Not many new i3 left in Texas so I have to go fully loaded, eligible for $2500 state rebate and $7500 federal rebate post sale and $3000 loyalty. Separately, I can use $11,000 USAA non-stackable with $10,500 BMWFS+loyalty. Sales manager said the quote included a sales tax credit (unsure if for lease and purchase or just one of the two). Here’s what I’m getting right now:

Purchase MSRP: $57,095

Discount: $6,000 (10.5%)

Rebates: $10,500 (Manufacturer+Loyalty) Sale: $40,595 ($40,995 with dealer tint)

Sales Tax: $507

Doc: $150

TTL/Inspection: $165

Misc Fees: $27 Amount Due: $41,842

Post Sale Rebates: $7500 fed, $2500 state Net Price: $31,842

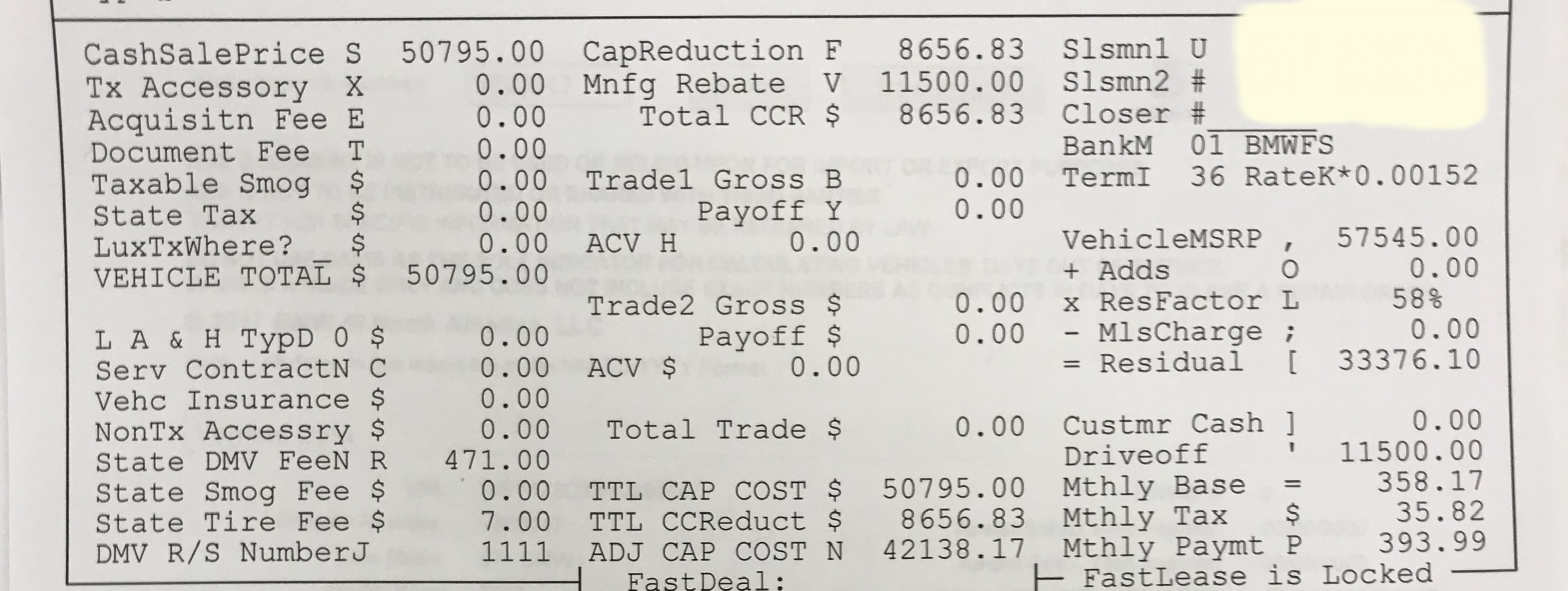

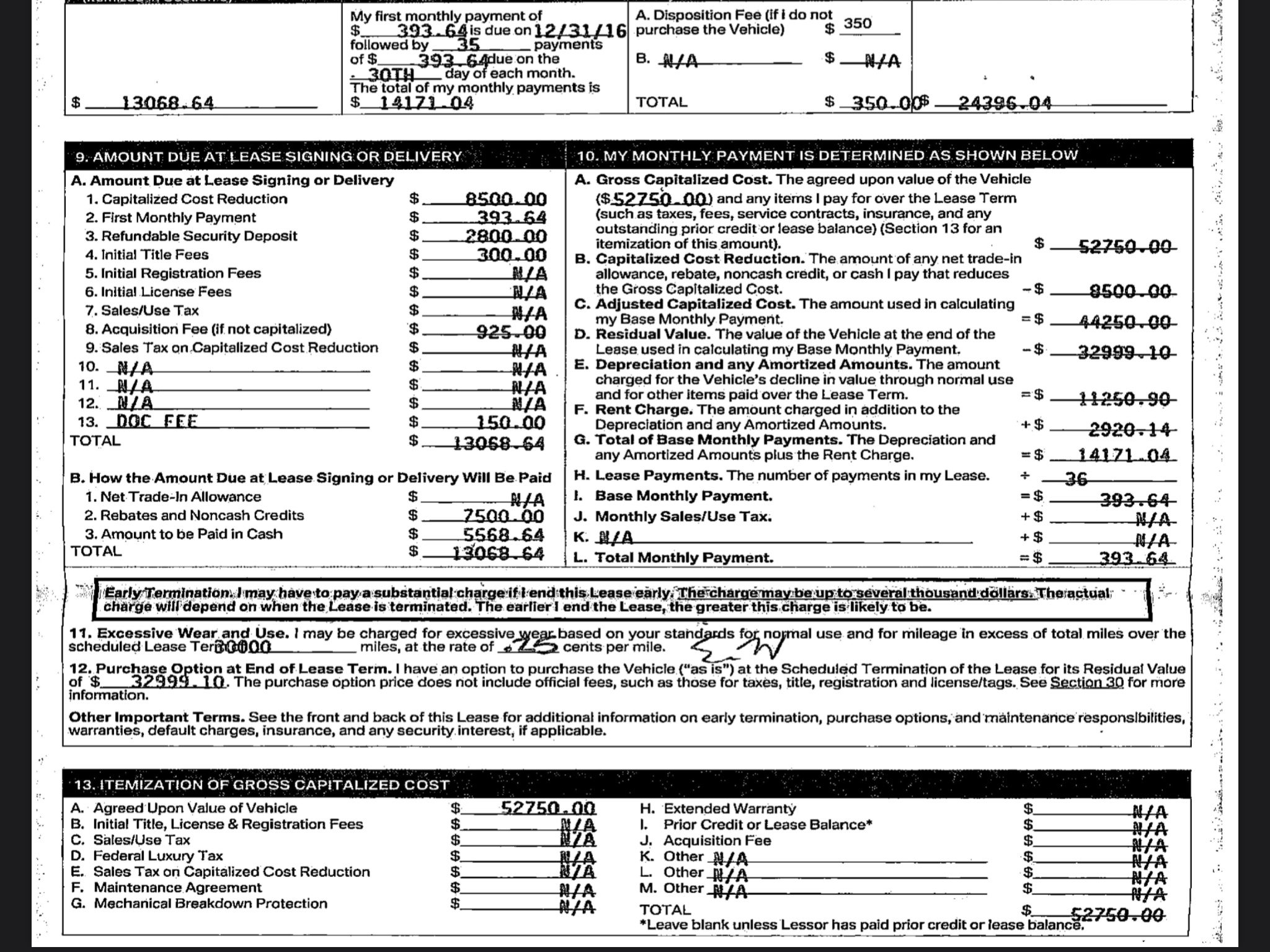

36/12K Lease Sale: $40,595

Residual: 57%

MF: .00168 (Looks like max markup)

0 MSD

Cash Due: $407 Monthly: $408

I plan to sweeten the purchase option with USAA (extra $500) and asking him to go half on the tint. He seems firm on his discount otherwise, probably due to scarcity. I have asked about Owner’s Choice but from another dealer I think only $7500 will apply and I’m not sure I can use USAA.

For the lease, I can’t get the number he is quoting (I’m coming up with around $386 monthly). Regardless, I’m asking him to give me buy rate (.00128 unless I’m mistaken), max out MSD, and waive acquisition for increase in MF.

For the hackrs Is there anything else I’m missing here? Would Owner’s Choice come out better or worse for those with experience?

I would definitely try to get more discount. I negotiated 13% off on a $51k i3 a couple months ago — you should be aiming for something around that, maybe even more given your car’s high sticker.

That’s almost identical to mine from 2 years ago, I think mine was 57-58k sticker, 36/10 but I rolled in all fees and registration etc so I have 35 payment at $393 including 10% Los Angeles tax. Minus 2500 state rebate and 400 power company rebate I’m low 300’s. I think you might have a little more wiggle room but it’s a sweet car for essentially $300 per month after you factor in your rebates. I think I got a tad over 11% off.

Haven’t double checked, but I’m pretty sure it’s much better to keep the acquisition fee for the lower rate, especially since you are going to do MSDs, I don’t really get that part?

