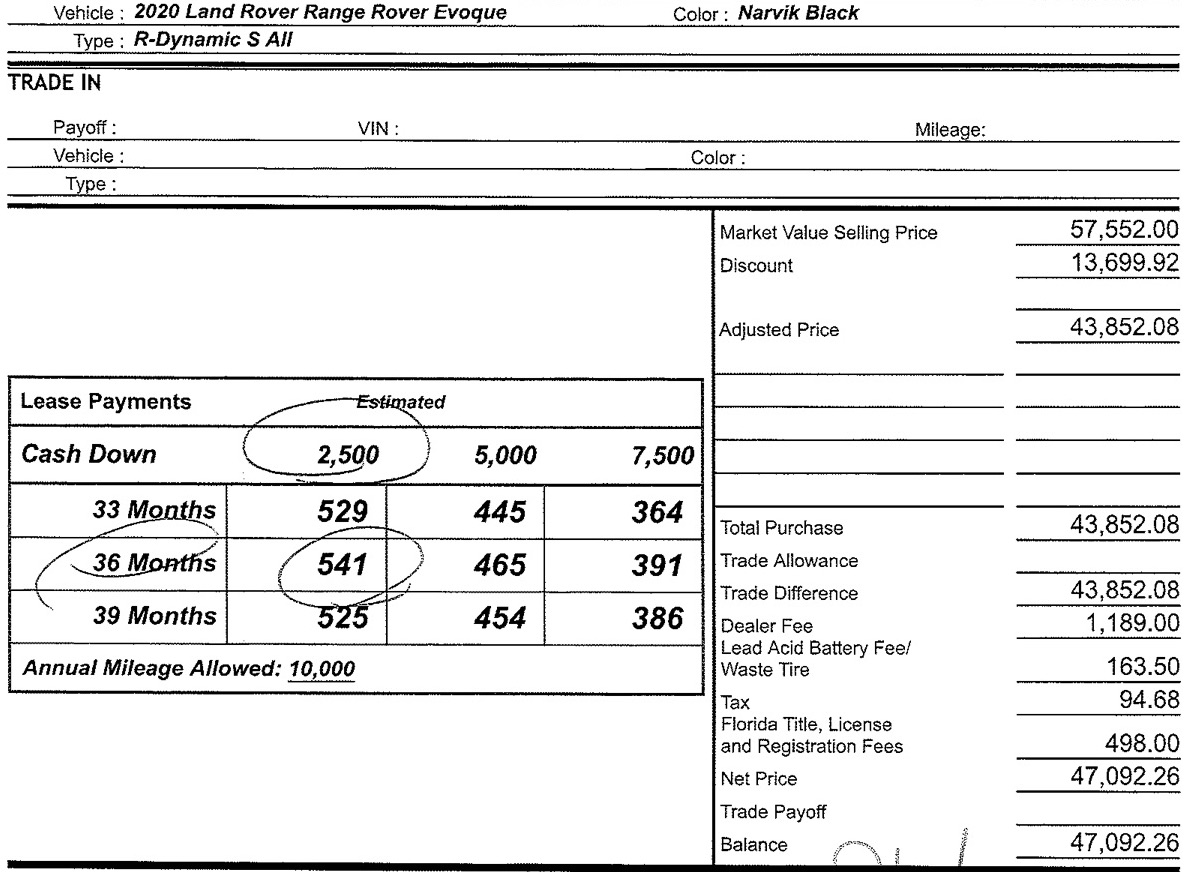

Hey guys, I’m in Louisiana and trying to work on a deal with a dealership in Florida. We’re negotiating right now and here’s what they’re offering. It’s on a loaner with about 5,800 miles. The only thing not included in the images below is the money factor, .00101. Residual value is 51.97% (based on the $29,912.40).

Looks like they’ve marked down the selling price as far as they can go. I’m going to work down the money factor some as well.

Also, does it look advantageous to try and look at either 33 or 39 month terms instead?

Can y’all give me your opinion on where I can trim this down down some more and let me know your thoughts on this deal in general? Thanks!

