I just got down to $13000 singlepay price everything included averaging out to $361 a month same 18000k a year. Is it still a crap deal? please I would love to know?

I don’t think AHFC rebates apply to demos, but I could be wrong. The dealer certainly doesn’t seem to think so and there’s no reason for him to hide a rebate.

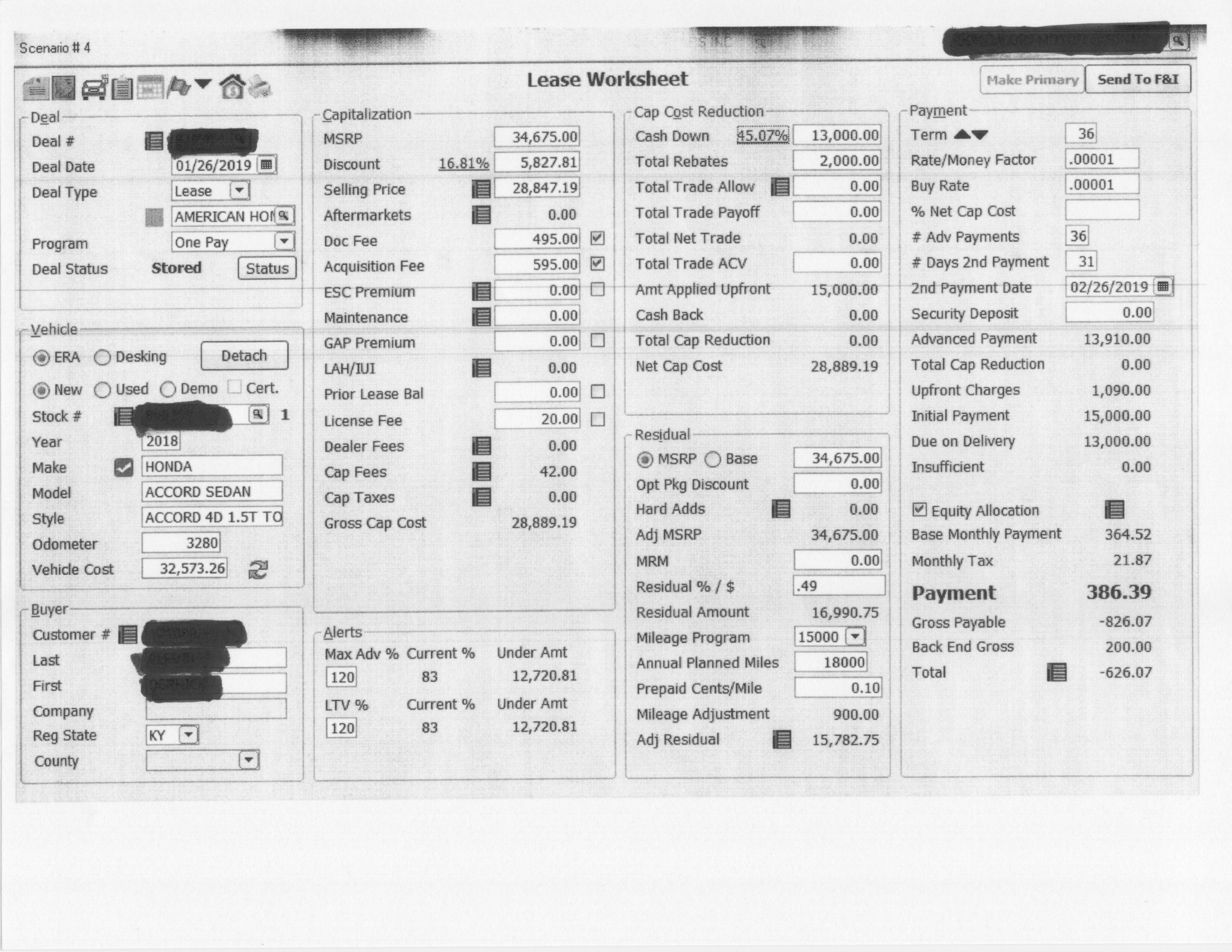

Ask the dealer to send you the lease worksheet for a $13k one pay. There are many Accord Touring 1.5T threads on here, you should know from them what selling price range is reasonable. You need to stop payment shopping this and work from selling price incl rebates.

And also ask if the $2900 rebate from AHFC applies to demos or not, because his prior sheet didn’t have it. I am also curious how the RV/allowed mileage changes with a Honda demo. I don’t think I’ve ever seen a Honda demo thread on here.

This post hurts my head, why would anyone talk to a dealer that’s $3k over sticker on the 2018 slow selling accord,

2 Likes

Funny how he dropped it $3k just like that…

Come down to $10000 one pay and work off that…

FROM THE MANAGER:

I have provided several documents for you to review below. I utilized the dealerships last remaining flex cash funds to accommodate the offer you provided me. the adjusted selling price of the 2018 1.5 touring demo is #26847.19 after utilizing the flex cash. that price also includes the appearance pkg which includes the following. 1) all season mats 2) trunk tray 3) splash guards 4) nitrogen in the tires 5) pin stripe. the front end profit reflects a -826.07 loss. minus dealer hold back of 676. Yielding a net loss of -150.07. Dealer hold back is not calculated in front end profit as it is utilized to cover variable expenses such as lighting; water; int. on floor plans etc. as a 14 year employee my price on this vehicle would be $2150 more than what we have agreed on for you. We are not allowed to utilize flex cash for employees because of the limited funds that are available. The owner reserves the right allocate those funds to his customers.