And I wouldn’t buy any of these cars new, the residuals are over inflated and the battery packs keep getting better, original was 80 miles, then 120, and I think the next one will be around 180 miles on battery alone.

Are you sure you’re not counting the $7500 tax incentives twice on your purchase calculation?

My understanding is that the $10500 bmw incentives are the $7500 federal rebate plus the $3000 loyalty.

It would be strange if you would get those for purchase, but if you do, it may make the purchase a more attractive option.

Bmw passes the federal credit to you if you lease, and if you buy, you naturally get those as well.

The double dip is what makes the purchase option attractive. They are giving me $11K off if I bring my own financing (or $10.5 if I use them) plus I can still claim state and federal incentives, giving over $20K off the vehicle before dealer contribution!

I’ve heard that waiving acquisition for higher MF saves a few hundred over the course of the lease if the payment is low or the term short, but I’m not sure how 36 month sub-$400 plays there.

I’m currently leasing a 2017 Rex which is where my loyalty comes from, and it’s nearly identical to this one spec-wise. I plan to buy a Tesla eventually, and with competition starting to heat up (Rivian and others) I think this i3 would serve as a bridge for the next few years. You’re absolutely right about residual vs. resale.

Hence, even though a purchase wouldn’t normally be advisable in this case, if I’m looking at $31K after all rebates and discounts (lower than residual) and I can sell it for low-to-mid twenties after 3 years, I should end up with a lower overall cost, correct?

Not an expert, but I think the acquisition fee waiver is the equivalent to 10 MSDs. Use one of the calculators on here to double check. So put 7 MSDs then waive the acquisition fee to increase the MF and you are still in the hole. I think.

Some people are getting better deals, but for a car this MSRP it’s a bargain either way. I don’t know how the taxes affect a deal, but using one of your calculators and just selecting the waive Aquisition fee button says the payment goes up $10. All I say is just double check that, but either way I know a couple of people who are in the 4-500+ range for the same vehicle. Good deal no matter what even if someone else got something better.