then use the EV credit as a CCR; otherwise, residualize it. The above assumes the CCR tax is capitalized and that the monthly payment streams are taxed. The difference between capitalizing and not capitalizing the CCR tax is negligible. So, either pay the tax at lease inception or capitalize it. Either way, it will have a negligible impact on your decision.

NOTE: The expression above, if true, tells us by how much the residualized contractual payment exceeds the CCR contractual payment. In the example below, it is 33.65.

Lol again, I wasn’t sure what to expect from you, but this is more maths than I was envisioning. We gotta figure out how to get the LH software to embed a working spreadsheet hahah

I’m curious if there’s an inflection point where if the MF gets low enough or the tax rate gets low enough… that you’d be worse off with CCR Rebate vs Residual Rebate.

After picking up my brains from the floor since they EXPLODED

Your 3rd column is wrong as Residualized doesn’t work that way, they Alter the RV and the MF at the same time so your ‘simple’ plan of adding $7500 to the RV doesn’t work.

Absolutely! Check out the spreadsheet below. The payments are nearly equal with an MF = .00108. Try using MF = .00001 and it’s much better to residualize the EV credit. So, for this scenario, MF = .00108 is the breakeven. Anything below it favors residualizing the EV credit. Anything greater, favors using it as a CCR assuming the other variables (e.g., sales tax rate) remain the same.

I guess GM Financial has found a way to get people the lower monthly lease payment, and also remove their incentive to rapidly buy out the lease. I wonder if the other EV financing companies will follow suit.

I also wonder if their way of using the $7,500 to subvent the residual will make it harder to sell or securitize the lease. Since now the residual is grossly inflated. Most Blazer EV customers will get the $7,500 rebate as a tax deduction, so the real value in the secondary market will be much less than the subvented residual on the lease.

I think the captives self-insure their residuals. However, the banks usually purchase residual insurance through residual insurance carriers. I doubt the banks, or their residual insurers would allow a residualized EV credit.

Good question. I don’t know how their accounting works.

Rather than eating the $7500 as cap cost reductions immediately to customers. GM can raise MF some(Blazer LT model money MF is .00251) and collect the $7500 business tax credits for their financials.

The 2LT lease advertised on Chevy website at $469/month w/ enhanced residual. Normally would be $431/month, had the $7500 been a cap cost reduction.

Seems like this has been sufficiently answered, so to summarize…

Yes, it only applies to purchase, though many manufacturers pass it through on a lease. You can refer to this link for additional information, but be sure to confirm w/dealer before purchase.

If you intend to purchase and find that you do not qualify for the $7,500 credit due to the income limit, simply try being poorer.

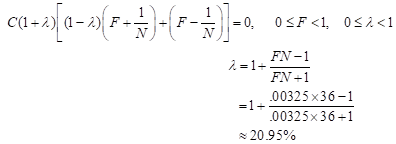

Sorry. You were wondering about the inflection point. It’s not an inflection point. An inflection point is where the concavity of a graph of a function changes. I think you meant the break-even point. In the interest of brevity, I skipped several steps in solving for F and the sales tax rate, lamda. See my original post.

Ok so latest list of Electric things that don’t get the $7,500 coming back through on a lease.

BMW 330e

BMW X5e

BMW 530e

Ford Escape PHEV FWD

Fisker Ocean (I don’t think it’s leasable now)

Chevrolet Silverado EV truck doesn’t seem to have the pass through yet

Subaru Outlander PHEV gets $6200 not $7500

Toyota Prius Prime

Toyota Rav4 Prime

Mercedes Benz C63s E Performance

(I’m leaving the Blazer EV off because a $7,500 residual enhancement is still a “passthrough” of some value related to the IRA money.)