ME: I am still questioning if the Selling price is $26847 why is it showing $28847 and if the $2000 rebate applies and reduces the price then the Single pay price should be reflected $2000 less. Correct or am I looking at this wrong?

Manager Response: The adjusted selling price is 2000 less when you take into account for the flex cash. It does not however itemize on the price line. It gets itemized on the rebate line for a lease. Reference the additional 2000$ under the cash line. The additional accessories do not itemize on that work sheet at all. That expense comes off of my bottom line. They are itemized on the retail purchase co tract that you will sign in the business office. It’s a different document

Is he right?

initial payment of 15000 is reduced by the 2000 flex cash resulting in a 13000 DAS

he is still showing 495 doc fee which pays for the accessories he said he is eating; doc fee is additional dealer profit and negotiable

for a lease with 18k miles per year, i don’t see much more fat left to trim

Decent explanations from the manager IMO; don’t see that too often…GL

I have a done deal and going to sign later today. With the invaluable help from a certain few of this forum, I was able to come away with a deal of $12,000 Single pay 36 months, with 18k per year. Out of 5 dealers 3 wouldn’t touch even $13000 and 1 said they would match to a new 2018 but give nothing else with extras and appearance packages. I gave a best and final offer at the 11th hour and the Sales manager agreed! I had already received some oil changes, GC’s and so on. I have a great deal. I owe a big part of that to the few on here that gave me realistic feedback without all of the snark.

***Tonyg, you are right. This manager impressed me the entire way and throughout the entire process. Even though several felt that he started too high but I knew enough to know that I would never agree to a deal of any kind without vetting it. My issue in starting out was my lack of education with respect to know what the bottom line deal should look like and the best way to get there. Next time I will know before going into a negotiation what my bottom line will be instead of feeling my way through it and will some uncertainty. I knew there was a reason I didn’t walk away and I am glad I didn’t.

1 Like

333 a mo seems like a pretty good deal at 18k miles a year. Congrats!

I was never worried about the negotiating aspect of the process. Knowing what the bottom line should be and what to look for is what had me uncertain. Thanks to the forums I was able to get there and KNOW I got a good deal!

so, i was wrong. he found another 1000 to trim!

This deal beats the other dudes unicorn (295/month).

36/10 vs 36/18:

[34675 * 0.03] + 900 (prepaid miles, 15k-18k) = 1940 or ~54/mo

12000 / 36 = 333; 333 - 54 = 279 (equivalent 36/10k lease)

caveats: onepay, demo miles (it’s broken in)

with one-pay do you save on taxes?

Less interest and usually a lower interest rate.

- Less interest – Because you are making an upfront payment that covers the depreciation of the car over the period of time you’ll drive it, you don’t have to pay interest on this amount. So rather than paying interest on the full cost of the car, you only pay interest on the residual value, or the value of the car at the end of the lease, which is usually about 60% of the MSRP.

- Lower interest rate – Some manufactures (including Audi, Mercedes-Benz, Lexus and Porsche) will discount the interest rate for one pay leases. The savings can be significant—for example a 0.4% interest rate for a one pay instead of 2.8% for a traditional lease.

Good site for a more detailed explanation.

https://www.cartelligent.com/blog/when-does-one-pay-lease-make-sense

Yea I read that – how much easier is the credit approval? – why did you choose to go one pay as the mf is minimal on the term lease for the accord?

When I first started researching I wanted to avoid financing and I’m fortunate enough to be able to pay cash upfront. Plus I had purchased a couple of expensive macbook pros and Amazon had a great deal with earning 5% using my prime card so I charged it. Due to having no debt and a low need for credit I keep my accounts all paid. This put a LARGE hit on my score like 80 points. So I didn’t want that to affect my chances. I read credit wouldn’t play a factor with a single pay. Then when talking to the dealers I learned I heard wrong. Even when leasing there is still financing involved. Even though I had a hit they saw my history and my 1 hit but they said I had no issues with my score for them so I still qualified for top tier. The dealer reassured me that even if it would have dropped me in terms of a lower tier they would be able to talk to the necessary people to get it worked out. I still saved nearly $1000 over the traditional lease.

The take away is this. As long as your credit score isn’t extremely low due to negative factors. Thus demonstrating poor credit habits. and you don’t qualify on paper for top tier they will factor in the fact that you are putting up so much cash.**** Of course that was my experience and my outcome. Your results may vary.

Thanks for the reply makes sense.

Congrats on the deal.

In regards to credit, doesn’t matter if you are doing a one pay or traditional monthly lease, your credit worthiness is still measured and once the agreement is in place, the total amount of the lease payments which in your case is $12k will show up on your credit. Now what effect that new Honda loan will have on future needs all depends on your overall credit picture which is age and history, credit debt balances and new inquiries or credit apps.

How did I do?

Congrats on the solid deal! Make sure you share some pics of the car. I know you’ll love your time with it!

What happens if the car is in accident and gets totalled? This is prepaid deal, is it treated like a downpayment?