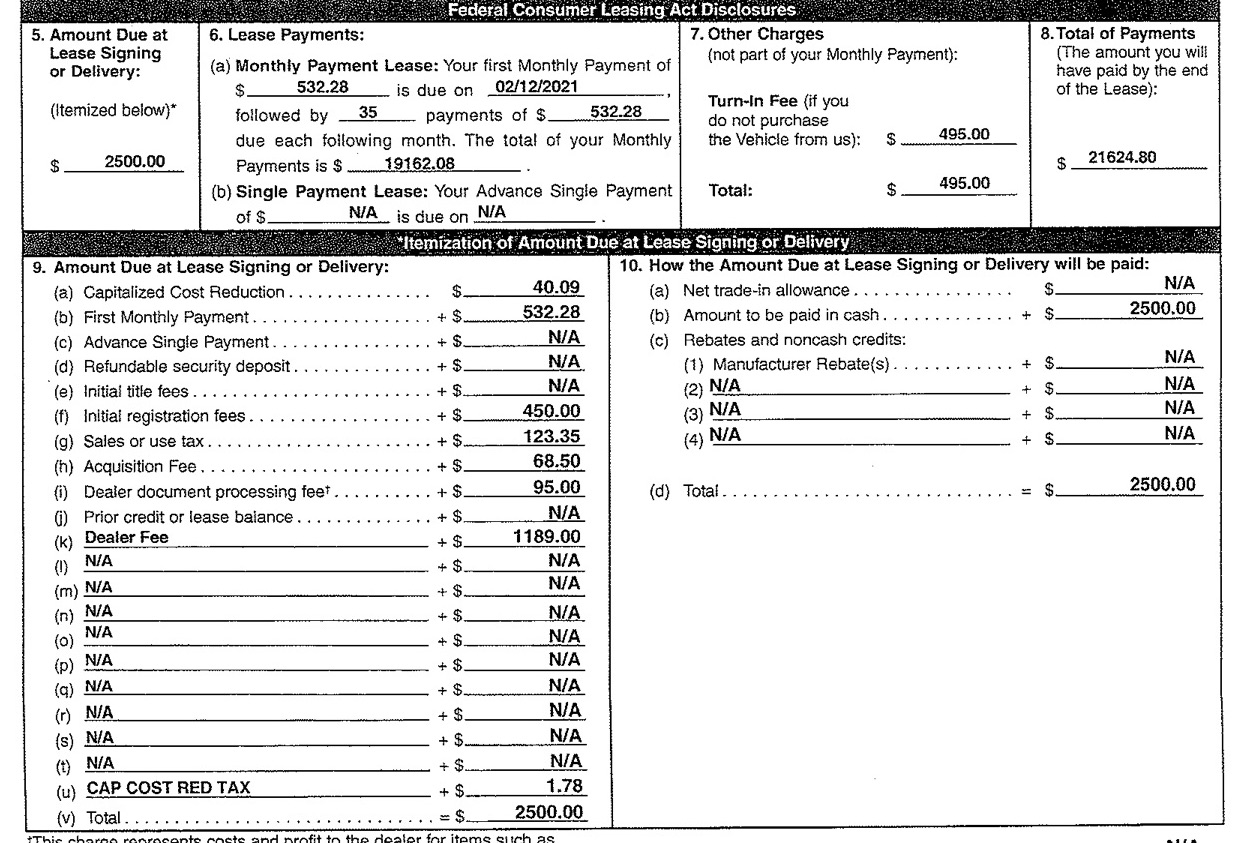

Having current, accurate information for residual value, money factor, and incentives is important in understanding your deal. As such, going directly to a source that has access to that data from the captive banks is your best option. The forums at Edmunds are where we go to get that information, as they have direct access to it from the captive banks. You’ll want to post of the model specific thread for the vehicle you’re interested in and request the most current numbers for your zip code. It is often easiest to find that thread by searching Google for “Edmunds lease” followed by the model of vehicle you’re interested in.

Buy rate is the mf as set by the bank. The dealer can’t lower the rate, but they can increase it. If they’re charging buy rate, there’s no negotiating possible here. If it’s not, you’ll want to determine how much. They may be showing a big discount on the sales price but be making it back up on the mf mark up.

Makes a lot of sense, thanks for clarifying that. So I need to figure out if that is the actual buy rate vs just the money factor that the dealer is setting.

Also, I noticed that lease contracts do not specify the money factor. But are dealers legally obligated to disclose it if you ask?